Salesforce’s quarter matters because it combines two things investors want to see in large software names: steady customer demand and a clear shift toward shareholder returns. The company ended the fiscal year at a higher revenue base, and future contracted revenue remains strong, which supports the idea that customers are still committing for the next years.

What changes the tone is the capital return plan. Salesforce generated very large operating cash flow and free cash flow over the year, and management is using that capacity to raise shareholder payouts. The company announced a new $50 billion share repurchase authorization and increased the dividend to $0.44 per share. For investors, the message is simple: growth continues, but the company is now also behaving like a mature cash generator that returns more capital.

How was the last quarter?

Salesforce $CRM showed in the fourth quarter that it can grow without "buying" revenue at the expense of profitability. Revenue rose to $11.2 billion and the core foundation of the business - subscriptions and support - added 13% to $10.7 billion. This is important because this is the part that is most predictable and forms the core of the company's long-term value.

But the report's strongest metric is the pipeline of contracts going forward. Total contracted future revenue of $72.4 billion (+14%) shows that despite the large comparative base, demand for the platform is still very much alive. Short-term contracted revenues of 35.1 billion (+16%) then suggest that it is not just a case of "sometime in the future" but that the contract pipeline is spilling over into revenues in the foreseeable future.

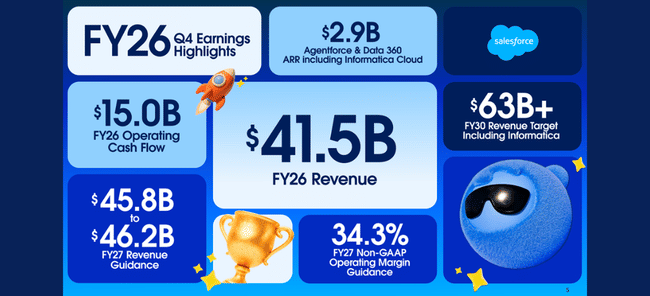

And the third layer is cash. For the full year, the company generated $15.0 billion of operating cash flow and $14.4 billion of free cash flow. To an investor, this means that Salesforce is not just a "growth story" but a very strong cash machine that can afford massive buyouts while investing in products and acquisitions.

Highlights of the results and outlook

Q4 revenue: $11.2 billion, up +12% year-over-year.

Subscription and support revenue: $10.7 billion, +13% YoY.

Total contracted future revenue (RPO): $72.4 billion, +14% year-over-year.

"Short-term contracted" revenue (cRPO): $35.1 billion, +16% y/y.

Operating margin for 2026: 20.1% on an accounting basis and 34.1% after adjustments.

Operating cash flow: $15.0 billion(+15%) and free cash flow : $14.4 billion(+16%).

Return of capital to shareholders: $14.3 billion (buybacks 12.7 + dividends 1.6).

New buyback program: $50 billion (replaces unused previous programs).

Dividend raised to $0.44 per share(+5.8%).

Q1 outlook: revenue of $11.03-11.08 billion, "short-term contracted" revenue growth of around 14%.

Outlook for sales (full year): $45.8-46.2 billion and operating cash flow is expected to grow about 9-10%.

CEO commentary

Marc Benioff builds communications on the fact that Salesforce wants to be the "operating system" for businesses where work is combined between humans and automated helpers in software. From an investor's perspective, it's important to filter the marketing and take the hard numbers that management attaches to it: annual recurring revenue from the suite around Agentforce and Data 360 exceeded $2.9 billion (more than tripling year-over-year), and Agentforce alone reached $800 million, growing 169% year-over-year. In addition, CFO Robin Washington mentions that the acceleration of "new contracts and expansion with existing customers" in the second half of the year reinforces confidence that organic growth can accelerate again in the second half of fiscal 2027.

Outlook

The outlook for 2027 is built on two pillars: steady double-digit revenue growth and maintaining strong profitability after adjustments. Salesforce expects revenue of $45.8 billion to $46.2 billion, or 10-11% growth, and an operating margin of 20.9% on an accounting basis and 34.3% after adjustments. That's a clear signal that the company doesn't want to "chase" growth at the cost of broken margins - and that the discipline the market has appreciated in Salesforce in recent years is set to continue.

For the first quarter, the company expects revenue of $11.03 billion to $11.08 billion and earnings per share after adjustments of $3.11 to $3.13. At the same time, it expects near-term contracted sales to grow around 14%, which is important because that metric often outpaces the future pace of reported sales. At the same time, management is explicit that organic growth should accelerate again in the second half of the year - a promise the market will want to see confirmed in the next two to three quarters.

Long-term results

Salesforce has undergone a four-year transformation from a "fast-growing company" to a "large, steadily growing, high-margin company with huge cash." Revenues have grown from $31.4 billion in 2023 to $34.9 billion in 2024, $37.9 billion in 2025 and $41.5 billion in (FY) 2026. The growth rate has gradually stabilized around 9-11% per year, which is typical for a company of this size - which is why the question of whether new products can "kick-start" growth again without having to discount margins comes to the fore.

Profitability is seeing a return of operating leverage. Operating profit has risen from $1.0 billion in 2023 to $5.0 billion in 2024, $7.2 billion in 2025 and $8.3 billion in 2026. That's a massive shift that didn't happen by accident: costs have grown slower than gross profit and the company has systematically pushed for efficiency. Net profit rose from 0.2 billion in 2023 to 4.1 billion in 2024, 6.2 billion in 2025 and 7.5 billion in 2026.

The key detail for shareholders is "earnings per share" and working with the number of shares. Earnings per share rose from $0.21 in 2023 to $4.25 in 2024, $6.44 in 2025 and $7.85 in 2026. At the same time, the average number of shares declined (from roughly 992 million to 950 million), so the company is not only increasing earnings, but also translating some of the value into "per share" metrics via buybacks. Combined with the fact that it returned $14.3 billion to shareholders for 2026 and launched a new $50 billion buyback, it is clear that return on equity will be one of the main drivers of earnings in the years ahead.

And here's an important interpretation: Salesforce is no longer a "grow 20% a year" story. It's a story about being able to grow steadily, hold high margins, and return capital aggressively from cash. Moreover, if it can really accelerate organic growth in the second half of the year, it may change what "growth premium" the market is willing to pay. If it doesn't, there is still a very solid foundation of contract pipeline and cash strength.

News

The biggest news is that the company has started to publicly measure "how much work automated helpers can do in the system" and adds scale of use numbers (billions of units of work, trillions of tokens processed). For the investor, the only thing that matters is that Salesforce is trying to prove that AI is not just an extra feature, but a new revenue source that is already of measurable size (recurring annual revenue in the billions of dollars) and accelerating business activity (tens of thousands of contracts). The second innovation is purely capital-intensive: the new $50 billion buyout is a huge commitment that also suggests the company expects high cash generation over the long term.

The shareholder structure

Salesforce is a distinctly institutional title: the institution holds roughly 84% of the shares, and the insider stake is around 3%. The largest shareholders are Vanguard (roughly 9.6%) and BlackRock (roughly 8.6%), followed by State Street and Capital International. This typically means high liquidity, and also means that share price movement is sensitive to how large funds evaluate contract pipeline growth, margin stability, and rate of return on capital.

Analyst expectations

According to MarketBeat's summaries, the consensus is around a "slightly positive" recommendation and the average target price is roughly $300, with a wide range of estimates.

The practical interpretation: the market will continue to want proof that "AI in action" actually accelerates organic growth, not just marketing. In this report, Salesforce showed excellent cash and a record backlog of contracted sales. Now it will decide whether that translates into visibly faster growth in the coming quarters without the need to rely on acquisitions.