The fourth quarter of 2025 delivered a long-awaited positive milestone for Boeing: a return to operating and net profitability. After an exceptionally difficult 2024 marked by production disruptions, regulatory scrutiny, and heavy losses, the headline numbers suggest a meaningful improvement.

Markets remain cautious, however. A significant portion of the earnings recovery is tied to one-off items and accounting effects rather than a fully stabilized industrial core. As Boeing enters 2026, the focus shifts from whether the company has emerged from the trough to whether the improvement can be sustained without further setbacks.

How was the last quarter?

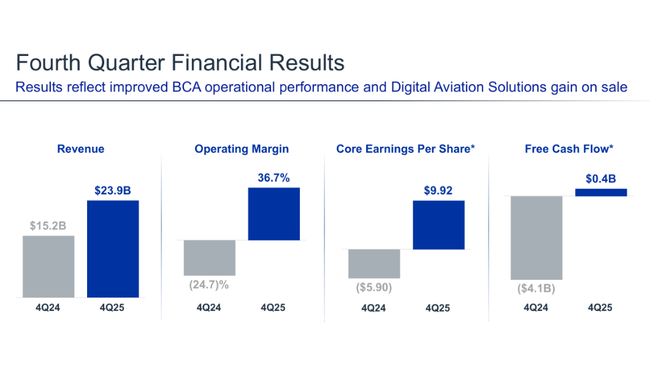

In Q4 2025, Boeing $BA reported revenue of $23.9 billion, up significantly year-over-year from $15.2 billion in Q4 2024. This growth was driven primarily by higher aircraft deliveries and strong performance from the services segment, particularly government contracts.

At the operating level, the company returned to profit. Operating profit reached USD 8.8 billion, while in the same period of the previous year Boeing posted an operating loss of USD 3.8 billion. However, the key factor was a one-off gain on the sale of Digital Aviation Solutions of USD 9.6 billion, without which the operating result would have looked much weaker.

Net income attributable to shareholders was $1.9 billion, compared to a loss of nearly $4 billion in Q4 2024. Earnings per share were $2.49, compared to $5.46 a year earlier. So the improvement is dramatic, but it should be read with an awareness of the strong impact of exceptional items.

In terms of cash flow, the situation remains mixed. While the company is generating positive operating cash flow, high inventories, production stabilization costs and service commitments continue to tie up the balance sheet and limit financial flexibility.

Global Services segment

The Global Services segment was clearly the strongest link of the quarter. Quarterly sales were $5.2 billion, a modest increase year over year, but the operating margin of over 200% is the main focus. However, this extreme figure does not reflect normal operating performance - it is almost entirely due to a one-off capital gain on the sale of Digital Aviation Solutions.

From a longer-term perspective, another figure is more important: Global Services won a record $28 billion in new orders in 2025 and ended the year with a record backlog of $30 billion. This confirms that service and government contracts remain a stable pillar of the business and a key source of future revenue, independent of the cyclical nature of commercial aviation production.

Management commentary

CEO Dave Calhoun commented on the 2025 results in a significantly more sober tone than would be consistent with Boeing's return to profit. In his assessment, he repeatedly emphasized that positive numbers are not an end in themselves, but the result of tough decisions, portfolio restructuring, and increased operational discipline. For Calhoun, 2025 was all about "resetting the company" and getting back to the basics: safety, quality production and stable cash flow.

The CEO freely admitted that much of the improvement in results was related to one-off items, particularly the sale of Digital Aviation Solutions, and warned against over-optimism. He stressed that the real measure of success would not be one-off profits, but the ability to maintain a positive operating result in future years without extraordinary effects. That's why he said the company had prioritised strengthening its balance sheet, reducing risks and simplifying its structure over aggressive growth in 2025.

Calhoun also highlighted the growing importance of the services and government contracts segment, which he described as a key stabilising element at a time when commercial aviation remains under regulatory and operational pressure. He said the record volume of orders in Global Services confirms that Boeing can generate value beyond the actual production of aircraft and that this segment will play a more important role in the group's overall profitability in the coming years.

Outlook

Boeing did not provide a detailed quantified outlook, which the market sees as a signal of caution. The company expects a gradual improvement in commercial aircraft deliveries and continued growth in services, particularly in the government and defence segments. At the same time, however, it openly admits that the production system remains fragile and that any further regulatory intervention or certification delays may slow down the planned turnaround.

For investors, this means that 2026 will primarily be a test of execution, not aggressive growth.

Long-term results: 2022-2025

A look at Boeing' s performance between 2022 and 2025 shows an extremely volatile trend that is unprecedented among large industrial concerns. The year 2022 was still marked by the reverberations of the pandemic and supply chain problems, with the company reporting revenues of USD 66.6 billion and remaining deep in the red. The operating loss exceeded $3.5 billion and the net loss was close to $5 billion, reflecting a combination of low aircraft deliveries, high fixed costs and extraordinary expenses related to production quality.

The year 2023 brought the first signs of a stabilisation in revenues, which rose to nearly US$77.8 billion, but profitability remained negative. While the operating loss narrowed, the company was still unable to generate a sustainable operating profit. This year can be described as more of a "stop the bleeding" phase than an actual turnaround. Margins remained under pressure and the return to normal production rates was slower than the market expected.

The turning point came in 2024, but in a negative direction. Revenues fell back to $66.5 billion and Boeing posted a massive operating loss of over $10.7 billion and a net loss of nearly $12 billion. This decline was the result of a combination of production issues, regulatory intervention, and cost increases associated with quality control, customer compensation, and delivery delays. It was 2024 that significantly damaged investor confidence and confirmed that the company's problems are not cyclical but structural.

The year 2025 then presents a stark contrast. Revenues jumped to USD 89.5 billion, up more than 34% year-on-year. Boeing returned to an operating profit of USD 4.3 billion and a net profit of USD 1.9 billion. However, this turnaround should be read with caution. The results were significantly boosted by a one-off capital gain on the sale of part of the business, while the operating margin itself remains low and sensitive to any fluctuations in production.

News

The most significant strategic event of 2025 was the sale of the Digital Aviation Solutions division, which generated a capital gain of approximately $9.6 billion for Boeing. The move was not just an accounting operation, but part of a broader effort to simplify the company's structure, focus on key areas and strengthen the balance sheet. It sent a clear signal to management that it was willing to sacrifice non-core activities in favour of stabilising the core business.

In addition, Boeing significantly strengthened its Global Services segment, which won a record $28 billion in new orders in 2025 and closed the year with a backlog of $30 billion, the highest in the segment's history. A key contract was an order from the U.S. Air Force to upgrade the cockpits of the C-17 aircraft, among others. It is services and government contracts that are increasingly being profiled as a stabilizing element, partially offsetting the volatility of commercial aircraft production.

Another important step is the pending acquisition of Spirit AeroSystems to gain greater control over key parts of the supply chain. This is Boeing's response to long-standing quality and production coordination issues. While this transaction may increase the costs and risks of integration in the short term, in the long term it has the potential to reduce operational uncertainty and improve quality management.

Shareholding structure

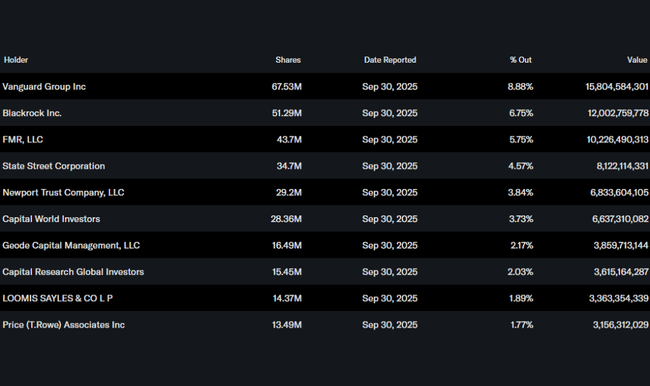

The shareholder base remains strongly institutional. The largest shareholders are Vanguard, BlackRock, Fidelity and State Street, suggesting that Boeing remains an important part of long-term portfolios, although the short-term investment thesis remains high-risk.

Analyst expectations

Analysts view the results as a step in the right direction, but the consensus remains cautious. Key questions for the coming quarters center on the sustainability of profitability without one-off effects, the stabilization of narrow-body aircraft production, and the ability to generate consistent free cash flow.

Boeing is therefore not a story of a quick turnaround, but of a long restructuring, where each positive quarter must be confirmed by the next. Meanwhile, the market is making it clear that it will take more than one good quarter to fully restore confidence.