AT&T’s fourth-quarter results confirm that the business is operating in a stable and predictable mode. Cash flow remains solid, adjusted earnings are under control, and the core operations continue to support the balance sheet. From a defensive standpoint, the story holds together.

What the results do not offer is a turning point. Revenue momentum remains limited, margin expansion is not the focus, and there is no new catalyst to reframe the investment narrative. For investors, AT&T continues to represent a cash-flow and dividend profile rather than a growth opportunity, with the key question centered on sustainability rather than acceleration.

How was the last quarter?

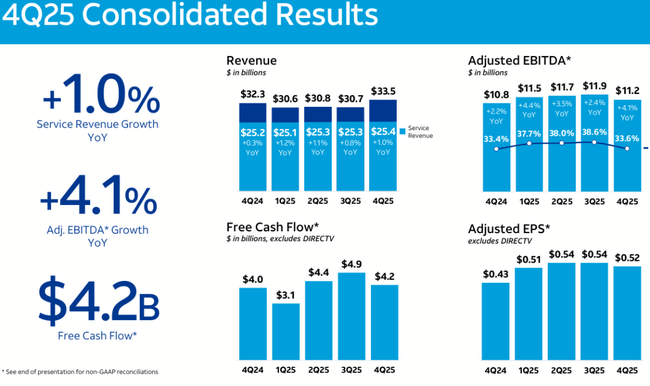

Q4 2025 confirmed the continued trend of low revenue growth but solid operational performance. Total revenues reached $32.3 billion, up 0.3% year-on-year. This is very limited momentum at the overall level, but a positive signal coming from the core business. Service revenue grew by 1.0% YoY, showing that core telecom services maintained a modest upward trajectory.

Operational performance was stronger than revenue growth. Adjusted EBITDA in Q4 was $10.9bn, up 4.1% YoY. EBITDA margin was 33.6%, slightly above Q4 2024 levels, although well below the seasonally strong Q3. This confirms that AT&T $T can maintain cost discipline, but without significant margin leverage.

At the earnings level, the company reported a net profit of $4.16 billion. Adjusted EPS came in at $0.52, a noticeable improvement from $0.43 in Q4 2024, but also a slight slowdown from Q3 2025. Thus, profitability remains stable, not accelerating.

From a cash perspective, the quarter was solid. Free cash flow was US$4.2bn, down from a strong Q3, but in the context of the full year confirms the company's ability to generate cash even with high investment.

Q4 2025 Highlights:

Revenues $32.3 billion, +0.3% YoY

Service revenue +1.0% YoY

Adjusted EBITDA USD 10.9 billion, +4.1% YoY

EBITDA margin 33.6% YoY

Free cash flow USD 4.2 billion

Adjusted EPS USD 0.52 (vs. USD 0.43 YoY)

Segment view: where AT&T is gaining and losing momentum

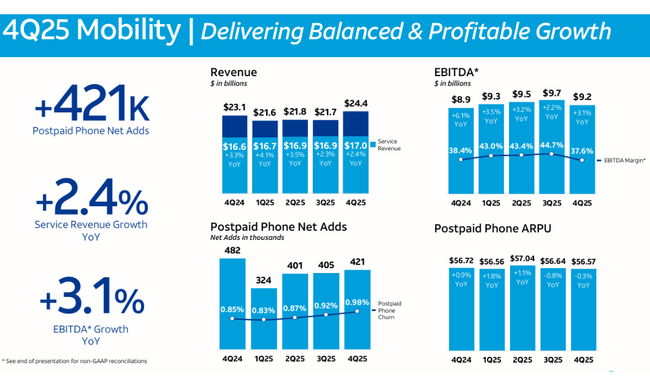

The mobile segment remains a mainstay of stability. Postpaid phone net adds were +421k, a solid result in a highly competitive environment. Postpaid ARPU rose to $56.72 (+0.9% YoY), indicating good customer retention. Service revenue in the mobile segment grew by 2.4% YoY and EBITDA by 3.1% YoY, confirming balanced, profitable growth.

Optical infrastructure continues to perform very strongly. AT&T Fiber added 283k customers in Q4, while Internet Air gained another 221k. Fiber revenue grew 13.6% YoY and Fiber ARPU reached $72.87, well above traditional broadband. Also crucial is the growth in convergence rate to 42%, meaning more customers are using multiple AT&T services simultaneously and increasing their long-term value.

Business Wireline, on the other hand, remains a weak link. EBITDA in this segment declined 6.7% YoY, reflecting the structural decline in traditional business connectivity. While growth in fiber and advanced connectivity cushioned some of the decline, the trend remains negative.

Management commentary

Management emphasizes balanced growth, stability and discipline in capital allocation. Mobile, fibre and customer convergence across the portfolio remain strategic priorities.

Communications indicate that AT&T is not targeting aggressive expansion. Instead, it is focusing on maximizing the value of existing infrastructure, maintaining a quality network and gradually improving financial flexibility. This conservative approach is a key reason why the title is viewed as a defensive investment rather than a growth story.

Outlook

The outlook for 2026 to 2028 confirms a steady but limited growth trajectory. Management expects service revenue growth in the low-single-digit range annually, i.e. without significant acceleration. Adjusted EBITDA is expected to grow 5%+ in 2026, with gradual improvement towards 5%+ by 2028.

Capital investment is expected to remain in the range of $23-24bn per year, implying continued investment in the network without dramatic increases. A key point in the outlook is free cash flow, which is expected to reach US$18+bn in 2026, US$19+bn in 2027 and US$21+bn in 2028. This is critical for both dividend sustainability and debt reduction.

On the earnings front, the firm expects adjusted EPS of US$2.25-2.35 in 2026 and double-digit three-year CAGR through 2028, suggesting gradual improvement rather than leapfrog growth.

Long-term results

The long-term view shows a company that has undergone a painful restructuring and is now in a normalization phase. Revenues in 2025 reach $125.6 billion, representing 2.7% year-over-year growth after a flat 2024. This confirms that AT&T is operating in an environment of very limited structural growth.

Stability is evident at the operating profit level. Operating income was USD 24.2 billion, virtually unchanged from the previous year. EBITDA rose to USD 53.2bn (+20.9% YoY), reflecting a combination of operational discipline and normalisation after previous exceptional items.

The most visible improvement came on the bottom line. Net income rose to US$21.9bn, almost double the 2024 figure, and EPS came in at US$3.04 (+104% YoY). However, this jump should be read as a return to normal after a weaker year, not a new growth trend.

The number of shares outstanding remains stable, which means that EPS changes do indeed reflect profitability trends. AT&T thus confirms the long-term profile of a company that maximizes value through cash flow, not through revenue growth.

News

During the year, AT&T continued to expand its fiber network, increase its convergence rate and gradually reduce debt. The company has avoided large acquisitions and remains conservative in its capital policy, which promotes stability but limits the potential for faster expansion.

Shareholding structure

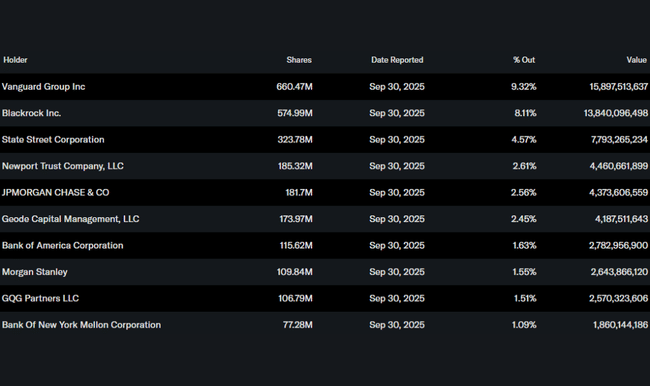

The shareholder structure is strongly institutional. The institution holds roughly 67% of the shares, with Vanguard (9.3%), BlackRock (8.1%) and State Street (4.6%) being the largest shareholders. The low insider stake is consistent with the mature stage of the firm and the long-term nature of the investment base.

Analyst expectations

Analyst consensus remains cautious but stable. AT&T is viewed as a defensive title with an attractive dividend yield and predictable cash flow. Analysts appreciate the improvement in capital structure and stabilization of results, but also note limited growth potential and sensitivity to macroeconomic conditions. Thus, the market's post-earnings reaction is consistent with reality - AT&T is delivering what it promises, but does not warrant an upward repricing.