In oil and gas, the market often pays for visibility, not for a single strong print. When prices are lower than last year, investors want proof that a company can defend cash generation through operating discipline. A quarter can look excellent and still leave the stock flat if the next quarter carries disruption risk.

Devon’s Q4 2025 made the “discipline” case. It generated $702 million of free cash flow, delivered production above the high end of guidance, and kept unit costs moving down. The income statement was solid too, with adjusted EPS of $0.82 on $4.12 billion of revenue. The cautious tone comes from what follows: Q1 2026 volumes are expected to take a hit from extreme weather, realized oil prices remain lower than a year ago, and investors are still trying to frame what Devon becomes after the Coterra combination.

How was the last quarter?

Devon $DVN posted a net profit of $562 million in Q4 2025. USD 562, or USD 0.90 per share. Adjusting for items that analysts typically exclude, "core" earnings came in at $510 million. USD 0.82 per share. The just-adjusted profit was very close to the market consensus and was mainly supported by operating performance, not a one-off accounting effect.

At the revenue level, the company reported $4.12 billion, down roughly 6% year-over-year, consistent with realized oil prices being noticeably weaker in the quarter than a year ago. Reuters reports an average realized oil price of $34.52 per barrel versus $40.32 a year earlier, which naturally puts pressure on overall revenue and the margin profile if the company offsets the price pressure with higher volumes and savings.

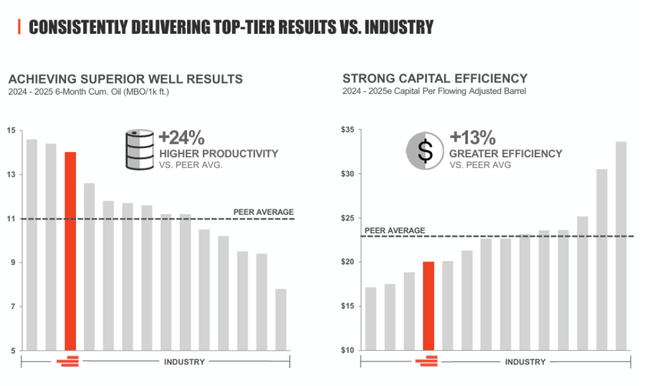

Volumes, on the other hand, have been a strength. Total production came in at 851k boe/d, beating the top end of guidance; oil alone was 390k b/d and represented 46% of the mix. In practical terms, this means that Devon has been able to squeeze more out of the highest quality parts of its portfolio in a lower price environment, particularly in the Delaware Basin, where the report cites above-average performance from new wells.

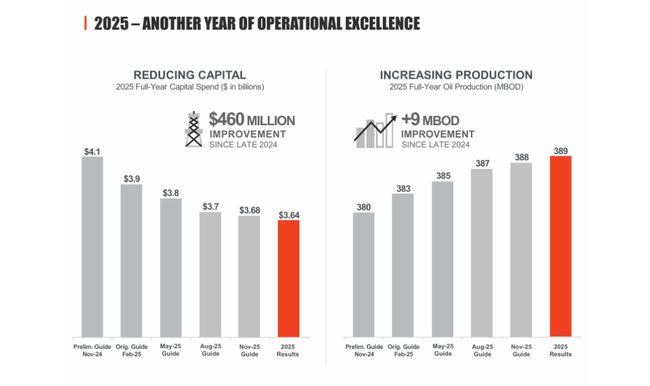

Cash flow is key investment language for Devon. Operating cash flow in the quarter was $1.5 billion and free cash flow was $702 million. The company still invested actively. Capital expenditures excluding the acquisition component were $883 million. Capital expenditures were USD 88 million, about 4% below the midpoint of guidance, which management attributed to a combination of cost management and timing of some infrastructure investments. In other words, operating leverage was evident in the quarter: high volumes + lower unit costs can stabilize cash flow even in a weaker pricing environment.

Another important point is the cost side. Production costs including taxes fell to USD 10.99/boe, 4% lower than in the third quarter. The largest item - a combination of operating and transportation/processing costs - was $8.60/boe, about 3% better than the company's expectations. This is a valuable signal to investors as it shows that the cost savings program is not just a presentation, but translates into real unit metrics.

The balance sheet remains conservative. At the end of the quarter, the company had cash of $1.4 billion, an undrawn credit line of $3 billion, total debt of $8.4 billion and a net debt to EBITDAX ratio of 0.9x.

CEO commentary

CEO Clay Gaspar built communications on two pillars: 'execution discipline' and 'accelerating return on capital through optimization'. In his vocabulary, it is significant that he considers "outstanding results" to be not just earnings, but free cash flow and "meaningful cash returns," which is exactly what is most valued in a producer over the long term.

The second part of the announcement is purely strategic: he presents the merger with Coterra as a move to put Devon in a different weighting, creating a platform with higher cash flow, better margins and the ability to return more capital than either company could on its own. Between the lines, it's a clear message that management wants DVN to trade as a "higher quality, more stable and scalable" story, not a run-of-the-mill cyclical producer with no clear plan for cash.

Outlook

In the short term, the outlook is more cautious. Devon expects Q1 2026 to be hit by winter weather: production is expected to be cut by around 1%, or 10k boe/d (roughly half the impact in oil). Adjusting for this "downtime", the company targets an average of 823-843k boe/d. Q1 capex is expected to be around 900mn boe. The company's capex is expected to be USD 900mn, slightly above Q4 levels, suggesting that it does not want to put the brakes on activity just because of a one-off weather event.

Long-term results

Devon is a textbook cyclical story, with two worlds alternating on the financial statements: the "commodity tailwind" and the "commodity headwind". In 2022, revenue jumped to $19.83 billion and operating profit to $8.58 billion, an extremely strong year supported by energy prices. This was matched by net profit of USD 6.02 billion and EPS of 9.15. However, 2023 saw a normalisation, with sales falling to USD 15.14 billion and operating profit to USD 4.79 billion, which translated into a drop in net profit to USD 3.75 billion and EPS to 5.86. In 2024, sales rose slightly to US$15.57bn, but it was a weaker year margin-wise: gross profit and operating profit fell to US$4.27bn and US$3.77bn respectively, while net profit fell to US$2.89bn and EPS to 4.57. In practice, this is confirmation that Devon can manage costs, but the oil and gas price cycle still has a dominant impact on the bottom line.

What is interesting though is the resilience at the operating leverage level. Between 2021 and 2024, operating costs have held relatively steady in absolute terms (in the order of hundreds of millions of USD), while fluctuations have mainly gone through sales and gross profit. This is exactly the type of structure where profitability can accelerate quickly when realized prices and volumes rise, while when prices fall, the company tries to "maintain" cash flow through efficiency. Similarly, EBITDA shows that even after the boom fades, the business remains robust: from $10.38bn in 2022, it has fallen to $7.57bn in 2023 and $7.43bn in 2024, still a high level for a company with a strong return on capital.

An important nuance is working with the share count. The average number of shares has gradually declined between 2021 and 2024 (from 663 million to 623 million), which means that some of the return to shareholders has gone systematically through buybacks, increasing the "EPS per share" effect even in worse commodity years. In the Q4 2025 results, this framework is even more visible: the company bought back 7.1m shares for 250m in the quarter. It has returned $4.4 billion since the program's inception and says it has retired roughly 14% of its shares. This is key to Devon's investment thesis: it's not just about how much it makes in a given year, but how consistently it can convert cyclical gains into more sustainable value per share.

News

The biggest strategic development is the planned merger with Coterra. The transaction is expected to be all-stock, closing in the second quarter of 2026, and the new entity will be named Devon Energy. Upon completion, existing Devon shareholders are expected to own approximately 54% and Coterra shareholders 46% of the combined company. The main investment argument is scale and synergies: the companies are talking about $1 billion of sustainable annual pre-tax synergies by the end of 2027, which is expected to come through optimizing the capital program, improving operating margins and simplifying corporate costs.

The internal optimization program is also worthy of note. Devon reports that it has already achieved 85% of its $1 billion "business optimization" target and is aiming for full achievement by the end of 2026. For an investor, this means that some of the cost improvements should be structural, not just temporary, increasing the chances that even at average commodity prices the company will be able to hold solid free cash flow.

Shareholding structure

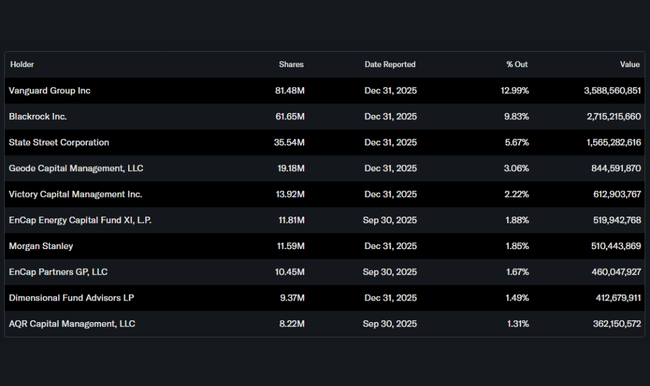

Devon is a typical "institutional" stock. Insiders hold approximately 0.83% of the stock, while institutions control approximately 81.36% of the total shares and 82.05% of the free float. This typically means two things: greater sensitivity to changes in the macro view of energy and oil (as institutional money rotates sectorally), but also a more stable capital base that often supports disciplined capital allocation and cash returns.

Passive managers dominate among the largest holders. Vanguard holds approximately 12.99%, BlackRock 9.83%, State Street 5.67% and Geode 3.06%. In practice, this reinforces the "index" nature of the title and gives management a relatively clear mandate to focus on the metrics that large funds track most: free cash flow, expense structure, balance sheet and return predictability for shareholders.

Analyst expectations

In terms of specific names, it's good to work with the fact that DVN has had mixed but mostly constructive analyst sentiment in recent months. JPMorgan, for example, raised its December 2025 recommendation to Overweight and set a target price of $44, arguing just the optimization plan and valuation relative to intrinsic value. More recent commentary following the announcement of the deal has also seen more cautious voices, with RBC Capital reportedly holding Hold with a target price of USD45.

At the broader market level, the consensus is in a range of roughly USD 34-62 per share, with the average target estimate appearing around USD 46-48. This is matched by the prevailing Buy/Moderate Buy recommendation, but with a visible Hold component, which is common in commodity titles: investors want a clear framework for cash returns while keeping an eye on the oil price cycle