Lockheed Martin's first quarter of 2026 looks rather unremarkable on the numbers, but strategically it is very strong. Revenues are at $18 billion, the same level as a year ago, operating profit and net income are down year-over-year, and free cash flow is slightly negative. But at the same time, the company is reaffirming its full-year outlook, presenting a backlog at record levels, and entering into framework agreements with the government to triple to quadruple production of key missiles and anti-aircraft systems over the next few years.

It adds a symbolically powerful moment in space. The Lockheed-built Orion capsule successfully completed the Artemis II mission, carrying the crew the farthest from Earth in history and returning them safely, strengthening the company's position in space programs.

Q1 2026 results

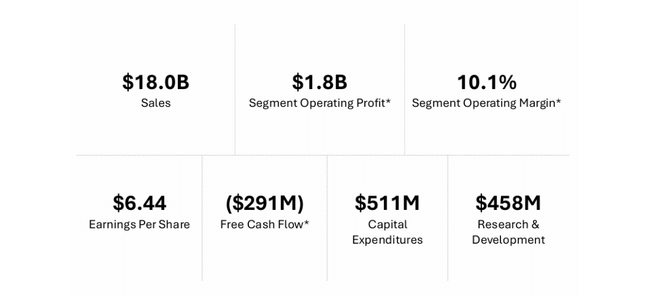

Lockheed Martin $LMT reported revenue of $18.02 billion in Q1 2026, virtually unchanged from $17.96 billion in Q1 2025. Meanwhile, analysts were expecting slightly higher revenue of around 18.38 billion, leaving the company slightly behind consensus on the top line.

Segment operating profit (business segment operating profit) was $1.82 billion, down from $2.09 billion a year ago, a drop of about thirteen percent. Total GAAP operating profit (including allocated items) was $2.06 billion, compared to $2.37 billion in last year's first quarter.

Net income was $1.49 billion, which translates to $6.44 per share, compared to $1.71 billion and $7.28 a year ago. Earnings per share are therefore down about twelve percent year-over-year, and the company has roughly met previous expectations that Q1 would be weaker than last year's very strong base.

Cash from operations was just $220 million in the quarter, compared to $1.4 billion last year. Free cash flow after capital expenditures ended negative $291 million compared to positive $955 million a year ago. Management explains this primarily by the timing of billing and working capital, not structural weakness, but in the eyes of investors this is one reason the stock is down several percent after the results.

In the quarter, Lockheed spent about $511 million on capital expenditures, $458 million on its own research and development, paid dividends of about $816 million and paid down $1 billion of long-term debt. In the short term, this puts pressure on cash flow, but in the long term it strengthens capacity and the balance sheet.

Results by segment

Aeronautics

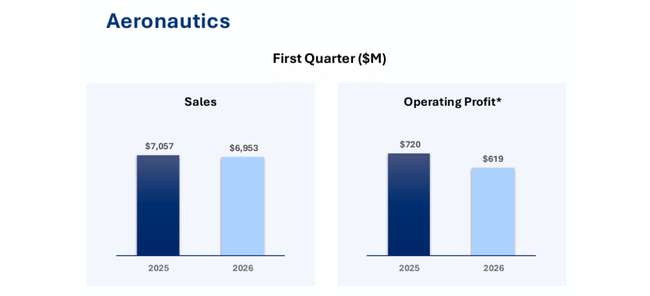

The Aeronautics segment had sales of $6.95 billion, down slightly from $7.06 billion a year ago. The decline was mainly due to lower volumes in classified programs and F-16s.

Revenue from classified programs was about $325 million lower due to lower volumes, and F-16 added approximately $145 million of the decline through a combination of lower production and unfavorable profit rate adjustments. These impacts were partially offset by growth in the F-35, where revenues increased about $325 million due to higher volume, primarily in maintenance and support contracts.

Aeronautics' operating profit fell to $619 million from $720 million, and margins declined to 8.9 percent from 10.2 percent. Profit booking rate adjustments, positive reserves for program profitability, declined. The $125 million negative adjustment on the F-16 was related to production problems and delays, while another $55 million of the unfavorable adjustment went to the C-130 due to supplier problems and delivery delays. In addition, it missed one-time favorable adjustments from last year on a classified program, which at the time lifted profits by about $80 million. This was partially offset by a higher positive adjustment on the F-35 of around $130 million, but the net effect was still negative.

Missiles and Fire Control

Missiles and Fire Control is the only segment to combine revenue and profit growth in Q1. Sales rose to $3.65 billion from $3.37 billion, up about eight percent. This is mainly due to the ramp-up of increased production of integrated air defense (PAC-3, THAAD) and tactical missiles (JASSM, LRASM, PrSM).

Operating profit rose to $500 million compared to $465 million last year, with margins holding around 13.7 percent. Growth reflects higher volumes, no large one-off items mentioned by the segment.

Rotary and Mission Systems

Revenue in the RMS segment fell to 3.99 billion from 4.33 billion, down about eight percent. This is due to lower volume in radar and systems parts and weaker performance in Sikorsky helicopters - particularly the CH-53K, Seahawk and Black Hawk programs.

Sikorsky suffered not only from lower volume but also from negative profitability adjustments due to production problems and delays, which translated into a significant drop in profits. RMS operating profit fell to 423 million from 521 million, and margins fell from 12.0 to 10.6 percent. Part of the decline is also due to the segment's one-time booking of about 50 million positive items from an intellectual property licensing deal in last year's first quarter, which did not recur this year.

Space

The Space segment had revenues of $3.43 billion versus $3.21 billion last year, an increase of about seven percent. The main growth drivers are strategic and missile defense programs, specifically the ballistic missile fleet and the next-generation interceptor NGI program.

But operating profit fell to 281 million compared to 379 million in last year's first quarter, and margins fell from 11.8 to 8.2 percent. This was again due to lower positive earnings adjustments. Last year, Space benefited from the favorable completion of some commercial civil space programs that produced significant one-time gains; nothing similar came this year.

Symbolically, however, the Space segment is boosted by the completion and successful mission of the Orion capsule as part of Artemis II. The Lockheed-built capsule returned a crew after a nearly 10-day mission around the Moon, during which it got farther from Earth than any previous manned mission. This mission reinforces the company's reputation as a key partner with NASA in the human lunar return program and preparations for a flight to Mars.

Management commentary and new framework agreement

In his comments, CEO Jim Taiclet builds Q1 on two pillars: proven capabilities in state-of-the-art defense and space, and new, "commercially inspired" long-term agreements with the government to substantially increase capabilities.

He mentions that the F-35 and F-22 are proving very effective in live deployments in challenging missions, and that the layered air defenses Lockheed is delivering - from radars to Aegis to THAAD to PAC-3 MSE - protect both military targets and civilians.

A key new development is the framework agreements with the U.S. War Department to increase production of munitions, particularly advanced versions of the Patriot, THAAD and PrSM missiles. These are multi-year frameworks that combine commitments for off-take with investment plans to expand production capacity. Taiclet says these agreements will allow production of critical missiles and interceptors to increase to three to four times current levels.

Importantly, from an investor's perspective, these contracts create demand visibility for many years ahead and give Lockheed room to invest in factories, supply chain and workforce with confidence that demand is assured. It's also a model that Taiclet says can become a model for future contracts in other areas - more long-term frameworks instead of short-term piecemeal contracts.

Outlook for 2026

Lockheed Martin's post-Q1 outlook for 2026 is confirmed. The company expects revenue in the range of $77.5 billion to $80 billion, which would represent growth of roughly five percent from $75.1 billion in 2025. Segment operating profit is expected to reach $8.43 billion to $8.68 billion, up roughly 25 percent from last year.

Including the pension FAS/CAS adjustment of about $1.36 billion, amortization of intangible assets and other items, total operating profit should reach about $9.4 billion to $9.7 billion. The company estimates earnings per share in the range of $29.35 to $30.25, up from $21.49 diluted earnings per share in 2025.

Cash from operations is expected to reach $9.15 billion to $9.45 billion, capital expenditures $2.5 billion to $2.8 billion and free cash flow $6.5 billion to $6.8 billion. A Q1 with negative free cash flow is more of a seasonal blip, not a new normal, and the company is counting on a traditionally stronger second to fourth quarter.

Overall, Lockheed says it expects roughly five percent revenue growth in 2026, significantly higher operating profit growth, and stable, very strong free cash flow to fund both investments and dividends and buybacks.

Long-term results

Revenue rises from roughly $66 billion in 2022 to $65.98 billion (technically a slight decline), then to $67.57 billion in 2023, $71.04 billion in 2024 and $75.06 billion in 2025. The growth rate has stabilized at about five percent per year in the last two years after covariance fluctuations, which is consistent with the gradual growth of defense budgets and contract increases, but also shows that this is not "meteoric" growth.

More interesting is the evolution of profitability. Gross profit was about $8.29 billion in 2022, hovered around $8.48 billion in 2023, but fell to $6.93 billion in 2024, only to rise again to $7.62 billion in 2025. This means that even though revenues grew, gross margin fell significantly in 2024, likely due to program mix, input inflation, pricing, and provisions for problems on specific contracts. 2025 then shows a return to better margins, albeit not to 2022 levels.

Operating profit, which for Lockheed equates to gross profit plus relatively small negative operating expenses, increased from 8.35 billion in 2022 to 8.51 billion in 2023, but fell to 7.01 billion in 2024 and returned to growth to 7.73 billion in 2025. Profit before tax, after rising to 8.10 billion in 2023, fell to 6.22 billion in 2024 and 5.92 billion in 2025. Net profit follows this pattern, falling from 6.92 billion in 2023 to 5.34 billion in 2024 and 5.02 billion in 2025.

Earnings per share rise from $21.74 in 2022 to $27.65 in 2023, up more than a quarter, but then fall to 22.39 in 2024 and 21.56 in 2025. Some of the EPS decline is dampened by buybacks as the number of shares gradually declines from roughly 264.6 million diluted shares in 2022 to 231.9 million in 2025.

Overall, Lockheed's revenue growth has been accelerating slightly in recent years, but profitability is flying more due to program mix, one-time profitability adjustments, and macro cost pressures. EPS trend looks like: strong growth in 2023, then a two-year cooling. So the 2026 outlook with expected EPS around $29-30 represents a significant re-acceleration of earnings if it can be met.

Shareholders

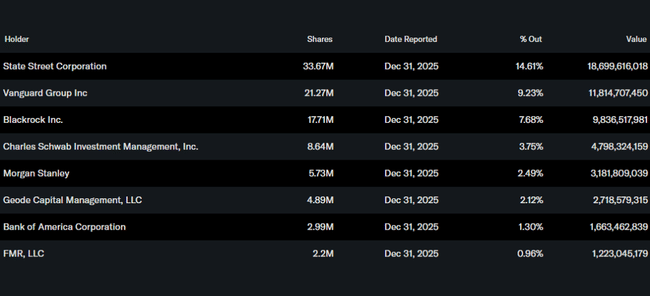

Lockheed Martin is a textbook example of an institutionally owned title. Insiders hold only about 0.1 percent of the stock, according to Yahoo Finance, while the institution owns about 75 percent of the stock and free float. In total, over three thousand two hundred institutions hold shares.

The largest shareholders are State Street with about 14.6 percent, Vanguard with 9.2 percent, BlackRock with 7.7 percent, Charles Schwab Investment Management with 3.8 percent and Morgan Stanley with 2.5 percent. That said, the mood around the title is set by a few large houses, which often hold it as a core position in the defensive sector.

Lockheed has traditionally combined dividend and buybacks. In February 2026, it announced the year's first dividend of $3.45 per share payable at the end of March, in line with its history of gradual dividend increases. At a price of around $540 to $560, the dividend yield is in the roughly two to three percent range, plus the effect of buybacks that gradually reduce the number of shares outstanding and support EPS growth.

News and strategic direction

In addition to Orion and the munitions framework contracts, other new developments include air defence contracts. Lockheed was recently awarded a $4.7 billion contract to continue accelerated production of the PAC-3 MSE, which follows a framework agreement with the War Department and is expected to enable a threefold increase in interceptor production over the next few years.

The company is also continuing to invest in upgrading its production lines, digitizing production and expanding capabilities for missiles, radars and other key elements of layered defense. Restructuring within RMS (moving programs into new SEMS and MIC2 lines) is intended to enable faster delivery of integrated solutions to customers and better connect sensors, effectors and command and control.

In the long term, this profiles Lockheed as a company that stands not just on one "flagship" type, the F-35, but on a broader portfolio of systems - from aircraft to missiles to command and control systems to space technologies. Q1 2026 shows that in the short term, profitability may fluctuate depending on the status of specific programs, but demand for major systems is growing and new framework agreements and contracts are creating great visibility for the years ahead.

For the investor, this means that Lockheed today is not a classic growth title, but rather a stable defense mainstay with moderate revenue growth, more volatility in profitability, and very strong cash flow that management is translating into dividends, buybacks, and capacity enhancements in a world where defense budgets are growing rather than shrinking.