Kinder Morgan entered the final quarter of 2025 positioned exactly where investors want infrastructure players to be: at the center of structural energy demand, but insulated from commodity price volatility. Long-term, take-or-pay contracts continue to anchor cash flows as U.S. natural gas exports reshape global LNG markets.

The results reinforce that stability. Record earnings, strong free cash flow generation, and steady dividend growth underline a model built for durability rather than acceleration. For 2026, the message is clear: growth may be measured, but visibility and capital discipline remain the core of the investment case.

How was the last quarter?

In the fourth quarter of 2025, Kinder Morgan $KMI reported net income attributable to shareholders of $996 million, a significant improvement from $667 million in the same period last year. Adjusted for one-time items, primarily gains on asset sales, adjusted net income was $866 million, up 22% year-over-year.

Earnings per share were $0.45, up 50% year-over-year, while adjusted EPS of $0.39 was up 22%. These figures clearly demonstrate the company's strong operating leverage, which can turn relatively stable sales into ever-increasing profitability.

Adjusted EBITDA was $2.27 billion in the quarter, up 10% year-over-year, with the Natural Gas Pipelines segment being the main driver, benefiting from record gas transportation volumes towards LNG terminals and the domestic power sector. Operating cash flow was $1.7 billion and free cash flow after capital expenditures was $0.9 billion, representing year-over-year increases of 12% and 18%, respectively.

Management commentary

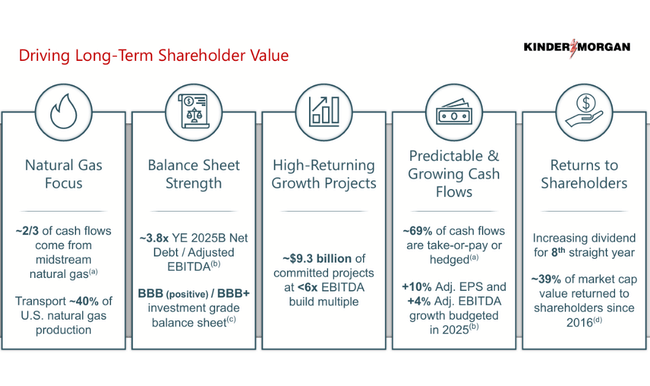

Management has repeatedly emphasized Kinder Morgan's strategic role in global energy security. According to Executive Chairman Richard Kinder, the company supplies more than 40% of the natural gas used as an input to US LNG facilities, directly contributing to US export dominance, particularly towards Europe.

CEO Kim Dang then highlighted the pipeline segment's record performance and the company's ability to internally fund growth projects without impairing its balance sheet position. Net debt to adjusted EBITDA remained at 3.8x, which is considered conservative and sustainable within the sector.

Outlook for 2026

The company's outlook for 2026 is moderate rather than expansionary, which may seem less attractive at first glance, but fits with Kinder Morgan's long-term philosophy. The firm expects adjusted net income of $3.1 billion, which implies roughly 5% growth from 2025 after adjusting for one-time items. Adjusted EPS is expected to be $1.36, also up approximately 5% from 2025.

Adjusted EBITDA is expected to reach $8.6 billion, up 2.5% year-over-year. The company also plans to pay a dividend of $1.19 per share, an additional 2% increase over 2025. Management expects to maintain debt at 3.8x EBITDA, confirming its focus on financial discipline.

The key growth driver remains structural growth in natural gas demand, which is estimated to grow 17% through 2030, primarily driven by LNG exports and data center energy demands.

Long-term results

Looking out to 2022-2024, it is evident that Kinder Morgan is a typical example of a stable infrastructure company. Revenues over this period were in the $15-19.5bn range, with a slight decline after 2022 reflecting the normalisation of energy markets rather than a structural issue in the business.

More fundamental is the evolution of profitability. Net profit rose from US$2.55 billion in 2022 to US$2.61 billion in 2024, while EPS increased from US$1.12 to US$1.17, despite a gradual decline in the number of shares outstanding. Adjusted EBITDA grew steadily from US$7.0 billion in 2022 to US$7.63 billion in 2024, confirming the gradual improvement in operating efficiency.

Margins remain very robust over the long term, driven by a high proportion of fee income and low sensitivity to commodity price fluctuations. The downside is relatively limited revenue growth, while the upside is high cash flow predictability and the ability to pay and grow the dividend over the long term.

News

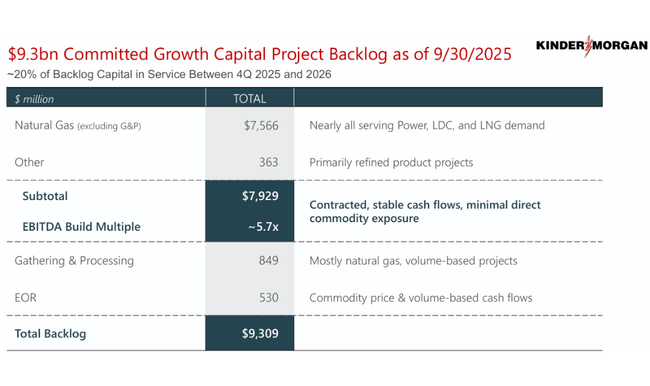

At the end of 2025, the company's project backlog was approximately $10 billion, with 90% of projects related to natural gas and the remainder directly related to power generation. Excluding specific segments, the company expects the remaining USD 8.6 billion of projects to generate an average EBITDA multiple of around 5.6 times in the first full year of operations.

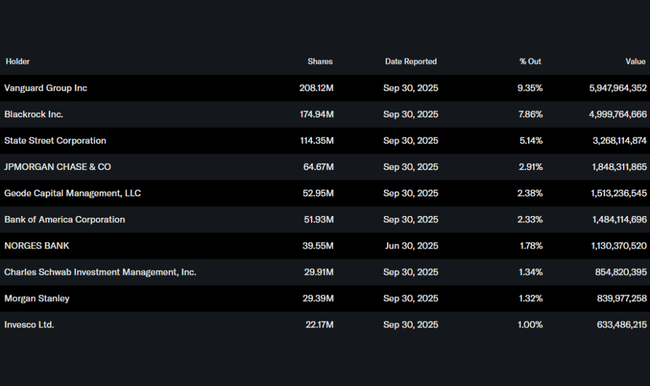

Shareholding structure

Kinder Morgan's shareholder structure combines significant insider participation with a dominance of long-term institutional investors. Approximately 13% of the shares are held by insiders, ensuring a strong alignment of management interests with shareholders. Institutions control roughly 69% of the shares, with Vanguard, BlackRock and State Street playing key roles.

Analyst expectations and market view

The analyst consensus for 2026 at Kinder Morgan is for stability and moderate growth, not acceleration. The market broadly accepts the firm's strong position in LNG infrastructure and high cash flow visibility, but also reflects that the pace of growth remains constrained by the capital intensity of the business and management's conservative financial policies.

Under the LSEG/Refinitivconsensus, analysts expect adjusted earnings per share of around $1.35-$1.38 for 2026, in line with the company's official guidance of $1.36. This consensus is key - neither the results nor the guidance surprised analysts to the upside. Adjusted EBITDA is expected to be around USD 8.5-8.7 billion, again very close to management's communicated target of USD 8.6 billion.

Target prices are in a relatively narrow range for most analyst houses. The median target price implies single-digit upside potential, with ratings concentrated mostly between "Hold" and "Moderate Buy". Analysts are particularly positive on the long-term LNG contracts, the high proportion of fee-based revenues and the disciplined approach to debt. In contrast, there is a more cautious stance on the pace of EPS growth beyond 2026 and the fact that a significant portion of the project backlog will be phased into results.