Nvidia reported $68.1 billion in quarterly revenue. Growth was strong both versus last quarter and last year, and the core driver remains data-center spending for AI. The key quality signal is that profitability did not weaken at this scale. Gross margin stayed around 75%, and operating profit grew faster than revenue.

What investors will focus on next is guidance. Nvidia expects about $78.0 billion in revenue next quarter, with a small range around that figure. The company also said this outlook assumes no data-center revenue from China. That supports the idea that demand elsewhere is very strong, but it also highlights how export rules can still affect where growth comes from.

How was the last quarter?

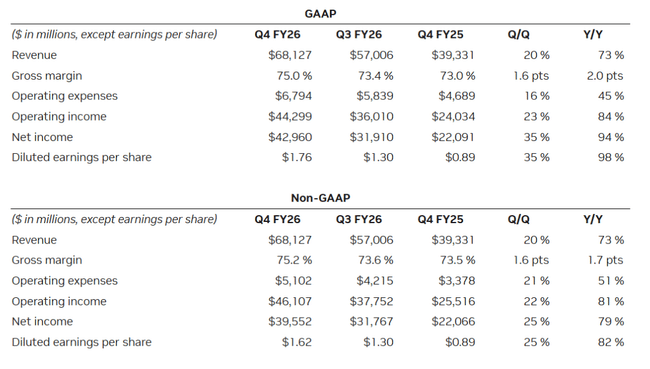

In the fourth quarter of fiscal year 2026, Nvidia $NVDA posted revenue of $68.127 billion, up +20% versus Q3 and +73% year-over-year. Gross margin on a standard accounting basis was 75.0% (75.2% adjusted), up 1.6 percentage points from the prior quarter. Operating expenses rose to $6.794 billion (+16% vs. Q3), but operating profit and net income rose to $44.299 billion (+23% vs. Q3) and $42.960 billion (+35% vs. Q3), respectively, thanks to faster sales and margin growth. Earnings per share were $1.76 ($1.62 after adjusting for the impact of the same).

The key is where the growth is coming from. Data center segment revenue was $62.3 billion, and itself grew faster than the company as a whole: +22% vs. Q3 and +75% year-over-year. For the full fiscal year 2026, the data center segment generated $193.7 billion (+68%). This means that today it is no longer "one strong product" but an industry-wide range of computing infrastructure delivery, where networking, systems and entire turnkey platforms for running AI are sold alongside the chips themselves.

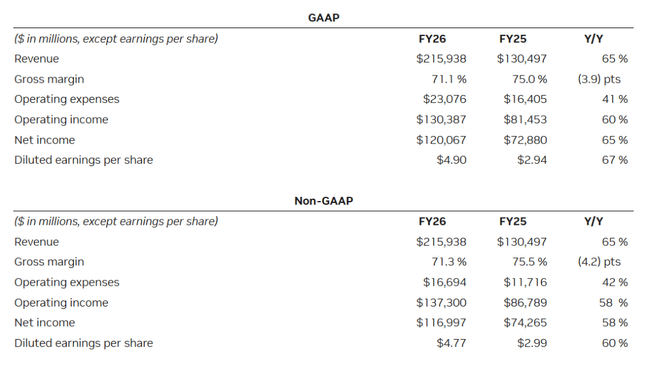

At a company-wide level, the picture is similarly extreme for the full year. Fiscal year 2026 brought revenues of $215.938 billion (+65%), operating profit of $130.387 billion (+60%), and net income of $120.067 billion (+65%). Earnings per share rose to $4.90 ($4.77 on an adjusted basis). At the same time, we can see that the company is investing in growth and people: annual operating expenses increased by 41% (on standard accounting), a logical accompaniment to a situation where NVIDIA is running at the edge of capacity while preparing the next product generation.

A very important part of the report is the return on capital. NVIDIA returned $41.1 billion to shareholders during fiscal year 2026 (a combination of buybacks and dividends) and still had $58.5 billion of authorized buyback capacity available at the end of Q4. The dividend remains nominal ($0.01 per share), so the main tool for shareholders continues to be buybacks.

Highlights of the results

Revenues of $68.1 billion, +20% versus last quarter, +73% year-over-year.

Data center revenue $62.3 billion, +22% vs. last quarter, +75% YoY.

Gross margin of 75.0% (75.2% adjusted), an improvement from last quarter.

Operating profit $44.3 billion, +23% vs. last quarter, +84% YoY.

Net income $43.0 billion, +35% versus last quarter, +94% year-over-year.

Earnings per share $1.76 (adjusted $1.62), nearly double year-over-year.

For the full fiscal year 2026, sales of $215.9 billion (+65%) and net income of $120.1 billion (+65%).

The company returned $41.1 billion to shareholders in 2026 (buybacks and dividends) and still has $58.5 billion in authorized buybacks.

Q1 outlook: revenue of $78.0 billion plus or minus 2% and excluding data center contribution from China.

Important accounting change: starting in Q1, the company will now include stock compensation expense in "adjusted" metrics.

CEO's comments

Jensen Huang builds the communication on the fact that companies are moving from experimentation to mass adoption of "autonomous helpers" in software and processes, which is lifting demand for computing power and shifting the focus from learning models towards their daily use in companies. In practice, this means a push for the lowest cost per compute and the highest efficiency, where NVIDIA is betting on next-generation systems and fast inter-chip interconnects. The tone is both confident and investment-savvy: the company wants to convince the market that the biggest wave of demand isn't over, it's just changing shape.

Outlook

The outlook for the first quarter of the fiscal year is exceptionally strong: revenue of $78.0 billion plus or minus 2%. Gross margin is expected to remain around 75% (74.9% on a standard accounting basis and 75.0% on an adjusted basis, with a plus or minus 0.5 percentage point tolerance). Operating expenses are expected to rise to about $7.7 billion ($7.5 billion on an adjusted basis), with about $1.9 billion of stock compensation expense already included.

The sentence about China deserves the most attention: NVIDIA does not include any data center revenue from China in the outlook. If the situation doesn't improve, it's a drag. If, on the other hand, there is a possibility of at least partial shipments, this is an asymmetric positive factor that is not in the current outlook.

Long-term results

Nvidia today is an extreme example of what the combination of a superior product, strong demand and operating leverage will do. Yet fiscal 2022 was a "normal" tech business: sales of around $26.9 billion and profits of $9.8 billion. Fiscal year 2023 was virtually stagnant sales, but also a push for profitability - operating profit fell to around 4.2 billion and net profit to 4.4 billion. Then the story broke: fiscal year 2024 brought sales of 60.9 billion and net profit of 29.8 billion. Fiscal year 2025 had already jumped to 130.5 billion in sales and 72.9 billion in net profit. And now fiscal year 2026 has delivered sales of 215.9 billion and net profit of 120.1 billion. That's not "rapid growth," that's a scaling of the entire business in just a few years.

But the bottom line is that it's not just about sales, it's about how profitability behaves. Gross margin in the quarter [Q4 2026] was around 75%, very high even by the standards of the top semiconductor companies. For the full fiscal year 2026, gross margin is lower than the previous year (the data shows a drop of about four percentage points), a signal that the company is also rapidly expanding capacity, changing product generations, and some of the "cost of production" may be temporarily pushing margins. Even with that, however, operating profit for 2026 was $130.4 billion, up 60% from a year ago. In other words, even if margins fluctuate slightly, volume and operating leverage are so great that overall profits continue to grow at a tremendous rate.

When we look at costs, there is an important nuance: operating costs are growing fast (over 40% annually), but in absolute terms they are still "small" compared to the growth in sales and profits. That's the very definition of operating leverage - the company adds people, development and operations, but every additional dollar of sales carries a high contribution to profits.

Another long term important factor is "earnings per share" and working with share count. Nvidia has a slightly declining average share count, so earnings growth translates well into growth per share. Earnings per share for fiscal year 2026 rose to $4.90 ($4.77 after adjusting). And because the company is returning huge cash through buybacks, this effect may continue to strengthen. In fiscal 2026 alone, it returned $41.1 billion to shareholders through buybacks and dividends, and at the end of the quarter it still had $58.5 billion in authorized buybacks. The dividend is rather symbolic; the main "driver for shareholders" is share buybacks.

News

The report shows that NVIDIA doesn't want to stand on just one product generation. The company has unveiled the next platform for the next period, while expanding partnerships with key players that operate large data centers. At the same time, it is strengthening the ecosystem around networking, storage and software so that customers buy the whole solution, not just the chip. Significantly, the company is also openly communicating the push for AI operational efficiency, i.e., reducing the cost of running models in the field, a topic that will directly impact customer investments in 2026 and beyond.

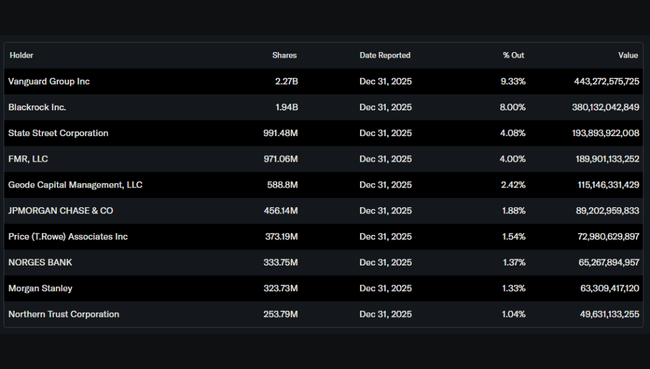

Shareholder structure

Nvidia is a distinctly institutional title: institutions hold roughly 69.6% of the stock (and roughly 72.8% of the free float), while insiders hold around 4.35%. The largest holders are Vanguard, BlackRock, State Street, Fidelity and Geode. This typically means high liquidity, stable "index" capital, and also sensitivity to how large funds change exposure to AI and the technology sector as a whole.