Target closed out the fourth quarter 2025 with results that accurately depict the company's current phase. On the one hand, we can see that demand for non-daily necessities remains soft and overall sales are down year-over-year, while on the other hand, the quality of the business is improving: gross margins were up in the quarter and the company is talking about better trends in home and core assortment compared to the third quarter. In addition, what Target has been building as a complementary engine over the past few years - revenue outside of actual merchandise sales, particularly from memberships, advertising and marketplaces - is accelerating. That's exactly the mix that can lift earnings faster than sales when demand stabilizes.

Management says 2025 has been a challenging year, but the company already says it saw "healthy, positive" sales growth in February, which sounds like an important turnaround in their communications. The outlook for 2026 is cautiously constructive: Target expects about 2% revenue growth, a slightly higher operating margin, and earnings per share in a fairly wide range of $7.50 to $8.50. In other words, it's not expected to rocket, but to return to growth mode and gradually improve profitability.

How was the last quarter?

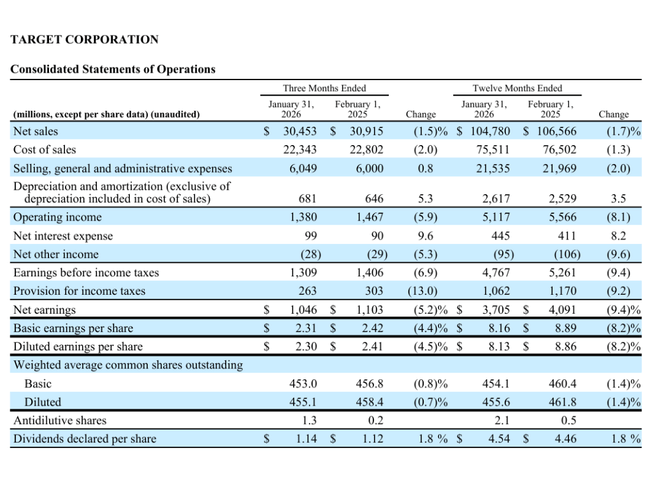

Target $TGT generated $30.453 billion in revenue in the fourth quarter, down 1.5% from a year ago. That's the key fact: the quarter didn't deliver a return to growth at the level of overall sales, but the company also says the result was in line with expectations and that sales and traffic accelerated in the last two months of the quarter. Meanwhile, the sales structure is more important than the number itself: the food and beverage, cosmetics and toy categories grew, and management points out that trends in the core assortment and home were better than in the third quarter.

Comparable sales were down 2.5%. This figure also explains why Target relies so heavily on digital and on revenue outside of actual merchandise sales. Sales in brick-and-mortar stores were weaker year-over-year (-3.9%), while the digital portion grew (+1.9%). In practice, this means that Target continues to shift to a model where delivery and pickup volumes are growing, but brick-and-mortar operations can't yet keep pace. The company reports that same-day delivery, supported by Target's Circle 360 membership, grew more than 30%.

At the quarter's profitability level, that doesn't look bad. Operating profit was $1.380 billion, down 5.9% year-over-year, but gross margin rose to 26.6% from 26.2%. There are specific reasons investors are interested: lower inventory losses, lower logistics and digital fulfillment costs, and growth in advertising and other services revenue. This was countered by higher costs of goods and imports and general pressure from trading activities.

Earnings per share were $2.30, compared with $2.44 after adjustments. An important detail is that the difference is $0.15 of one-time transformation costs. Thus: even though earnings per share were down slightly year-over-year, the company is trying to show that "under the surface" work is already underway to improve efficiency and prepare for a return to growth.

Highlights of the results

Fourth-quarter revenue of $30.5 billion, -1.5% year-over-year.

Comparable sales in the quarter -2.5%: stores -3.9%, digital +1.9%.

Earnings per share $2.30 on an accounting basis; $2.44 after adjustments (includes $0.15 of one-time transformation costs).

Operating profit in the quarter $1.38 billion, -5.9% year-over-year.

Gross margin in the quarter of 26.6% (from 26.2%), due to lower inventory losses, lower logistics costs and growth in advertising and other services revenue.

Full year 2025: sales of $104.8 billion(-1.7%) and net income of $3.7 billion(-9.4%).

FY 2025 dividend $4.54 per share, +1.8%; Q4 buybacks 0 and still $8.3 billion of authorized capacity remaining.

CEO commentary

CEO Michael Fiddelke' s commentary is not about triumph, but about turnaround and readiness. He says bluntly that 2025 was a challenging year, but the team is focused on serving customers while positioning for profitable growth in 2026 and beyond. A key phrase is the mention of "healthy, positive" revenue growth in February - management is signaling to investors that the trend may be breaking. And it also lists four pillars Target wants to play on: stronger authority in merchandise offerings, a better shopping experience, faster adoption of technology, and continued investment in employees and communities. This is typical language from a company that doesn't want to promise miracles, but wants to show that it has control over what it can influence.

Outlook

Target expects revenue growth of about 2% in 2026. Importantly, management says it wants revenue growth in every quarter of the year, and that more than one percentage point of growth is to come from new stores and revenue beyond just merchandise sales. This means that the company is betting on complementary "high-margin" areas - membership, advertising, marketplaces - and does not want to depend solely on the consumer returning to make more merchandise purchases.

On margins, management promises only a modest improvement: operating margin should be about 0.2 percentage points higher than the 2025 adjusted operating margin of 4.6%. That sounds modest, but in retail, even a small margin improvement on stable sales often has a significant impact on earnings per share. The company estimates earnings per share for 2026 of $7.50 to $8.50. The range is wide, and management is implicitly saying that the biggest uncertainty is in the timing of costs and how quickly demand and traffic will actually improve. The company also expects the first quarter to be more "spot on" profit-wise, with stronger earnings growth to come later in the year.

Long-term results

Target's long-term picture is one of a company that has experienced significant volatility in profitability in recent years, even as sales have remained relatively stable around the $100 billion mark. In 2022, it had sales of roughly 106.0 billion, but profitability was significantly higher (earnings per share of over $14), while in 2023 on similar sales (109.1 billion), earnings per share fell to six dollars. The year 2024 brought a return to better profitability (earnings per share around $9) and 2025 was slightly weaker profitably, although sales remained in a similar range. This shows that the key variable is not "how many sales" but what the mix is, what the discounts are, the cost of imports and logistics, and how much money is lost on inventory.

In 2025, sales dropped to $104.8 billion (-1.7%) and net income to $3.705 billion (-9.4%). Operating profit dropped to $5.117 billion (-8.1%). This doesn't look dramatic at first glance, but in retail, it quickly translates to earnings per share. Crucially, the company itself cited pressure from higher discounts and costs associated with order cancellations in 2025, while lower inventory losses and growth in advertising and other services revenue were positive.

Capital discipline is the second long-term theme. The share count has declined only slightly in recent years, and the company did not buy any shares at all in the fourth quarter of 2025, although it still has $8.3 billion in authorization. At the same time, the dividend remains stable, which was $4.54 per share in 2025, up 1.8% year-over-year. Thus, shareholder returns are primarily based on the dividend and whether the company will return to buybacks when it has more certainty about growth and margins.

News

The most interesting development in the report is the growing importance of revenue outside of traditional merchandise sales. The firm reports that these revenues grew by more than 25%, membership more than doubled year-over-year, advertising platform Roundel grew double digits, and marketplaces grew by more than 30%. These are exactly the sources of growth that can lift overall profitability in the years ahead, as they typically carry a higher margin than normal merchandise sales.

Shareholding structure

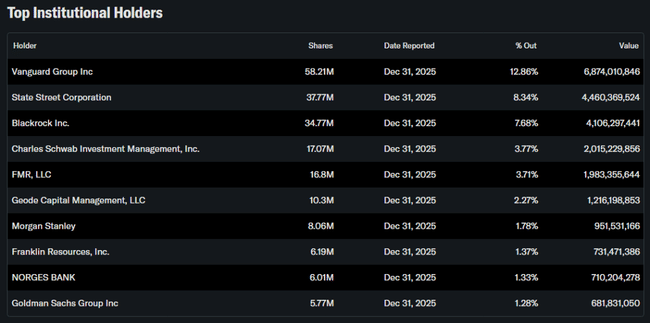

Target is a highly institutionally owned company: institutions hold roughly 86% of the stock and insider ownership is low. The largest holdings are Vanguard (about 12.9%), State Street (8.3%), BlackRock (7.7%) and Charles Schwab Investment Management (3.8%). This typically means high liquidity and sensitivity of the stock to how large funds view the consumer outlook, retail margins and interest rates.