Visa had another strong quarter, confirming that cashless payments continue to grow across the economy, even in an environment of higher rates and geopolitical uncertainty. Consumers remain active, corporate payments are gaining momentum and international transactions are benefiting from continued travel and trade. At the same time, the company is aggressively returning capital to shareholders - the combination of dividends and buybacks totaled $9.2 billion this quarter alone, and the board added a new $20 billion buyback program.

In terms of strategy, Visa continues to strengthen its role as a "payments infrastructure": expanding Visa as a Service, adding AI and stablecoin capabilities, while also strengthening its presence in emerging markets such as Argentina through acquisitions. The company is thus building a position not only in consumer cards, but also in commercial payments and business-to-business and institutional cash flows, giving it a broader base for growth in the years ahead.

Q2 2026 results: growth across all major lines

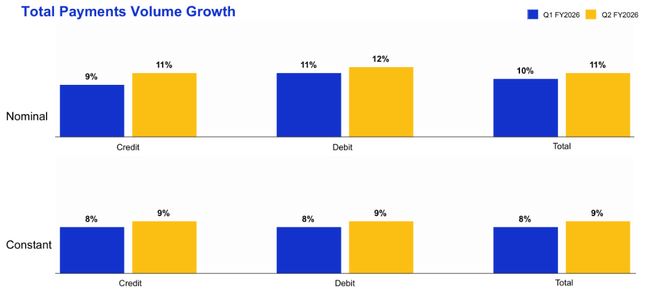

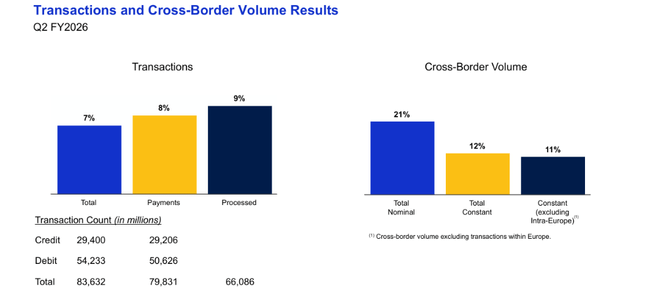

In the second fiscal quarter of 2026, Visa's net sales grew to $11.2 billion, up 17% year-on-year, or 16% after adjusting for currency effects. This was driven by a combination of higher payment volumes, strong cross-border traffic and growth in the number of processed transactions, with constant currency payment volume up 9%, total cross-border volume up 12% and the number of processed transactions reaching 66.1 billion, up 9% from a year ago.

The profitability shows a double effect: solid revenue growth, and the normalisation of extraordinary litigation costs. GAAP net income increased 32% year-over-year to $6.0 billion and GAAP earnings per share jumped 36% to $3.14, with last year's quarter burdened by a significantly higher litigation provision. Filtering out these one-time items, non-GAAP net income was $6.3 billion (+17% y/y) and non-GAAP EPS was $3.31 (+20% y/y), growing slightly faster than revenue alone.

The revenue structure shows that Visa $V is growing not just "on volume" but also in value-added services. Revenue from services related to payment volume grew 13% to $5.0 billion, data processing revenue grew 18% to $5.5 billion, and international transactions added 10% to $3.6 billion. The fastest growing category was other revenue, which shot up 41% to $1.3 billion - typically newer services and higher value-added solutions. Client incentives, which partially dampen these revenues, grew 14% to $4.2 billion, slower than total revenues, which is positive from a margin perspective.

On the expense side, GAAP operating expenses fell 4% to $4.0 billion, mainly due to lower litigation provisioning - $329 million this year versus $1 billion a year ago. On an adjusted basis, however, operating expenses were up 17% as Visa added money in people and marketing to drive payment volume growth and adoption of new services. As a result, operating profit rose significantly to $7.2 billion and maintained very high operating margins, among the most attractive in the financial sector.

Key Figures:

Net revenue was $11.2 billion, up 17% year-over-year, or 16% when adjusted for currency effects.

GAAP net income rose to $6.0 billion (+32% y/y), GAAP earnings per share (EPS) to $3.14 (+36% y/y).

Adjusted for extraordinary items (litigation, acquisition amortization, investments), non-GAAP net income was $6.3 billion (+17% y/y) and non-GAAP EPS was $3.31 (+20% y/y).

Key volume metrics behind the revenue growth:

Payments volume grew 9% in the quarter at constant currency.

Total cross-border volume increased by 12%.

Processed transactions amounted to 66.1 billion, 9% more than a year ago.

The revenue structure shows that growth is very balanced:

Service revenue: USD 5.0 billion, +13% y/y - based on the previous quarter's payment volume.

Data processing revenue: USD 5.5 billion, +18% y/y - benefiting from higher transaction volumes and more complex services.

International transaction revenue: USD 3.6bn, +10% y/y - growth mainly driven by cross-border payments.

Other revenue: USD 1.3bn, +41% y/y - growing rapidly, likely due to value-added services and new solutions.

Client incentives: USD 4.2bn, +14% y/y - growing but slower than revenue, which is positive for margins.

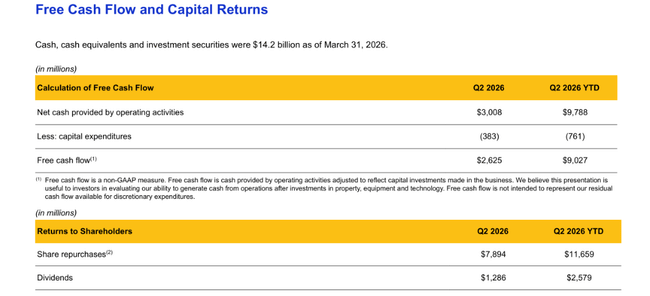

Cash flow, balance sheet and capital allocation

Visa remains exceptionally profitable at the cash flow level:

For the first six months of fiscal 2026, the company generated net income of $11.9 billion and operating cash flow of $9.8 billion.

As of the end of March 2026, it had cash, equivalents and investment securities of $14.2 billion.

The balance sheet structure remains very strong, although there has been a significant increase in debt and a concurrent reduction in cash:

Long-term debt increased from USD 19.6 billion to USD 22.4 billion (thanks, among other things, to the new USD 3 billion of senior notes with fixed rates of 3.8-4.7% and maturities of 3-10 years).

Cash and cash equivalents fell from USD 17.2bn to USD 12.4bn, partly due to aggressive share buybacks and dividend payments.

Capital allocation is strongly pro-shareholder:

Visa repurchased approximately 25 million Class A shares for $7.9 billion in the quarter, at an average price of $320.66 per share.

Total dividend and buyback spending reached $9.2 billion in the quarter alone.

As of March 31, 2026, the company still had $13.2 billion under its existing buyback authorization, and in April 2026, the board approved a new multi-year buyback program for an additional $20 billion.

At the same time, a quarterly dividend of $0.67 per A share was declared, payable on 1 June 2026.

Also of interest is the $125 million dividend. A USD 125 million deposit into a litigation escrow account to protect the company and Class A shareholders from the impact of select litigation - the account has a similar effect to the buyback by reducing the number of Class B-1 and Class B-2 shares.

Strategic moves, acquisitions and capital structure

Visa continued to pursue strategic transactions during the quarter:

It completed the acquisition of Prisma Medios de Pago S.A.U. and Newpay S.A.U. in Argentina, strengthening its role in card processing, real-time payments and ATM network (Banelco) and payment gateway (PagoMisCuentas).

The aim is to modernize the payment infrastructure and strengthen its position in emerging markets where there is a large scope for a shift from cash to digital payments.

Another structural step is the offer to exchange Class B-1 and B-2 shares for a combination of Class B-3 and C shares and possibly cash for fractional shares. This move has implications for the shareholder base structure and may gradually increase the liquidity and transparency of the capital structure, although for the average investor this is more of a technical issue.

Management commentary and outlook

CEO Ryan McInerney described the 17% revenue growth as the fastest since 2022 and highlighted that it was driven by resilient consumer demand as well as the success of the strategy in consumer payments, commercial solutions and money movement and value-added services. From management's perspective, this is therefore broad-based growth, not a one-off effect of one segment or region.

In addition, Visa further developed its "Visa as a Service" services in the quarter, adding agent-based AI and stablecoin functionality. The aim is to consolidate its position as a payments "hyperscaler" - a global platform on which an increasing proportion of the world's payment flows run, both in traditional cards and new forms of digital payments.

In terms of outlook (guidance), the company mentions two main lines in the materials presented:

Short-term: continued growth in payment and transaction volumes, although the pace may be sensitive to macroeconomics, travel and consumer confidence.

Long-term: expanding from a pure card network to a role as a comprehensive payments and cash flow infrastructure, including collaboration with fintechs and banks.

What's in it for the investor

Fundamentally, the quarter was very strong: double-digit revenue growth, significantly higher profits, high margins and solid volume growth across all key metrics.

In addition, the company is showing great confidence in its future - massive buybacks, a new $20 billion authorization, a steadily growing dividend and investment in technology.

Higher non-GAAP expenses (+17%) suggest Visa is consciously investing in people, marketing and innovation to stay ahead in an environment where competition from fintechs, alternative networks and regulation is growing.

From an investment perspective, the results support the thesis that Visa remains a quality growth stock with elements of blue-chip defensiveness - the business is highly profitable, capital-light and has a long structural growth story. The short-term trajectory will depend largely on market expectations for volume growth and regulation, but the Q2 2026 numbers alone tend to make the case for why Visa can afford to combine earnings growth with generous capital returns to shareholders over the long term.