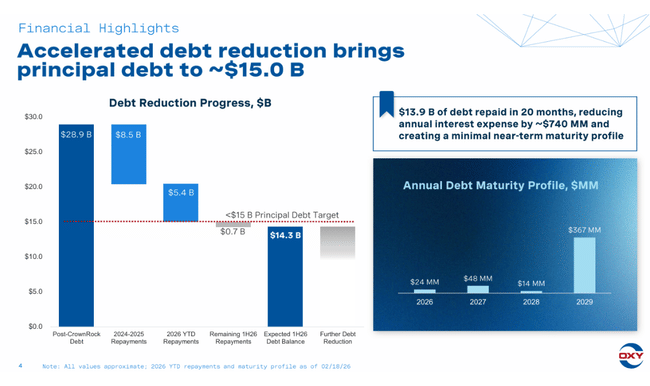

For Occidental, the key shift is not a sudden jump in profitability. The more important change is financial flexibility. The OxyChem sale, completed in early January 2026, created room to move quickly on leverage, and the company says debt is down by $5.8 billion as a result. That matters because it changes the risk profile when commodity prices are not supportive.

Q4 itself shows why that flexibility is valuable. Occidental posted a net loss on an accounting basis, but reported solid adjusted earnings and strong cash performance even though realized prices for oil, NGLs, and gas moved against it. The dividend increase to $0.26 signals management believes free cash flow can be protected through spending discipline and capital flexibility, not through a perfect price environment.

How was the last quarter?

Occidental $OXY reported a net loss attributable to shareholders of -$68 million, or -$0.07 per share, in the fourth quarter of 2025. But on an adjusted basis, the company reported a profit of $315 million, or $0.31 per share. The difference between GAAP and adjusted earnings is substantial and, in this case, also quite "readable": it's mainly the costs and transaction items associated with the sale of OxyChem, which hurt the accounting result in the short term but don't say as much about the operating health of the core business.

The most important numbers this time are in cash flow. Operating cash flow was $2.6 billion and operating cash flow before working capital changes was $2.7 billion. The company invested about $1.8 billion in capital expenditures (including discontinued operations), and even after accounting for minority contributions, generated free cash flow before working capital changes of about $1.0 billion. This is exactly the type of result that matters most to OXY, because in a cyclical sector, the winner is often the one that can maintain cash even at weaker prices while reducing debt or raising return on capital from it.

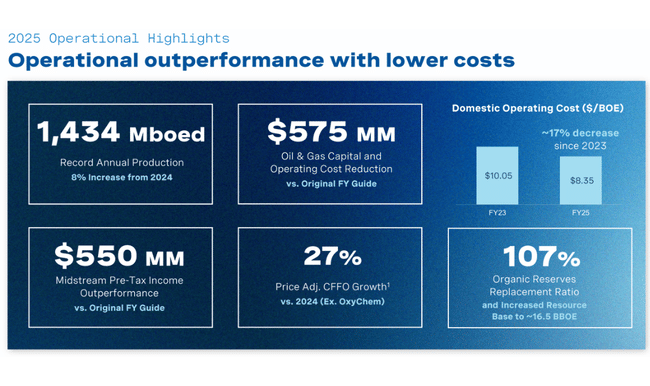

On the operating side, the company beat expectations on volume. Total production came in at 1,481 mboe/d and was above the high end of guidance, driven by Permian and Rockies. At the same time, the midstream and marketing segment also performed well, with pre-tax adjusted earnings ahead of the top end of guidance and the quarter a significant improvement over Q3. This is important for investors as it is the "non-upstream" part that often helps to cushion the impact of commodity fluctuations.

The pressure on the bottom line was primarily price driven. In the upstream, pre-tax profit fell from $1.3 billion in Q3 to $0.7 billion in Q4, and management explicitly says that on a comparability-adjusted basis, the main driver was a decline in realized prices across products. In Q4, WTI averaged around US$59.14/bbl and Brent around US$63.09; the realised price of crude oil fell 9% q-o-q to US$59.22, NGLs fell 15% q-o-q to US$16.68 and domestic gas fell 24% q-o-q to US$1.12/Mcf. This is exactly the part of the story that explains why OXY may be able to "produce" strong cash flow, but accounting profitability is price sensitive in the short term.

The big shift comes on the balance sheet. The completion of the sale of OxyChem on January 2, 2026 has put the company in a different position in terms of debt: Occidental reports that it has reduced debt by $5.8 billion since mid-December 2025, bringing "principal debt" to about $15.0 billion. That's a number that will resonate with investors perhaps more than EPS alone, as OXY's credit profile and pace of de-leveraging is one of the key valuation parameters.

CEO commentary

Vicki Hollub built her commentary around three points: operational excellence, cost efficiency and capital program flexibility. Importantly, management avoids triumphalism over earnings, instead emphasizing "meaningful production and operating expense outperformance" and the ability to beat full-year guidance in both oil and gas and midstream. Between the lines, this implies an effort to shift the perception of OXY from a "high debt commodity bet" to a company that has a significantly stronger balance sheet after the sale of OxyChem and can more consistently generate free cash flow even at worse prices.

Outlook

In the Q4 results material itself, the company's main focus is that both production and midstream result have surpassed the top line, and that it will maintain flexibility in its capital and development programmes following the transaction. However, for the 2026 outlook, it is useful for investors to set this in the earlier corporate outlook: Occidental has communicated in the past that it expects rather stable production and lower capex for 2026, with capex in a range of approximately US$6.3-6.7 billion. In practice, this means setting "cash flow protection": not chasing volumes at all costs, but holding returns and room for debt and dividend.

The interpretation is more conservative to defensive. When a company cuts capex and aims for stable production, it is usually saying that it wants to be prepared for a scenario where commodity prices do not record euphoria. Moreover, following the sale of OxyChem, it is clear that some of the "new" space will go primarily into balance sheet and capital return, not aggressive production growth.

Long-term results

Occidental is a typical example of a company where the long-term picture is made up of two layers: the commodity cycle makes for big swings in revenues and earnings, while cost structure and capital discipline determine how well the company survives the leaner years. In 2022, when the sector benefited from an exceptionally strong pricing environment, OXY posted revenue of $36.25 billion, operating profit of $13.28 billion, and net income of $13.22 billion. EPS shot up to 13.41, showing how brutally fast upstream leverage translates into the stock when price, volume, and margin come together.

Then came normalization. In 2023, sales fell to $28.33 billion and net income to $4.67 billion, and in 2024, sales fell further to $27.10 billion and net income to $3.04 billion. EPS pulled back from 13.41 to 4.22 and then to 2.59 in two years. Importantly, it's not just "less profit" but how quickly the margin cushion shrinks: gross profit fell from $17.05 to $9.65 billion and EBIT from $15.15 to $5.25 billion between 2022 and 2024. This is exactly why investors in OXY are so concerned about the balance sheet and debt - because in a worse cycle, the margin for error shrinks dramatically.

From an operating leverage perspective, EBITDA is interesting to watch because it often better captures "cash earning power" than net income loaded with depreciation and one-time items. EBITDA has fallen from $22.16 billion in 2022 to $14.54 billion in 2023 and $12.72 billion in 2024. It's still a high level, but the trend is clear: the company has moved from an exceptional year to a mode where it must compensate for weaker pricing with disciplined investment, cost optimization and capital structure. In this context, the sale of OxyChem and the rapid debt reduction makes sense as a move to stabilize OXY for just "average" years, not just boom years.

News

The biggest change is the sale of OxyChem, which closed on January 2, 2026. The company is reclassifying OxyChem into discontinued operations because of this, which will change the structure of results and the perception of OXY going forward: the business is becoming more purely "oil & gas + midstream", increasing sensitivity to the commodity cycle, but also freeing up capital and accelerating de-leveraging. The deal immediately became a balance sheet catalyst, as Occidental reports a $5.8bn reduction in debt over a short period and a drop in principal debt to around $15bn.

The second line is the return of capital. Occidental raises its quarterly dividend by more than 8% to $0.26 per share and notes that the dividend per share has doubled in the past four years. This is significant for investors because OXY historically had a reputation as a company where the dividend and balance sheet were "subservient" to growth and acquisitions; today, management is trying to show the opposite story - resilient cash flow and financial flexibility is the priority.

Shareholding structure

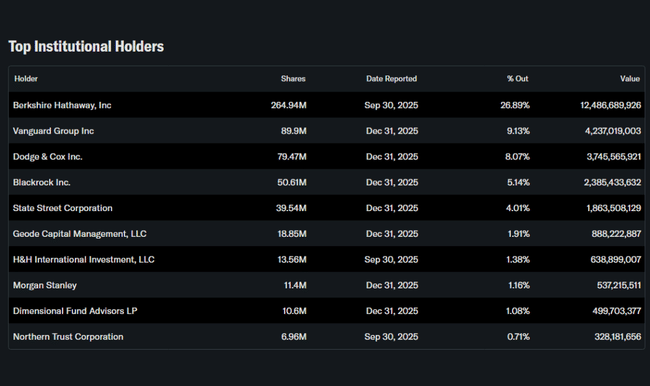

Occidental has an extremely strong "insider" footprint, which in practice is mainly associated with Berkshire Hathaway. The insider share is reported at around 27.18%, while the institution holds around 51.88% of the shares and approximately 71.25% of the free float. In such a structure, the title often responds not only to oil but also to how the market reads the long-term role of the strategic shareholder and its tolerance for debt, buybacks or transactions.

The largest institutional shareholder is Berkshire Hathaway with approximately 26.89% of the shares, followed by Vanguard, Dodge & Cox and BlackRock. For title stability, this has a twofold effect: on the one hand, it can reduce short-term "panic" in a bad cycle, as a large long-term shareholder tends to be less sensitive to quarterly noise; on the other hand, it increases the importance of capital discipline, as large holders typically push the firm to use free cash flow not to fund expansion at any cost, but to improve the balance sheet and shareholder returns.