Don't expect improvement all of 2023, warns one of Wall Street's most important companies with strong arguments

The market is like a roller coaster this year. Huge drops alternate with sharp upward movements. Personalities and companies are racing to make positive and negative predictions. Often unfounded. That's not the case with the latest prediction from the Wall Street financial giant.

If you are on the positive side of the barricade and believe that the market will soon turn for the better, then you probably won't like Goldman's report. Especially if you believe that the Fed and rate cuts will be the catalyst for thoto turnaround.

"We doubt that the inflation path we project for next year would be sufficient to provide such confidence in a rate cut,"Goldman's chief economist Jan Hatzius wrote in a note.

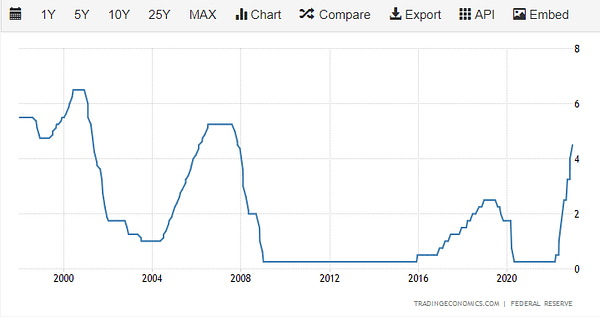

The Fed surprised in two ways on Wednesday after raising interest rates by 50 basis points, taking the benchmark rate to its highest level since 2007.

The Fed's economic forecasts now show it sees rates peaking at 5.1% in 2023. That's another 50 basis points higher than projected back in September. And of course such news hurt the market.

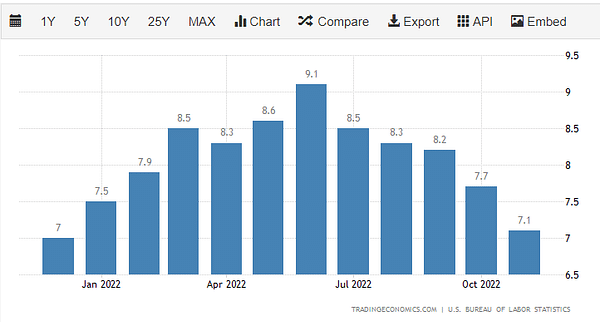

Moreover - Fed chief Jerome Powell sounded a bit more hawkish on the direction of interest rate policy than some had expected. There was increasing talk that the Fed would raise rates by only 25 basis points at its February 2023 meeting in the face of cooling consumer price index (CPI) and slowing labor market growth.

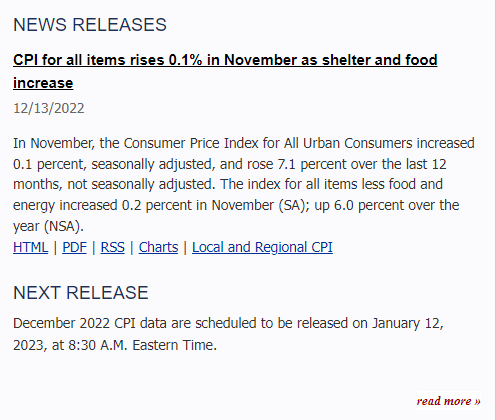

Powell basically completely dispelled this talk, which put stocks under pressure into Wednesday's close and early Thursday trading. "Inflation data received so far for October and November show a welcome reduction in the monthly rate of price increases," Powell told reporters at a conference after the Fed's decision. "However, substantially more evidence will be needed to give us confidence that inflation is on a sustained downward path."

Goldman's Hatzius models three more 25 basis point rate hikes in February, March and May. Hatzius projects that the peak in interest rates for this cycle is 5% to 5.25%.

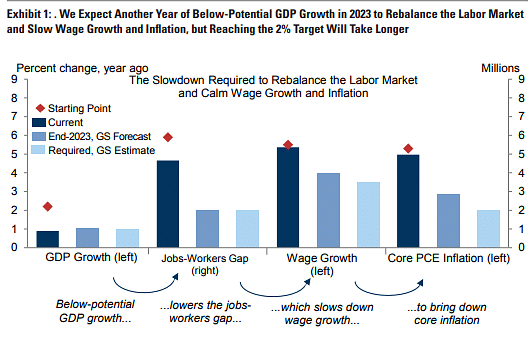

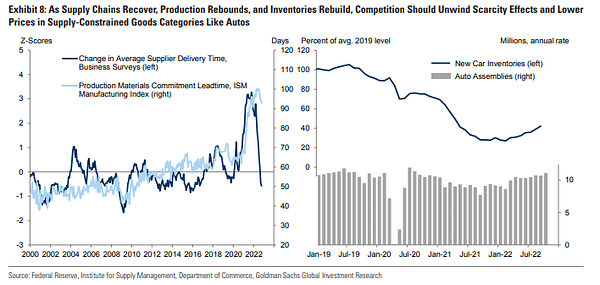

But they also mention the positives. For it seems that at least the supply chain recovery is finally delivering the deflationary signs that can't and won't come due to a host of other pandemic and war influences. As production of goods (especially automobiles)recovers and inventories are restored, competition should reverse the effects of scarcity that raised retail prices and consumer prices at the beginning of the pandemic. In addition, commodity prices are moderating and transport costs are falling.

If you enjoy my articles and interviews, feel free to throw a follow. Thanks! 🔥

Disclaimer: This is in no way an investment recommendation. This is purely my summary and analysis based on data from the internet and other sources(GS, Tradingeconomics.com, bls.gov). Investing in financial markets is risky and everyone should invest based on their own decisions. I am just an amateur sharing my opinions.