2025 highlighted a subtle but important shift in Novo Nordisk’s growth profile. Volumes continued to expand at a strong pace and constant-currency revenue growth remained robust, confirming that demand for obesity and diabetes therapies is still structurally strong. At the same time, pricing pressure and regulatory dynamics—particularly in the US—started to play a more visible role in reported results, softening the headline picture.

Investors are now looking beyond growth itself. The key questions center on how effectively higher volumes can offset price compression, whether oral Wegovy can unlock a new wave of demand, and how resilient the pipeline is as competition intensifies. The year confirms Novo’s strength, but it also signals that the next phase will be less forgiving on margins.

How was 2025?

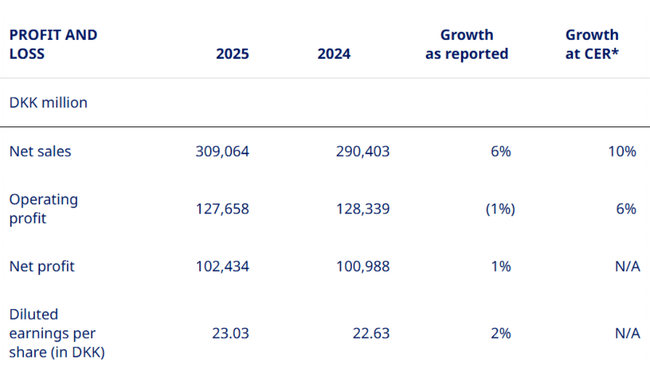

For the full year 2025, sales were approximately US$44.8 billion, which corresponds to year-on-year growth of 6% and 10% respectively at constant exchange rates. The difference between these two figures is important - the stronger Danish krone dampened reported growth, while real demand remained robust.

Operating profit was around USD 18.5 billion, down 1% year-on-year in reported currency but up 6% when adjusted for currency effects. The key negative factor was one-off transformation costs of around USD 1.2 billion, without which operating profit would have grown at a double-digit rate even in reported currency. As a result, despite the pressure, the operating margin remained very high at approximately 41%, which continues to make Novo Nordisk one of the most profitable pharmaceutical companies in the world.

Net profit was approximately USD 14.8 billion, up approximately 1% year-on-year, while earnings per share (EPS) rose 2% to approximately USD 3.34. Profitability thus remained stable, but it is clear that the rate of earnings growth has lagged significantly behind the rate of revenue growth - exactly the signal that the market is sensitive to.

In terms of segments, growth was driven primarily by obesity care, where sales grew 26%, driven by Wegova's continued global expansion. GLP-1 diabetes treatment grew at a low single-digit rate, confirming the gradual saturation of traditional markets. Rare diseases added a solid 5%, acting as a portfolio stabilizer.

CEO commentary

Commenting on the results, Mike Doustdar openly admitted that 2025 was a challenging year for the company in terms of the pricing environment, particularly in the US where price adjustments, Most Favoured Nations agreements and impending patent expiries in some international regions are all impacting results.

However, he also stressed that the company was very encouraged by the rapid take-up of oral Wegova in the US, where the number of weekly prescriptions reached around 50,000 within weeks of launch. Management, he said, remains confident that the combination of new dosage forms, higher doses and a new generation of molecules will allow it to grow patient numbers and overall volumes over the long term, even if the pricing environment remains under pressure.

Outlook for 2026

The outlook is a major reason why investors are cautious. Adjusted revenue growth (excluding the impact of the one-time reserve reversal in the 340B program) is projected to be -5% to -13% in 2026 at constant currencies. In reported currency, growth is expected to be roughly 3 percentage points lower, implying very weak to negative headline growth.

Similarly, adjusted operating profit is expected to fall in the range of -5% to -13% at CER. On the positive side, the planned reserve release of around USD 4.2 billion under the US 340B programme will improve both revenue and profit in the short term, but this is a one-off accounting effect, not a structural improvement.

At the same time, management expects the global GLP-1 market to continue to grow rapidly, and Novo Nordisk intends to capture this growth with oral Wegova, higher doses of the injectable form and the phased ramp-up of CagriSem.

Long-term results

Between 2021 and 2024, Novo Nordisk's revenues grew from approximately US$20.4 billion to US$42.1 billion, more than doubling in four years. This growth has been driven almost entirely by an explosion in demand for GLP-1 drugs, particularly in obesity, where the company has established a virtually dominant position.

Operating profit grew from roughly US$8.5 billion to US$18.6 billion over the same period, with margins hovering above 40% over the long term. This shows the company's extraordinary pricing power in previous years. This is why the current slowdown is being viewed so sensitively - investors are used to a combination of high growth and extreme margins that is increasingly difficult to sustain.

Earnings per share between 2021 and 2024 grew from around $1.50 to $3.30, with growth supported not only by operating performance but also by systematic share count reductions. This trend continues now, although the rate of EPS growth is clearly slowing.

News

The most significant event is the approval and launch of oral Wegova in the US, which may change the structure of the obesity treatment market in the long term. In addition, the company successfully completed a Phase 3 study of CagriSema in diabetes and submitted a higher dose of semaglutide 7.2mg to the FDA, expanding future offerings.

The Phase 2 results with zenagamtide were also of interest in the research area, showing significant weight and HbA1c reductions, confirming the potential of the next generation of molecules.

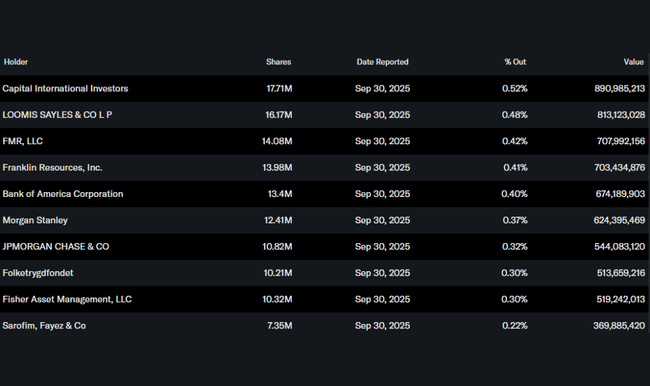

Shareholding structure

The shareholding structure remains stable and strongly institutional, with long-term investors such as Capital International Investors, FMR and Franklin Resources dominating. This suggests long-term confidence in the investment story, despite short-term fluctuations.

Analyst expectations

Analysts at the major banks agree that Novo Nordisk remains a structural winner in the obesity market, but caution on valuation pressure due to a weaker outlook for 2026. For example, Goldman Sachs analysts said after the results that the firm still has a unique pipeline and volume potential, but expect higher volatility and slower earnings growth in the short term. Target prices are mostly above current levels, but with an emphasis on the long term.