Disney delivered solid numbers in its fiscal second quarter, confirming that the "big reboot" under its new strategic plan is starting to work. Revenues rose 7% to $25.2 billion, total segment operating profit increased 4% to $4.6 billion and slightly beat earlier guidance, primarily due to stronger-than-expected revenue growth.

Management openly says the key to success is hidden in the second half of the fiscal year: Disney expects adjusted EPS growth of about 12% in full fiscal 2026, is targeting at least $8 billion in share buybacks, and is guiding investors to expect segment operating profit of about $5.3 billion for Q3. The combination of a better-than-expected Q2, a bright growth outlook for H2 and reports of healthy demand in domestic parks, albeit with a caveat of macro uncertainty, is exactly the mix that is sending the stock higher after a prolonged period of skepticism following earnings.

Q2 numbers: revenue growth and stable segments

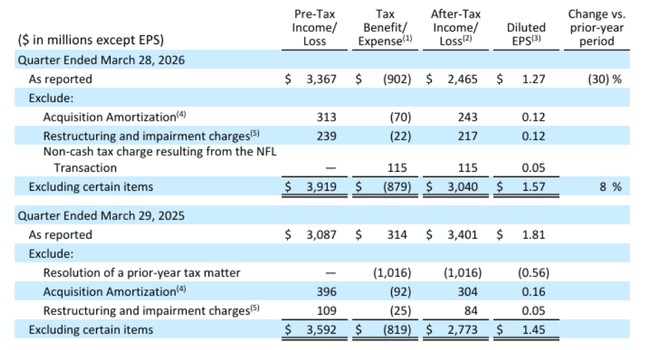

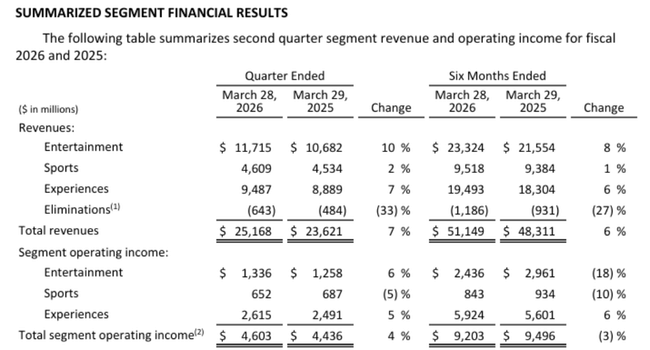

For Q2 FY 2026, Disney earned $DIS of $25.2 billion, up 7% from $23.6 billion a year ago. Pre-tax income rose 9% to $3.37 billion. Total segment operating profit increased to $4.60 billion (+4%), with all three key segments - Entertainment, Sports and Experiences - contributing, albeit to varying degrees.

For the first half of the fiscal year, revenue is $51.1 billion (+6%), but segment profit is slightly below last year (-3%), which management describes as a transitional effect of investments and realignments to bring acceleration in the rest of the year.

Cash flow from operations in Q2 was $6.9 billion (+2%), free cash flow $4.94 billion (+1%). Despite the year-over-year decline in FCF for the first half (2.66 vs. 5.63 billion), Disney is clearly communicating that capital discipline and the ability to generate cash remain solid pillars - but at the same time, increased investment in content, technology and expanding Experiences is running.

Segments.

Entertainment

The Entertainment segment increased revenue 10% to $11.7 billion, segment operating profit rose 6% to $1.34 billion. Driven mainly by streaming (Disney+, Hulu and related services): the so-called Entertainment SVOD earned 13% more y-o-y, with growth faster than in Q1 (11%), driven mainly by a better monetization mix after price increases, higher volume momentum and new international wholesale agreements.

Importantly, Disney delivered its first double-digit Entertainment SVOD operating margin this quarter and still expects at least a 10% margin for the full fiscal year 2026. In other words, streaming is no longer just a "black hole for cash" but is becoming a robust margin business that is starting to fully replace gradually declining linear TV revenues. Management explicitly says that today Disney already generates more subscription/affiliate fee and advertising revenue from SVOD than from linear TV - the mix has definitely flipped.

Sports (ESPN)

The sports segment earned $4.61 billion (+2%), segment operating profit, but fell to $652 million (-5%). Subscription and affiliate revenue growth of 6% was driven in part by the NFL transaction (about 3 percentage points), which also increased costs and non-controlling interest. Advertising revenue at ESPN was down 2% due to comparisons to last year's major sporting events (more NBA games, 4 Nations in hockey).

Importantly from a strategy perspective, digital (DTC) subscription revenues are already fully offsetting the secondary decline in linear subscriptions. ESPN Unlimited (a DTC offering launched last year) is starting to gain traction and the company is expanding content and product, working with DraftKings, among others, to more deeply integrate wagering into the ESPN ecosystem.

Experiences

Experiences (parks, resorts, cruise, other physical experiences) grew revenue 7% to $9.49 billion and segment profit 5% to $2.62 billion - record numbers for Q2. Per capita spending at domestic parks was up 5%, mainly due to higher revenue from admissions, dining and shopping. Global "guest count" (parks + cruise passenger days) was up 2% year-over-year.

Domestic visitation was down 1%, but management attributes this mainly to continued weaker international visitation - year-over-year comparisons should improve in future quarters. In addition, results were weighed down by the cost of Disney Adventure and World of Frozen (roughly -2 percentage points of segment profit growth), with these new assets expected to drag growth in the years ahead.

CEO commentary

Commenting on the results, Josh D'Amaro stressed that the company is "halfway there" - some of the changes are already showing up in the numbers, but the main effect should come in the second half of the year. He said Disney is "uniquely positioned" in that it reaches fans simultaneously in both the digital and physical worlds: from streaming to sports and games to parks and cruises, and the goal is to leverage that breadth to drive more fan engagement and higher revenue from existing content and brands.

He listed the top three priorities as:

Maintain the creative quality and strength of brands (movies, TV shows, franchises)

Deepen the direct relationship with fans by making Disney+ the "digital centre" of the entire ecosystem (connecting stories, experiences, games and commerce)

and make greater use of technology, including artificial intelligence, to better target content, personalise and operate more efficiently

Why the stock is rising: outlook, buybacks, streaming and Experiences

Why is the share price gaining after earnings?

Earnings Outlook - The company insists it will grow adjusted EPS by roughly 12% (excluding the 53rd week) and 16% including the 53rd week in full fiscal 2026. It also projects double-digit growth again in 2027, giving the market a "two-year" growth window story, not just one quarter.

Return on Equity - Targeting at least $8 billion of buybacks in 2026 is an aggressive signal that management believes in both undervaluing the stock and sustaining cash flows.

Streaming story - Entertainment SVOD is growing faster than expected and showing double-digit operating margins for the first time. The revenue mix is shifting to DTC, which at the same time is not "subsidized" in a cash-burning way.

Experiences - record Q2 numbers, growth in per-capita spend and strong Disney Adventure bookings (new ship in Singapore) along with a World of Frozen-type expansion in Paris and planned projects in Japan and Abu Dhabi reinforce the long-term story of IP monetization in the physical world.

Together, these paint a more compelling picture than a year ago: that Disney is not just a "legacy media house" but a combination of profitable streaming, a premium sports ecosystem (ESPN) and global physical experiences with high return on capital. The stock is responding to the fact that the quarterly numbers are not just "OK" but fit into a consistent framework of earnings growth, FCF and buybacks.