After the COVID boom and bust, Pfizer’s story is no longer about headline comparisons. Investors now focus on whether the company can stabilize its core business, improve earnings quality, and show a credible plan that leads to sustainable growth later in the decade. Q4 and full-year 2025 do not look dramatic on the surface, but they read as a step toward a more predictable base.

The more important context is what 2025 represented. It was a transition year in which the COVID revenue decline was fully absorbed and the growth narrative shifted back to the standard levers of big pharma: portfolio performance, pipeline progress, and disciplined capital allocation. Viewed through that lens, the results look less like weakness and more like consolidation before the next cycle.

How was the last quarter?

The fourth quarter of 2025 delivered revenues of $17.6 billion, down 1% year-over-year on a reported basis and down 3% on an operating basis. On the face of it, this is a weak result, but the revenue structure is significantly better than the aggregate number suggests. The main negative remains the continued decline in the covide products Comirnata and Paxlovid, but this was largely offset by solid growth in the key non-covide drugs. Adjusting for these, Pfizer $PFE s quarterly revenues rose 9% operationally, which is more material information for investors than the decline itself.

Profitability remained under pressure in the quarter. Pfizer posted a reported loss per share of $-0.29, while adjusted earnings per share came in at $0.66, up 5% year-over-year. The difference between the reported and adjusted numbers is again a reminder that the company is still undergoing restructuring, cost optimization and integration of earlier acquisitions. From a long-term investor's perspective, the trend in adjusted EPS is more important than the short-term volatility of reported results.

At the product level, the quarter clearly showed where Pfizer's growth pillars lie today. Abrysvo vaccine posted 136% year-over-year operating revenue growth, driven by indication expansion and international expansion. Oncology biosimilars grew 76%, mainly driven by price mix in the US. Eliquis added 8%, driven by strong global demand and favorable pricing in the U.S. following changes to Medicare Part D. The Prevnar family of vaccines also posted solid growth, driven primarily by the expansion of CDC recommendations in the U.S. for the 50-64 age group.

CEO commentary

In his comments, CEO Albert Bourla made it clear that 2025 was about execution and setting the stage for the next growth phase. He said Pfizer strengthened its fundamentals in 2025, stabilized cash flow and prepared the pipeline for a period when new key products will start to materialize. From management's perspective, 2026 is set to be a catalyst-rich year, particularly with around 20 key pivot study launches planned.

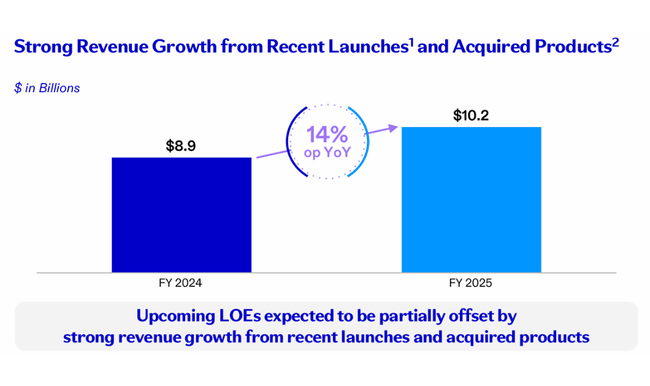

CFO David Denton added an emphasis on financial discipline. He highlighted that the non-covid portfolio delivered 6% operating revenue growth in 2025 and that cost control had enabled growth in adjusted EPS despite an unfavourable revenue mix. Management is thus making it clear to investors that Pfizer does not want to grow at any cost, but is building a return to growth on a combination of pipeline, selective investment and disciplined capital allocation.

Outlook

Pfizer confirmed full-year guidance for 2026. Revenue is expected to be in the range of $59.5 billion to $62.5 billion, with roughly $5 billion still expected to come from covid products. Adjusted earnings per share are expected to be in the range of $2.80 to $3.00, implying relative stability in profitability compared to 2025.

The outlook also reflects several structural factors. The company anticipates a negative impact of approximately $1.5 billion from the loss of exclusivity on select drugs, a higher tax rate, and adverse regulatory impacts including most-favored-nation pricing and tariff actions. On the other hand, Pfizer is planning R&D investments of $10.5 billion to $11.5 billion and continued pipeline strengthening, which is expected to be a major value driver beyond 2027.

Long-term results

A long-term view of Pfizer's financial performance clearly illustrates the extreme cyclicality of recent years. 2022 was the strongest year historically due to a peak in covenant revenue, with sales exceeding $100 billion and operating profit reaching nearly $38 billion. However, this peak was clearly unsustainable and subsequent years have brought a sharp normalisation.

By 2023, revenues had fallen by more than 40% to just under $60 billion and operating profit had fallen by almost 86%. 2024 had already brought stabilisation and a modest recovery, with revenues rising to $63.6 billion and operating profit more than tripling to $16.5 billion. These developments indicate that the worst of the downturn is likely behind the company, although a return to the pre-crisis trajectory will not be rapid or linear.

Earnings per share confirm this story. EPS is gradually improving after the collapse in 2023, but still remains well below 2021-2022 levels. A positive sign is the relative stability in the number of shares outstanding, suggesting that the firm is not yet diluting shareholders and maintaining flexibility for future capital decisions.

Shareholder structure

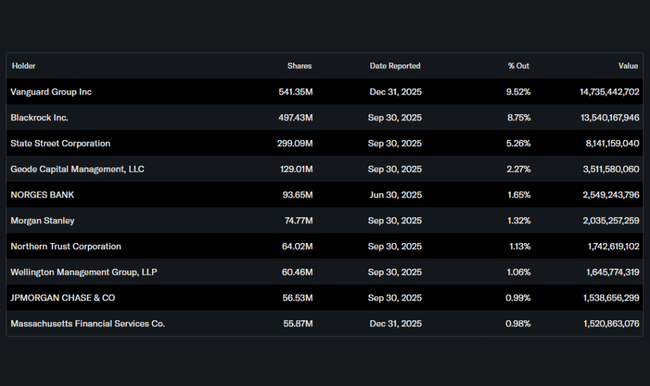

Pfizer's shareholder structure remains highly institutional. Approximately 68% of shares are held by institutional investors, with Vanguard, BlackRock and State Street being the largest owners. The share of insiders is negligible, which is typical for pharmaceutical giants of this size. The stable institutional base suggests that Pfizer continues to be viewed as a long-term defensive component of portfolios, not a short-term speculative title.

Analyst expectations

The analyst consensus is gradually shifting from skepticism to cautious optimism for Pfizer. The major investment houses view 2026 as a transition year, with limited earnings growth but increasing pipeline visibility beyond 2027. In particular, analysts highlight the potential of late-stage clinical trials in obesity, oncology and immunology, and management's ability to sustain the dividend in a period of lower earnings.

Target prices are mostly in the range of moderate to moderate growth potential, with regulatory pressure on US drug prices and uncertainty around the success of individual clinical programs remaining key risks. Thus, for investors, Pfizer today represents a story of a gradual return to growth rather than an immediate turnaround.