Broadcom started fiscal 2026 with a clear split: AI-related semiconductors are doing the heavy lifting, while the rest of the business stays steady. The company delivered a strong quarter and kept profitability very high, which matters because it shows the growth is not coming from “low-quality” revenue.

What investors will focus on most is the outlook. Broadcom expects next-quarter revenue around $22 billion, which implies a much faster growth rate than it just printed. Management also expects to hold similar profitability. That combination is what makes the report feel like a trend, not a one-time boost.

How was the last quarter?

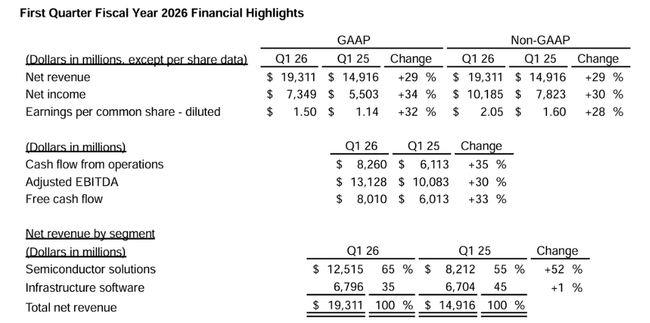

Broadcom built Q1 2026 $AVGO on two pillars: a sharp acceleration in semiconductors and stability in software. Total revenue was $19.311 billion, with the semiconductor division adding 52% to $12.515 billion. Software (infrastructure software) added just 1% to 6.796 billion, but that's what's important to investors: with such strong growth in chips, the software part is not acting as a drag, but rather as a stabilizer.

Profitability is extraordinary by the standards of large technology companies. Adjusted operating profit before depreciation and amortization was $13.128 billion, or 68% of sales. And more importantly, cash: operating cash was $8.260 billion, while investments in assets were only $250 million, leaving free cash at $8.010 billion. This is one of those reports where an investor doesn't have to ask "where's the cash" - there's an extreme amount of it, and it's coming in fast.

From a "what was one-off and what was structural" perspective, the main structural driver is clear: chips and networking for computing centers that build infrastructure for artificial intelligence. The company's self-reported revenue from this area was $8.4 billion and exceeded its own expectations, largely due to demand for custom accelerators and networking components for AI.

Top points of the results

Revenue of $19.3 billion, up +29% year-over-year.

GAAP net income $7.35 billion, $10.19 billion after adjustments.

Earnings per share $1.50, $2.05 after adjustments.

Free cash of $8.01 billion, roughly 41% of sales.

Semiconductor revenue $12.5 billion(+52%), software almost unchanged(+1%).

AI chip revenue $8.4 billion(+106%), outlook for next quarter $10.7 billion.

New $10 billion share repurchase program and $0.65 per share dividend.

CEO commentary

Hock Tan commented on the report very directly: the key is the growth in AI semiconductor revenue, which reached $8.4 billion in Q1 and more than doubled year-on-year. The sentence for investors to take away is the outlook for the next quarter: Broadcom expects AI semiconductors alone to reach $10.7 billion. That's a strong signal that the company is seeing orders and shipments in real time, not just "presentation optimism."

CFO Kirsten Spears complemented this with the "quality" of the results: revenue growth and profitability growth go hand in hand, and the company continues to make aggressive returns on capital. In the quarter, it returned $10.9 billion to shareholders (dividends and buybacks), a strategy that has been consistent at Broadcom for a long time: high cash should turn into a return of capital, not lie idle.

Outlook

The outlook for the second quarter is perhaps the most important part of this report. Broadcom expects revenue of around $22 billion, up 47% year-over-year. The company also expects profitability to remain flat: adjusted operating profit before depreciation and amortization of around 68% of revenue. Translated: Broadcom says it can grow faster without having to discount profitability.

What the outlook implicitly says about the structure is also important: since software is growing minimally, the increase to 22 billion is practically a bet on the semiconductor part to continue to accelerate. This is where the market's confidence will be broken: if expectations of 10.7 billion from AI chips are confirmed, it will be a very strong confirmation of the trend.

Long-term results

The last four years of Broadcom $AVGO have shown that it can grow in very different cycles - and that acquisitions and portfolio changes can stir up the cost base in the short term, but increase the company's potential in the long term. Revenues grow from $33.2 billion (2022) to $35.8 billion (2023), then to $51.6 billion (2024) and $63.9 billion (2025). This shift is not just organic growth, but the effect of expanding the software side after the larger deals in previous years, while gradually realigning the semiconductor mix toward compute centers.

On the profitability front, Broadcom's margins are structurally high, but the "shape" of profits changes depending on how hardware and software are mixed and what the depreciation and accounting items are. It is therefore practical for an investor to stick to two things: the ability to generate cash and the ability to return capital. And it is Q1 2026 that shows once again that the cash machine is running at full speed - free cash of 8.0 billion in a single quarter is itself an argument for why the market ranks Broadcom among the "best quality" titles within semiconductors.

News

Two specific news items from the report carry a lot of investment weight. The first is a new $10 billion share buyback program through the end of 2026, a clear signal that the company expects continued very strong cash flow after the investment. The second is the shift in communication around AI: Broadcom is no longer just talking about "general growth" but giving specific revenue numbers from this segment and a specific target for the next quarter (10.7 billion). This both increases transparency and raises the bar - the market will want to see these numbers repeated.

Shareholder structure

Broadcom is a heavily institutionally owned title: the institution holds roughly 79% of the stock, and the largest holders are Vanguard, BlackRock and State Street. That typically means two things: high liquidity and high sensitivity to how large money managers assess the cycle around computing centers and artificial intelligence.