AMD closed out 2025 with a strong fourth quarter, confirming that its transformation toward high-performance AI and data platforms has subtly translated into solid financial results. Revenues exceeded market expectations at a record $10.3 billion, and the 34% year-over-year growth reflects growing demand for EPYC processors for servers, Ryzen CPUs for client segments, and the booming Instinct platform for data center and AI workloads. AMD is thus undoubtedly among the technology winners of the ongoing wave of AI adoption in the enterprise sector.

But on the other hand, 2025 has also revealed some structural limits, especially in the area of gross margins and dependence on the Chinese market for GPUs, where regulatory constraints still represent a variable with a significant impact on the composition of results. Still, the CEO's comments suggest that the company enters 2026 with "strong momentum" and expects further expansion of its high-performance and AI platforms.

Quarterly results

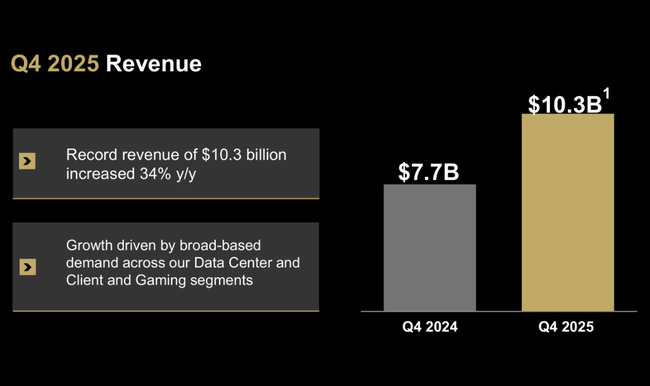

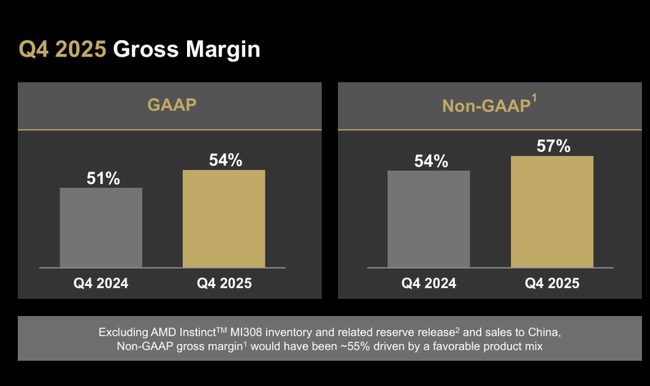

For Q4 2025, AMD $AMD achieved revenue of $10.27 billion, up 34% year-over-year and a higher quarterly number than the $9.25 billion in Q3 2025. Gross margin increased to 54%, up from 51% in Q4 2024 and a relatively strong Q3 2025, which saw a 3 percentage point improvement. This shows that the company is succeeding in scaling up production and improving product mix, despite increasing competition.

Profitability grew even more strongly. GAAP operating income reached $1.75 billion, up 101% YoY, and operating margin moved from 11% to 17%. Net income more than tripled to $1.51 billion, delivering EPS of $0.92, +217% YoY. On a non-GAAP basis, which removes some one-time items and volatile components, results were even stronger: operating profit of $2.85 billion(+41% YoY) and record EPS of $1.53, up 40%.

Segmentally, the Data Center division was the most dynamic, generating $5.4 billion in Q4 revenue (+39% YoY) driven by growing deployments of EPYC server CPUs and Instinct GPUs for AI workloads. The Client & Gaming segment grew 37% to USD 3.9bn, with the Client business alone leading the way with +34% revenue growth driven by strong demand for Ryzen CPUs and partial market share gains. The Embedded division grew only modestly (+3%), still a solid result given the long-term order cycle and seasonal effects.

In addition, AMD benefited from a one-time effect of the Instinct MI308 inventory rebooking of approximately $360 million in the quarter, which positively impacted gross margin - without it, non-GAAP gross margin would have been around 55%.

Outlook and positioning for 2026

Management, led by Dr. Lisa Su, remains optimistic about future developments. For Q1 2026, AMD expects revenue of approximately $9.8 billion ± $300 million, which would imply year-on-year growth of around 32%, although there would be a weaker seasonal decline across quarters. Non-GAAP gross margin is expected to be around 55%, confirming the stability of the margin structure even without Q4 one-off effects.

CEO commentary on the results

Management's commentary was significantly upbeat in tone, but at the same time did not deliver a new near-term catalyst, which the market was expecting after a strong run-up. Lisa Su called 2025 "defining" due to record revenue and profitability, and highlighted the accelerating adoption of EPYC processors and the rapid scaling of the AI datacenter business. She repeatedly highlighted the long-term potential of AI platforms and strong demand across segments, particularly in data centers.

However, from a market perspective, it is key that management has not scaled the near-term outlook. Instead, it confirmed sequential revenue decline in Q1 2026 (~-5% q/q) and highlighted seasonality and regulatory constraints around exports to China. Despite management talking about "strong momentum into 2026", for investors focused on the coming quarters, this was more about confirming a familiar story, not accelerating it.

Long-term results

AMD's long-term results show a clear trend of transformation from a traditional semiconductor manufacturer into a high-performance and AI-accelerated business. Between 2021 and 2025, revenues will undergo a dramatic transformation: from $16.4 billion in 2021 to a record $34.6 billion in 2025, corresponding to an average annual growth of over 20%. The fastest growth has been seen in the last two years, when demand for datacenter and AI solutions has become a key driver.

Gross profit increased from $7.9 billion to over $18 billion on a non-GAAP basis during the same period, although there was a one percentage point decline in non-GAAP gross margin in 2025 due to changes in product mix and one-time factors (e.g., export restrictions on certain GPU products to China). Operating expenses grew less steeply than sales, allowing operating profit to increase significantly from several hundred million in 2023 to over $7.7 billion in 2025 on a non-GAAP basis.

Profits and cash flow grew even more dynamically. GAAP net income rose from $854 million in 2023 to over $4.3 billion in 2025, and EPS increased from ~$0.53 to ~$2.65 over the same horizon. Thus, over the long term, AMD is weathering cyclical downturns and demonstrating its ability to translate market share and technology demand directly into results.

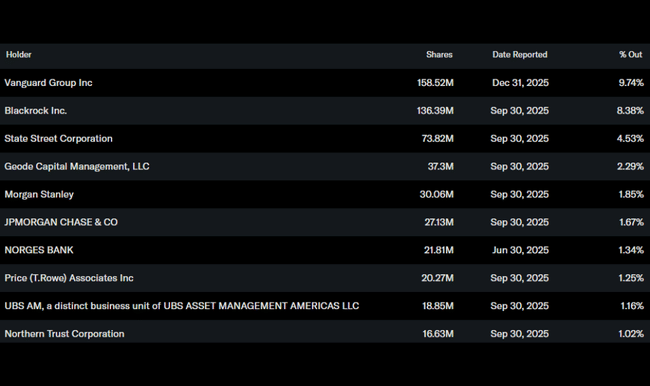

Shareholder Structure

The majority of the stock is held by institutions (~70%), with traditional asset managers such as Vanguard (~9.7%), BlackRock (~8.4%), and State Street (~4.5%) among the largest holders. The low insider ownership (only ~0.44%) is consistent with the broad institutional distribution base, and the risk profile of the stock then primarily reflects market dynamics and technology expectations, rather than significant short-term management behavior.

Analyst expectations and Wall Street reaction

Following the earnings release, analyst consensus did not deteriorate fundamentally, but sentiment shifted in a more cautious direction due to the outlook. Analysts appreciated the record Q4 and exceptional margins in the AI segment, but also cautioned that Q1 guidance implies a slowdown in growth rates, which increases the risk of a near-term correction after strong growth in the stock.

For example, Morgan Stanley analysts said after the results that AMD remains a long-term AI infrastructure winner, but the stock may "suffer from the absence of a positive surprise in guidance" in the coming quarters.