Moderna enters 2026 with an ambition to return to growth, but the reality of the Q4 and full-year 2025 numbers shows a company in transition. Revenues continue to decline due to the downturn in the covide business, losses remain significant and the cash cushion is gradually thinning. While management talks of "strong momentum" and up to 10% revenue growth in 2026, the key question remains whether new products and pipeline can make up for the pandemic revenue shortfall.

Quarterly results confirm continued cost restructuring and more disciplined expense management. For investors, not only the development of seasonal vaccine sales is now critical, but more importantly the success of regulatory processes and clinical data to determine whether Moderna can transform itself from a "covid company" to a full-fledged mRNA platform with diversified revenue.

How was the last quarter?

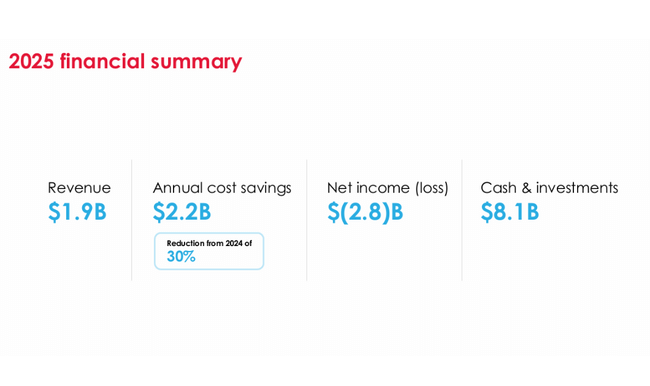

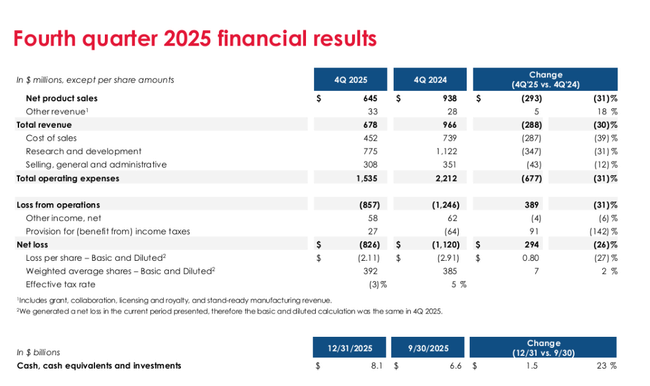

In the fourth quarter of 2025, Moderna's revenue was $678 million, down 30% year-over-year from $966 million in the same period in 2024. Covid vaccine sales remained the main source of revenue, with net product sales of $645 million, including $264 million in the U.S. and $381 million in international markets. Other revenues amounted to USD 33 million.

Cost of goods sold was $452 million, including $34 million of royalties to third parties and $144 million of inventory amortization. These costs decreased 39% year-over-year, primarily due to lower contract termination costs and lower inventory write-downs.

Research and development (R&D) was US$775 million, down 31% from US$1.122 billion in Q4 2024. The company continues to reduce spending as it completes large Phase 3 respiratory studies and as part of its portfolio prioritisation. SG&A operating expenses were $308 million, down 12% year-on-year.

Total operating expenses were $1.535 billion, resulting in an operating loss of $857 million on revenue of $678 million. Net loss for the quarter was $826 million, compared to a loss of $1.12 billion a year earlier. The loss per share was USD -2.11 (vs. USD -2.91 in Q4 2024). So while the loss margin is improving, the business remains deep in the red.

Gross margin in the quarter was approximately 33% (US$678m sales minus US$452m cost of sales), reflecting weaker volumes and pressure on manufacturing efficiency.

Full year 2025 in numbers

For the full year 2025, Moderna generated revenue of US$1.944 billion, down 40% from US$3.236 billion in 2024. Of this, US$1.818 billion was product revenue and US$126 million was other revenue. The US contributed US$1.2 billion and international markets US$745 million.

Cost of goods sold was $868 million (down 41%), R&D expenses were $3.132 billion (down 31%) and SG&A was $1.018 billion (down 13%). Total operating expenses were $5.018 billion.

Operating loss for the year was $3.074 billion, net loss was $2.822 billion, compared to $3.561 billion in 2024. Loss per share was -$7.26 (vs. -$9.28 in 2024). The improvement is noticeable, but the company remains significantly loss-making.

Cash, cash equivalents and investments as of 12/31/2025 were $8.1 billion (vs. $9.5 billion a year earlier). This included a $600 million drawdown on a $1.5 billion line of credit. The decrease in cash is primarily due to continued losses and pipeline investments.

CEO comment

Stéphane Bancel highlighted that the company has reduced annual operating costs by approximately $2.2 billion in 2025, significantly exceeding internal targets. At the same time, it launched a third commercial product and opened three new manufacturing plants outside the US.

Moderna enters 2026 with "strong momentum," according to management, expecting up to 10% revenue growth from mNEXSPIKE expansion and international partnerships. The CEO also points to the potential of several regulatory decisions and clinical data in Phase 2 and 3 that could fundamentally change the company's revenue profile.

Outlook for 2026

Moderna is targeting up to 10% revenue growth from 2025, roughly towards a level of around $2.1 billion. Revenue is expected to be split approximately 50% US and 50% international markets.

Expected Costs:

Cost of sales: approximately $0.9 billion

R&D: approximately USD 3.0 billion

SG&A: approximately USD 1.0 billion

Capex: USD 0.2-0.3 billion

The company expects a negligible tax charge and an ending cash position of between USD 5.5-6.0 billion at the end of 2026 (without further drawdowns on the credit facility). This implies continued cash outflow, albeit at a slower pace.

Long-term results

The evolution of recent years illustrates the dramatic transformation of the company. In 2021, Moderna $MRNA will reach $17.7 billion in sales and $12.2 billion in net profit, and even $18.9 billion in sales and $8.36 billion in net profit in 2022. EPS at the time was over $20.

The year 2023 marked a sharp turning point: revenues fell to USD 6.8 billion and the company plunged to a net loss of USD 4.7 billion. This was followed by a further drop in 2024, with sales falling to USD 3.2 billion and a loss of USD 3.56 billion.

The collapse in revenue is almost entirely related to the decline in global demand for covid vaccines. At the same time, however, Moderna dramatically increased R&D spending - from $1.8 billion in 2021 to more than $6 billion in 2023.

News

In infectious diseases, the review of the combined influenza and COVID vaccine continues in Europe and Canada. However, for the standalone flu vaccine, the company has received a Refusal-to-File letter from the FDA and has requested a Type A meeting to clarify the way forward.

The norovirus vaccine (mRNA-1403) has a fully enrolled Phase 3 trial, with data expected in 2026. In oncology, a collaboration with Merck continues on a personalized vaccine, mRNA-4157 (intismeran autogene), where the combination with Keytruda reduced the risk of recurrence or death by 49% in a Phase 2b study in melanoma compared to Keytruda alone. Phase 3 data are expected potentially in 2026.

Shareholding structure

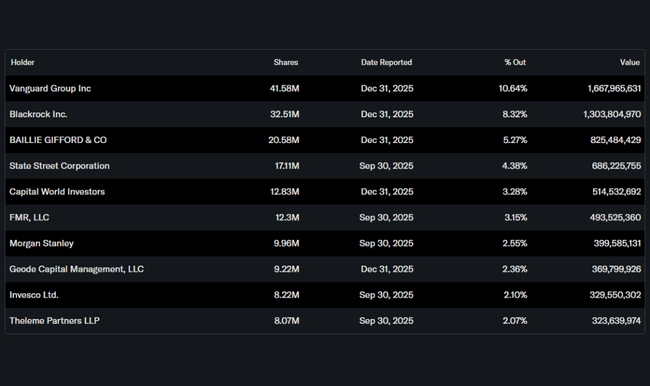

The shareholder structure shows strong institutional dominance. Approximately 75% of shares are held by institutions and more than 81% of free float is held by institutions. The largest shareholders include Vanguard (10.6%), BlackRock (8.3%), Baillie Gifford (5.3%) and State Street (4.4%). Insiders hold approximately 7.4% of the shares, which is a relatively high proportion and indicates some alignment of management interests with shareholders.

Analysts' expectations

Analysts are watching two key factors in particular: the success of the combination respiratory vaccine and the pace of cash burn. The consensus focuses on whether the company can actually achieve the promised up to 10% revenue growth in 2026 while stabilizing its operating loss. The stock's valuation thus remains primarily a function of expectations for future clinical milestones, not current profitability.