As much of the software sector oscillates between optimism and cost discipline, Adobe continues to operate from a position of structural advantage. The company is not chasing artificial intelligence as a standalone narrative, nor is it defending a legacy model under threat. Instead, Q4 2025 shows a business that is steadily integrating AI into products customers already depend on, reinforcing pricing power rather than undermining it.

What stands out is the breadth of Adobe’s relevance. Creative tools remain central, but enterprise workflows, document management, and productivity solutions now play an equally important role in long-term value creation. In an environment where many software firms struggle to prove durable monetization, Adobe demonstrates that AI can deepen customer lock-in instead of commoditizing the platform.

How was the last quarter?

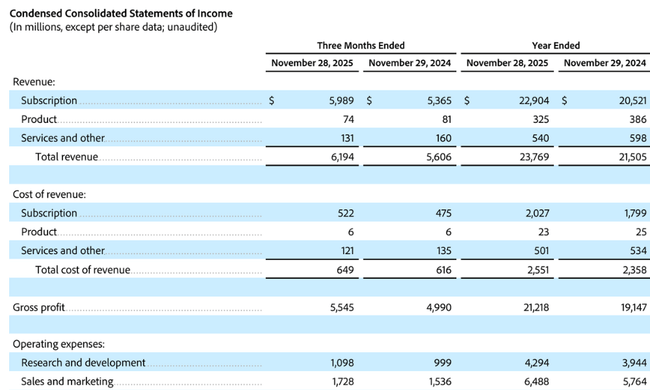

The fourth fiscal quarter delivered another record performancefor $ADBE and confirmed the stability of Adobe's business model across segments. Revenues were $6.19 billion, up 10% year-over-year, with consistent growth both in absolute terms and when adjusted for currency effects. Crucially, growth was not driven by one-off factors but by the continued expansion of subscriber relationships across customer groups.

Operating profitability remained at a very high level. GAAP operating profit was $2.26 billion, while non-GAAP operating profit was $2.82 billion. Net income on a GAAP basis was $1.86 billion and non-GAAP was $2.29 billion. Diluted earnings per share were $4.45 (GAAP) and $5.50 (non-GAAP), confirming the company's ability to translate revenue growth into profitability growth even with continued investment in AI and new platform development.

Cash performance was also a very strong signal. Operating cash flow in the quarter reached a record $3.16 billion, again underscoring the quality of the subscriber model and the low capital intensity of the business. Importantly, in terms of future revenue visibility, remaining contractual obligations (RCOs) reached US$22.52 billion, with 65% attributable to short-term obligations, indicating strong short and medium-term demand.

In terms of segments, Digital Media remains the main driver, generating US$4.62 billion in revenue in the quarter, up 11% year-on-year. Digital Experience added US$1.52 billion, representing 9% growth, with subscriptions in this segment alone growing by as much as 11%. The growth structure thus confirms that Adobe is not dependent on a single product, but benefits from a whole platform of interconnected tools.

CEO comments

CEO Shantanu Narayen in his comments, highlighted that the record results for the full fiscal year and the strong fourth quarter reflect Adobe's growing importance in the global AI ecosystem. He said the company is benefiting from the rapid adoption of AI tools across creative professionals and enterprise customers, and is succeeding in integrating generative and agent-based AI directly into products that customers use every day. The key message here was not about experimentation, but about the practical monetization of AI features within existing platforms.

CFO Dan Durn followed up with an emphasis on quality growth and cost discipline. He highlighted the strong global demand for Adobe's AI solutions across customer groups and expressed a high level of confidence in the company's ability to continue to deliver double-digit ARR growth in 2026 while maintaining top-line profitability. It is clear from his comments that management views the current developments not as the top of a cycle, but as a transition to the next phase of growth.

Outlook

The outlook for fiscal 2026 looks confident and consistent with the company's current pace. Adobe expects total revenues in the range of $25.9 billion to $26.1 billion and year-over-year growth in total ARR of approximately 10.2%. Management is also targeting continued subscription growth in both major customer groups, with the Business Professionals & Consumers segment expected to grow the fastest.

Profitability should remain very strong, with non-GAAP operating margin expected to be around 45% and non-GAAP earnings per share in the range of $23.30 to $23.50. For the first quarter of fiscal 2026, the company expects revenue of $6.25 billion to $6.30 billion and continued earnings per share growth. Importantly, the outlook also does not include the potential benefit of the planned acquisition, suggesting a conservative approach to forecasts.

Long-term results

The long-term performance shows an extremely stable and high-quality growth profile, which is still the exception rather than the rule for a company of this size. Total revenues have increased from approximately $15.8 billion to $21.5 billion over the past four fiscal years, which corresponds to continuous year-on-year growth in the range of around 10-11%. This is not a cyclical fluctuation, but a systematic trend that is supported by the expansion of the subscriber model across all major product lines and geographies.

Even more important than revenue growth itself is the evolution of the cost structure and gross margins. Cost of sales is growing at a significantly slower rate than revenue, which translates into accelerated gross profit growth over the long term. It increased from around USD 13,9 billion to more than USD 19,1 billion over the period under review. Thus, gross margin has not only remained at a very high level but has even improved slightly over time, confirming strong pricing, low demand elasticity and the ability to translate higher product value into prices.

At the level of operating performance, the company's strategic shift over the last two years is evident. Operating expenses are growing faster than revenues, mainly due to massive investments in development, AI infrastructure, data capabilities and product platform expansion. This is reflected in a slowdown in the rate of growth of operating profit, which is increasing by rather low single-digit percentages. Importantly, however, this is not an erosion of margins caused by market pressures, but a conscious decision by management to sacrifice some of the short-term momentum in favour of a long-term competitive advantage.

Nevertheless, net profit and earnings per share continue to grow at a steady pace. Net income has moved from about $4.8 billion to $5.6 billion, with EPS growth accelerating even faster thanks to a systematic reduction in the number of shares outstanding. The average number of shares outstanding has declined by about 2-3% each year, amplifying the effect of profitability growth on shareholders over the long term and confirming a disciplined approach to capital allocation.

Cash generation remains a great strength. EBITDA has grown from around US$6.7 billion to almost US$8 billion over four years, with a consistent growth rate that follows the overall development of the business. This has allowed the company to simultaneously fund heavy investment in development, make large share buybacks and maintain a very robust balance sheet without the need for significant debt.

News

In addition to the results themselves, Adobe also announced changes to its reporting starting in fiscal 2026. The company will focus more on reporting growth in total ARR and subscriptions by customer group, reflecting a shift in strategy toward long-term customer relationships and better transparency on key metrics. At the same time, there has been a revaluation of end ARR due to currency exchange rates, which has increased the baseline ARR entering 2026.

Shareholding structure

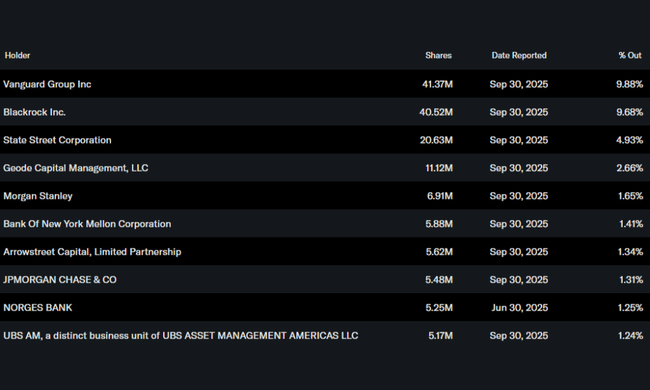

Adobe's shareholder structure is typical of a high-quality technology company with a global reach. Institutional investors hold more than 86% of the shares, with Vanguard Group, BlackRock and State Street among the largest shareholders. The high proportion of institutional capital indicates the confidence of long-term investors in the business model, strategy and the company's ability to generate stable returns. The proportion of insiders is very low, which is common for a firm of this size.

Analysts' expectations

The consensus of analysts perceives Adobe as one of the highest quality software companies in the market. Expectations focus on the firm's ability to sustain double-digit ARR growth over the long term, monetize AI features without disrupting existing pricing models, and maintain above-normal margins. Adobe is often viewed as a defensive growth title that combines stability with long-term growth potential, which is reflected in the market's willingness to accept premium valuations.