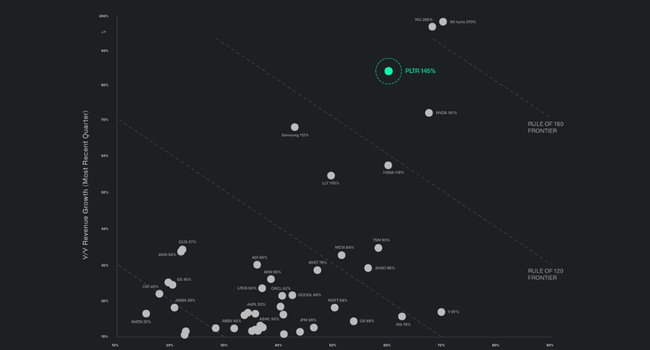

Palantir just posted the kind of quarter you normally expect from an early‑stage SaaS name, not from a scaled enterprise platform: revenue jumped 85% year on year, U.S. revenue more than doubled and U.S. commercial sales grew 133%. At the same time, the company printed a 60% adjusted operating margin, 57% adjusted free‑cash‑flow margin and 53% GAAP net‑income margin on 871 million dollars of profit, pushing its Rule‑of‑40 score to an unprecedented 145% – a level otherwise seen only at a handful of top AI‑infrastructure chip makers.

Management isn't afraid to raise its full-year revenue outlook to roughly 70 percent growth, and it promises at least a doubling of revenue in its U.S. commercial business. That's not a cosmetic upgrade of a few percentage points, but a clear message: what we're seeing in Q1 has a sequel.

Q1 2026 results: an explosion of growth and profitability

Palantir $PLTR earned $1.63 billion in Q1 2026, up 85% year-over-year and about 16% quarter-over-quarter. This is the highest year-over-year revenue growth in the company's history. U.S. revenue more than doubled to $1.28 billion, growing 104% year-over-year and 19% quarter-over-quarter.

Inside the U.S., both major segments grew:

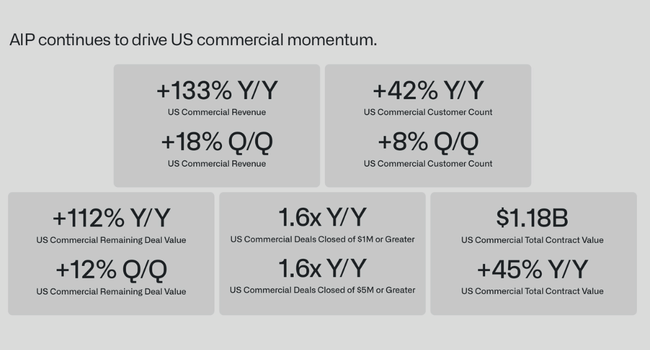

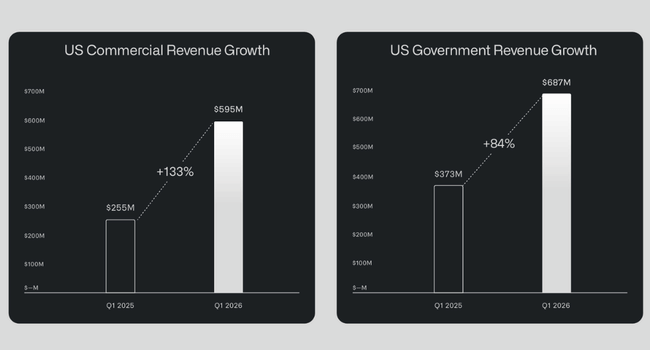

U.S. commercial grew 133% year-on-year to $595 million and 18% quarter-on-quarter

U.S. government business grew 84% year-on-year to USD 687 million and 21% quarter-on-quarter

The entire business thus combined extreme growth with high profitability: GAAP income from operations reached $754 million, an operating margin of 46%. Adjusted income from operations was $984 million, a 60% margin. GAAP net income was $871 million (53% net margin) and adjusted net income to common shareholders was $856 million.

At the earnings per share level, Palantir reported GAAP EPS of $0.34 and adjusted EPS of $0.33, with consensus around $0.28 - a beat of roughly 18%. Adjusted EBITDA came in at $990 million, a 61% margin. Cash from operations was $899 million (55% margin) and adjusted free cash flow was $925 million (57% margin). At the end of the quarter, the company held $8.0 billion in cash, equivalents and short-term U.S. Treasuries and still does not have the traditional long-term debt of most large software competitors.

Thus, the Rule of 40, which is calculated as the sum of revenue growth and adjusted operating margin, comes out to 145% (85% revenue growth plus roughly 60% adjusted operating margin). This is a number that virtually no large software/AI player achieves at this revenue scale - even the top SaaS players tend to be happy with 60-80%.

Palantir's share price drops slightly after the results as the market has pretty much had a hyper-growth scenario priced in and attention immediately turns to valuation. Even though the company delivered record numbers - 85% revenue growth, extremely high margins and a significantly raised outlook - some investors are taking advantage of the situation to realize gains after the previous rally and some are concerned that the current multiples (at both revenue and earnings levels) leave little room for error. Thus, the results are not a punishment for weak fundamentals, but rather a reminder that even great reports can lead to short-term price pressure for extremely overpriced AI titles if they don't deliver "something more" than already inflated expectations.

Trading dynamics: TCV, RDV and deal flow

In addition to the headline numbers, the basis in contracts is also important:

Total contract value (TCV) was $2.41 billion, up 61% year-on-year

U.S. commercial TCV was $1.176 billion, +45% year-over-year

Palantir closed 206 contracts with a value of at least $1 million, 72 contracts with a value of at least $5 million and 47 contracts with a value of at least $10 million. This shows that growth is not just about a few mega-deals, but a wide spread across medium and large companies.

Remaining deal value (RDV) in U.S. commercial reached $4.92 billion, up 112% year-over-year and 12% quarter-over-quarter. In other words, the pipeline of contracts already signed in the U.S. commercial segment more than doubled over the year. This is key, because U.S. commercial is at the heart of Palantir's AI growth story outside of government and military.

Management Commentary

Alex Karp describes the quarter as a "phase shift" in the company's history. He highlights three key theses:

Palantir is going from a small, controversial company to an AI infrastructure player that measures up to names like Nvidia, Micron, SK hynix - not in chips, but in software, data layer, and AI workflow orchestration.

Almost all AI workflows that generate real value, "especially on the battlefield", he says, run on Palantir - the company is "N of 1", a unique entity in its segment.

Product and business efficiencies are growing dramatically: Karp reports that annual revenue per employee has approached roughly $1.5 million, an extremely high number for an enterprise of this size.

At the product level, the core of the story is the AIP (Artificial Intelligence Platform) and the so-called agent workflows - that is, the AI agents that run on top of client data at Palantir and connect the models to real decisions and operations (defense, industrial, healthcare, financial). Palantir strives to be the "operating OS" for AI in critical and regulated industries where a language model is not enough, but security, auditing, governance and interfacing with existing systems is needed.

There is a rapidly growing demand for end-to-end solutions in U.S. commercial firms: it's not just selling licenses, but also pilot rollout, subsequent scaling and sometimes even participation in outcomes (outcome-based contracts). In the U.S. government segment, Palantir continues to benefit from contracts in defense, intelligence, and security, where AI workflows permeate planning, logistics, and tactics.

Outlook

Palantir significantly raises its outlook for Q2 2026 and the full year:

Q2 2026 Outlook:

Revenue in the range of $1.797 billion to $1.801 billion

adjusted operating income of $1.063 billion to $1.067 billion

FY 2026 Outlook:

Full-year revenue newly $7.650 billion to $7.662 billion, equivalent to roughly 71% growth, and 10 percentage points higher than the previous outlook

U.S. commercial sales to reach at least $3.224 billion, a growth of at least 120%

adjusted operating income of $4.440 billion to $4.452 billion

adjusted free cash flow of $4.2 billion to $4.4 billion

Management also expects positive GAAP operating income and net income in each quarter of 2026

For the investor, this means that Palantir sees Q1 not as an anomaly, but as the beginning of a new trajectory: rapidly growing AI infrastructure in the US (commercial and government sectors), high margins, and very strong conversion of profits to cash flow. In an environment where some AI software is still burning cash, the combination of 70% growth and FCF margins around 60% is extremely rare.

News

In the quarter, Palantir announced some visible news: on the product side, it is further expanding its AIP and agent AI workflows and entering into major new partnerships with companies such as Airbus, GE Aerospace, Stellantis and consulting house Bain, who will use its platform to deploy generative AI in manufacturing, logistics and business management.

On the business side, the news is mainly the explosion of the U.S. commercial segment - Palantir explicitly says U.S. commercial is now the main driver and that U.S. remaining deal value there has jumped to $4.92 billion, more than double from last year.

There's also an interesting shift in who the firm is doing business with: alongside traditional government and defense clients, there are large "blue-chip" industry players, as well as tech firms, including Nvidia, that Palantir is using to orchestrate its own AI use-cases. Finally, for the first time, Karp directly puts Palantir in the same sentence as Nvidia, Micron and SK hynix as "AI infrastructure" companies in this way - a clear attempt to rewrite the brand perception from "government software" to the core AI stack.

What to take away from Palantir Q1 2026

Palantir has effectively moved into the league of AI infrastructure "monsters", where it is both growing rapidly and generating exceptionally high margins - the combination of 85% growth and 60% operating margin is unique for a company of this size.

The U.S. business is now the core of the story - 104% growth in U.S. commercial, 133% in U.S. commercial and 84% in U.S. government - and both RDV and TCV suggest the pipeline is strong for the quarters ahead.

The outlook for 71% revenue growth in 2026 and 120% U.S. commercial revenue growth shows that management is confident in the continuation of the "AI supercycle" around Palantir.

But the stock is far from cheap - the dispute over valuation is likely to become a major issue in the months ahead, while the fundamental numbers so far look almost flawless.