Wall Street has largely moved past celebrating growth for its own sake. The premium today is on companies that can turn demand into cash, and cash into cleaner, scalable profitability — especially in industrial sectors where backlogs can look great while the income statement still leaks through costs and taxes.

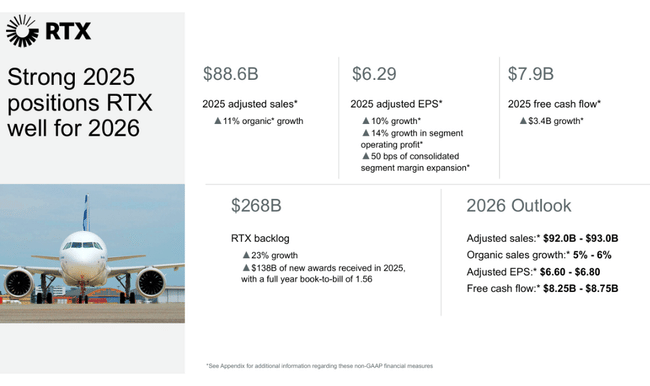

RTX ends 2025 with the kind of visibility investors like: revenue rose 12% to $24 billion, cash flow improved meaningfully, and backlog hit a new high across both commercial and defense programs. But the quarter also draws a line under what still needs fixing: adjusted EPS didn’t match the pace of the top line, with higher costs, tariffs, and a heavier tax burden still eating into the upside.

How was the last quarter?

RTX $RTX delivered fourth-quarter 2025 revenue of $24.2 billion, up 12% year-over-year, or 14% organically. Growth was broadly spread across all three major segments, confirming the return of commercial aviation and the continued strength of defense budgets. GAAP earnings per share were $1.19, but were significantly weighed down by acquisition accounting and restructuring costs. Adjusted EPS came in at $1.55, up only 1% year-over-year, showing that the cost base is still not fully optimized.

Net income attributable to shareholders was $1.6 billion, while adjusted net income rose to $2.1 billion, up 2% year-over-year. The key positive of the quarter was the return of strong cash flow, with operating cash flow reaching US$4.2bn and free cash flow reaching US$3.2bn, a sharp jump from the weak finish to 2024. It is cash flow that is becoming the main argument for RTX's investment story.

Visibility of future earnings has also improved significantly. The company's total backlog has grown to $268 billion, of which $161 billion is attributable to the commercial segment and $107 billion to defense contracts. This ratio confirms that RTX is not unilaterally dependent on government budgets, but is also benefiting from the resurgence of global air travel.

Segment performance: where value is created

Collins Aerospace reported fourth quarter revenues of $7.7 billion, up 3% year-over-year. But the real strength was in operating profit, which rose 27%, with margin improving 340 basis points. On an adjusted basis, profit growth was more modest, but the segment benefited from strong aftermarket growth, which is significantly more attractive on a margin basis than new aircraft deliveries.

Pratt & Whitney was the growth driver. Revenues jumped 25% to $9.5 billion, mainly due to higher volumes in commercial engines and strong military production. Operating profit rose 53%, although adjusted growth was lower due to higher costs and the absence of one-off items from last year. Still, the segment clearly shows operating leverage on rising volumes.

Raytheon added solid but less dynamic growth. Revenues were up 7% to $7.7 billion, while adjusted operating profit rose 22%. Air defense systems and naval programs play a key role here, where demand remains structurally strong due to geopolitical tensions.

CEO comment

CEO Chris Calio called 2025 a watershed year in terms of operational discipline. In his comments, he emphasized that the growth in revenue, earnings and cash flow is the result of better execution, not simply a cyclical recovery. He said RTX enters 2026 with "significant momentum", underpinned by record backlog and improving manufacturing stability.

Calio also openly admitted that investing in new capacity and technology remains a key priority. The company is focusing on expanding production lines, shortening supply chains and delivering orders on time, which is particularly critical for defence contracts. The CEO thus clearly frames 2026 as the period when RTX is to translate strong demand into higher and more sustainable margins.

Outlook for 2026: growth with better quality

For the full year 2026, RTX expects adjusted revenues in the range of $92-93 billion, implying 5-6% organic growth. Adjusted earnings per share are expected to be between US$6.60 and US$6.80, a further acceleration from 2025. Free cash flow is expected to rise to US$8.25-8.75bn, confirming the firm's emphasis on cash returns, not just accounting profit.

The outlook also assumes continued investment in manufacturing and technology, which limits margin expansion in the short term but enhances long-term competitiveness. The market views this approach positively as it reduces the risk of a repeat of the operational problems of previous years.

Long-term results

A look at the last four years shows that RTX has had a significantly volatile period. Revenues grew from $67.1 billion in 2022 to $88.6 billion in 2025, with the greatest acceleration coming in 2024 and 2025. However, profitability fluctuated significantly more than revenues, with operating profit falling sharply in 2023 to increase by more than 33% in 2025.

Net profit reached $6.7 billion in 2025, up 41% year-on-year, and EPS rose by almost 40%. But this jump isn't just cyclical - it also reflects stabilizing costs, an improving order mix and a return of operating leverage. In the long term, this puts RTX back on track towards a model where the combination of defence and commercial aviation generates balanced and predictable growth.

News and capital discipline

During the year, RTX completed the divestment of part of Collins Aerospace, simplifying the portfolio and freeing up capital for key areas. At the same time, the company continues to expand production capacity in engines and defence systems where demand is highest. The record backlog confirms that these investments have real backing in future orders.

Shareholding structure

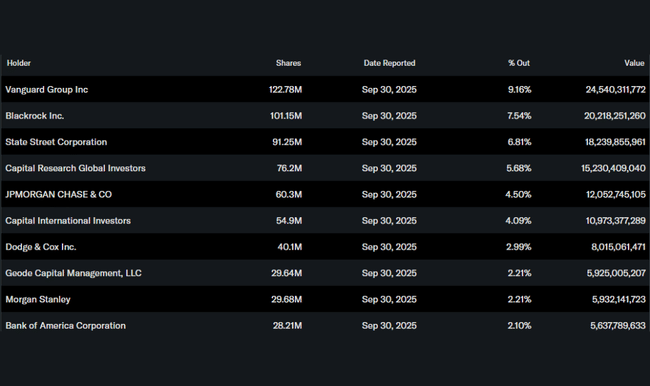

RTX has an exceptionally strong institutional base - the institution holds more than 81% of the shares. The largest shareholders are Vanguard, BlackRock and State Street, confirming that the title is viewed as a long-term strategic position, not a short-term speculation.