Alibaba’s latest quarter makes the split inside the group very clear. Overall revenue grew only modestly, but operating profit fell more than 70 percent and non‑GAAP net income dropped by roughly two thirds as the company poured money into instant retail, user experience upgrades and AI and cloud infrastructure. Cloud and AI were the bright spots: Alibaba Cloud revenue rose about 36 percent year on year to more than 43 billion yuan, while AI related product revenue delivered its tenth consecutive quarter of triple digit growth and management highlighted its MaaS platform as a new engine for the business.

For investors, the picture is a classic trade off between near term earnings pressure and long term growth. China e‑commerce is focused on stabilising users and monetisation but is seeing margins squeezed by subsidies and quick commerce competition, while cloud and AI are growing fast and could become a much larger share of group revenue by the end of the decade if current trends hold. The quarter therefore looks weak on short term profit metrics, yet it sketches a framework in which heavy spending on instant commerce and AI could pay off over time, provided the industry avoids another price war and Alibaba can translate its AI and cloud leadership into durable, higher margin cash flows.

How was the last quarter?

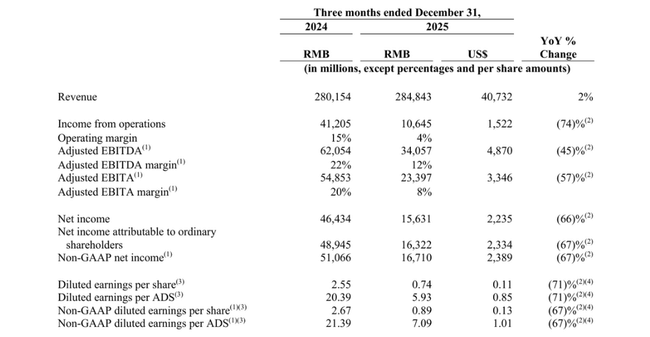

Total revenue for the quarter was CNY284.843 billion (about USD40.7 billion), up roughly two percent year-on-year; excluding the Sun Art and Intime retail businesses, it would have been roughly nine percent growth on a comparable basis. Operating profit, on the other hand, fell to CNY10.645 billion (about USD1.5 billion), down about 74 per cent year-on-year.

Adjusted operating profit (Adjusted EBITA) fell 57 percent to CNY23.397 billion (about USD3.3 billion) as Alibaba significantly increased investment in quick commerce, customer experience and technology, only partially offset by better cloud performance and savings in other parts of the group. Net profit attributable to shareholders was CNY16.322 billion (about USD2.3 billion), while total net profit was CNY15.631 billion (about USD2.2 billion), down by about two-thirds. Adjusted net profit was CNY16.710 billion (about USD2.4 billion), also down 67 percent year-on-year.

Earnings per share fell accordingly: diluted earnings per American Depository Receipt (ADS) were CNY5.93 (about USD0.85) and adjusted earnings per ADS were CNY7.09 (about USD1.01), down about 67-71 percent from a year ago. Operating cash flow dropped to CNY36.032 billion (about USD5.15 billion) from about CNY70.9 billion previously, while free cash flow fell to CNY11.346 billion (about USD1.6 billion) - mainly due to heavy investment in quick commerce. On the other hand, the group remains very liquid, with cash and liquid investments of around CNY560.2 billion (about USD80.1 billion).

Segments and AI + cloud

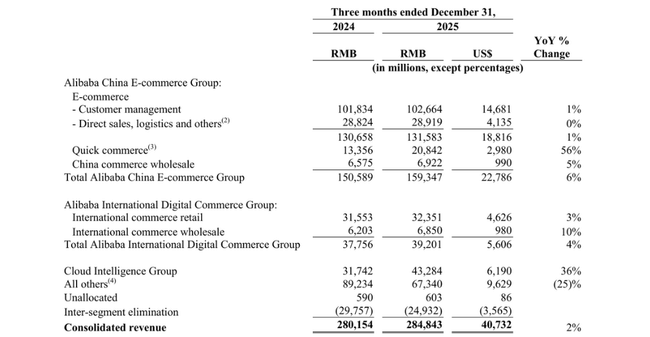

Chinese e-commerce(Alibaba China E-commerce Group) generated sales of about CNY159.347 billion (about USD22.8 billion), up about six percent year-on-year. Of that, customer management (advertising, commissions) brought in CNY102.664 billion (about USD14.7 billion), up just one percent from a year ago, as transaction activity was weaker and the one-time effect of software deployment fees wore off. Quick commerce (mainly renamed Ele.me, now Taobao Instant Commerce), on the other hand, grew rapidly, with sales increasing to roughly CNY20.842 billion (about USD3.0 billion), up about 56 percent year-on-year, while gradually improving unit economics through growth in average order size and more efficient logistics.

Alibaba International Digital Commerce Group (AIDC) had sales of around CNY39.201 billion (about USD5.6 billion), up four percent year-on-year. Retail international e-commerce (AliExpress, Lazada, Trendyol, etc.) grew three percent, wholesale grew ten percent, while AIDC's losses were significantly reduced year-on-year, mainly due to optimized logistics and more efficient use of marketing spend. The AliExpress Choice business improved unit economics and the "Brand+" program accelerated brand recruitment, which boosted sales.

The most important growth driver is the Cloud Intelligence Group. Its sales reached CNY43.284 billion (about USD6.19 billion), up about 36 percent year-on-year. AI product revenue grew at a triple-digit rate for the tenth consecutive quarter, and the Model-as-a-Service (MaaS) platform is becoming the new cloud driver. Alibaba Cloud is also strengthening reputationally: according to Gartner and IDC, it is the leader in databases, generative AI in Asia and financial cloud in China, with a share of around 43 percent in infrastructure for the financial sector.

Management commentary

In the results, CEO Eddie Wu highlighted that Alibaba continues to invest heavily in its two pillars - AI and consumption - and that AI will be one of the main growth drivers. He noted that Cloud Intelligence Group revenue is up 36 percent and that AI products are showing triple-digit growth for the tenth consecutive quarter, with MaaS already acting as a new cloud engine; on the consumer side, he highlighted the integration of user scenes into the Qwen app, which has reached over 300 million monthly active users. The tone is confident on the AI and cloud side, but between the lines he admits that the price for this strategy is significant pressure on current profits.

CFO Toby Xu commented on the rapid growth of the AI+cloud business as a reason why he is not afraid to ramp up investment, while noting that Quick Commerce is scaling while improving unit economics. He emphasized that strong liquidity and resilient cash flow generation give the company room to sustain high strategic investments. The CFO's tone is consistent with a "growth before short-term profit" strategy, emphasizing that the current decline in profitability is a conscious decision, not just the result of weak demand.

Outlook

Alibaba itself did not present a detailed numerical outlook for the quarter ahead in the press release itself, but several important lines can be gleaned from management's words. First, cloud and AI are set to continue to grow faster than the whole - management expects AI products and MaaS to continue to drive double-digit cloud growth and be even more integrated with the e-commerce ecosystem.

Second, quick commerce (Taobao Instant Commerce) will remain a priority - the company expects continued growth in volume and average order value, as well as continued investment, so the group's profitability will remain under pressure in the coming quarters. Thirdly, the Qwen app is becoming a horizontal interface for many services (Taobao, Tmall, Amap, Fliggy, Alipay) and is set to increase user engagement and generate transactions across the platform in the long term - the outlook thus rests on the assumption that AI-assisted shopping will become a common shopping tool.

Long-term results

For the twelve months ending 31 March 2025, Alibaba achieved revenue of CNY996.347 billion (approximately USD139.3 billion, at an exchange rate of around CNY7.15/USD), up nearly six percent year-on-year from CNY941.168 billion (approximately USD131.5 billion) in the previous period. In 2023, sales were about CNY868.687 billion (about USD121.0 billion) and in 2022 about CNY853.062 billion (about USD118.8 billion) - showing that sales growth has been more in the mid-single digits in recent years, although the absolute volume is huge.

Gross profit reached CNY398.062 billion (about USD55.6 billion) in the latest year, a double-digit growth against CNY354.845 billion (about USD49.4 billion) in the previous year. Thus, gross margin is gradually improving as the mix shifts towards higher value-added (cloud, AI, services) while the firm keeps a lid on the growth in cost of goods sold. Operating expenses were CNY257.157 billion (roughly USD35.9 billion), versus CNY241.495 billion (about USD33.6 billion) a year earlier - rising but slower than gross profit, which allowed operating profit to rise to CNY140.905 billion (about USD19.7 billion) from CNY113.350 billion (about USD15.8 billion).

Pre-tax profit jumped to CNY161.421 billion (about USD22.6 billion) from CNY93.861 billion (about USD13.1 billion), mainly due to the improvement in operating profit and other items; after-tax net profit remained CNY130.109 billion (about USD18.1 billion) compared to CNY80.009 billion (about USD11.3 billion). Thus, earnings per share grew faster than revenue in the past year: from roughly CNY31.6 (about USD4.4) to CNY55.1 (about USD7.9), and diluted EPS from CNY31.36 (about USD4.4) to CNY53.6 (about USD7.6). This is helped by a gradual reduction in the number of shares outstanding from roughly 2.69 billion in 2022 to 2.43 billion in 2025.

EBIT increased to CNY147.710 billion (about USD20.6 billion) from CNY119.507 billion (about USD16.7 billion), EBITDA to CNY182.672 billion (about USD25.5 billion) from CNY164.011 billion (about USD22.9 billion). Thus, over the long term, Alibaba is showing solid profitability growth on a full-year basis, but quarterly numbers (including this December one) can fluctuate significantly depending on the investment cycle, restructuring, and how aggressively the company pushes new quick commerce and AI projects.

Shareholder Structure

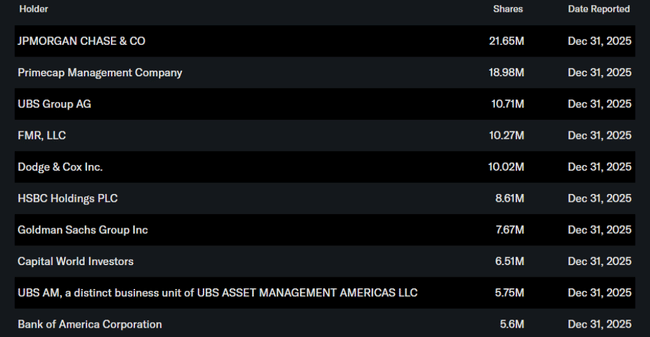

Alibaba has a very low official insider stake, around 0.01 percent of the stock, while the institution holds approximately 11.9 percent of the stock and free float. This is a relatively small institutional stake compared to U.S. technology titles, reflecting both regulatory and political risks and the fact that some shares are held through various structures and depositories.

The largest institutional investors include JPMorgan Chase (holding around 0.9 per cent), Primecap Management (around 0.8 per cent), UBS Group (around 0.45 per cent) and FMR (Fidelity) with a holding of just over 0.4 per cent. Most of the shares are therefore held by a broad base of smaller investors and various structures outside of traditional funds, which means greater sensitivity to market sentiment and news of regulation in China, but also room for potential future increases in institutional holdings if the risk profile improves.

News and strategic shift

Integration of Qwen app into the consumer ecosystem (Taobao, Tmall, Taobao Instant Commerce, Amap, Fliggy, Alipay) - AI chat is becoming a "layer" on top of Alibaba's services that can arrange shopping, transportation and travel in one go; the goal is to make Qwen the main gateway to shopping and services.

Qwen's rapid growth - consumable Qwen has surpassed 300 million monthly active users, the campaign around Chinese New Year has brought tens to hundreds of millions of first-time AI shoppers; AI is thus becoming not only a marketing tool but also a driver of real orders.

Developing its own AI infrastructure - T-Head' s chip division has mass-produced its own GPUs for training and deploying models, compatible with major AI frameworks; combined with Qwen and the cloud, Alibaba has more control over computing capacity and costs, which is key in the era of expensive GPUs.

Strengthening global cloud footprint - Alibaba Cloud operates 92 availability zones in 29 regions and holds a leading position in China in financial and hybrid cloud, according to IDC and Gartner; while expanding outside China to offer AI and database services to international clients.

Growth of quick commerce and rebranding of Ele.me - the service has been renamed Taobao Instant Commerce and more closely integrated with both Taobao and the Qwen app; quick delivery of food and goods is set to become an important growth pillar, even at the cost of weaker margins in the short term.

Expanding international partnerships - as part of the AIDC, Alibaba is expanding its collaboration with Shinsegae in South Korea and bringing more brands to AliExpress and other platforms through the "Brand+" program; the goal is to make international business build on stronger brands, not just anonymous cheap goods.