Johnson & Johnson entered 2026 exactly how we want to see it from a defensive healthcare giant - double-digit revenue growth, slightly declining but still strong adjusted earnings, and higher full-year guidance. The company confirmed that after the separation of Kenvue's consumer business, the new "clean" JNJ stands on two solid pillars - innovative therapies and medical technology - and that both areas are pulling upward.

At first glance, it may strike you that net accounting profit and GAAP EPS are down more than fifty percent year-over-year. But these are mainly last year's one-time effects (such as the impact of the transactions around Kenvue), so management and the market are looking primarily at the adjusted numbers: adjusted earnings per share of $2.70 are only slightly below last year and above analyst estimates.

How did Q1 2026 turn out?

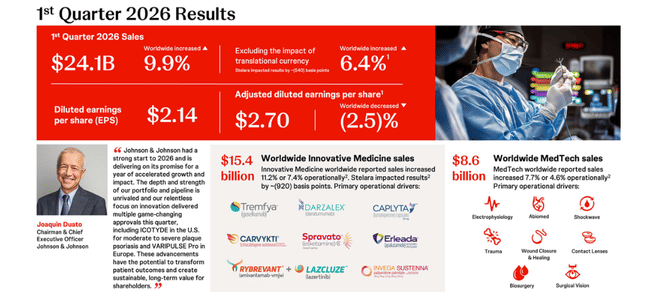

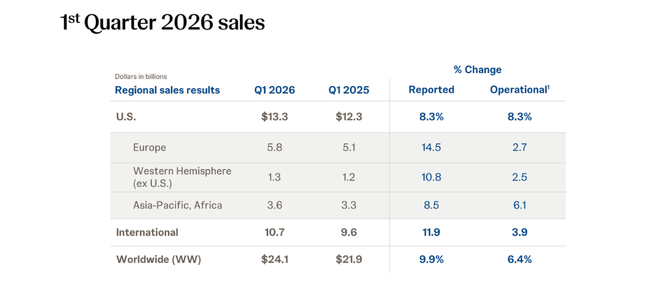

First-quarter revenues $JNJ rose to roughly $24.1 billion, up nearly 10 percent from roughly $21.9 billion in the same period last year. Adjusted for currency effects, revenue grew around six percent, with an adjusted operating view of just over five percent - solid organic growth for a company of this size. Most of the growth was driven by the pharmaceuticals (innovative medicine) division: this added sales to around $15.4 billion, compared to around $13.9 billion last year. The rest came from the medtech segment, which benefited from higher demand for orthopedics, cardiology and eye products.

At the profit level, the picture is two-layered. GAAP net accounting profit fell to about $5.2 billion from about $11.0 billion last year, and GAAP EPS fell from about $4.54 to $2.14 - more than half. This is primarily due to the fact that the comparative base was heavily impacted by one-time items (asset sales, tax effects, etc.), while this year's number is "cleaner" operationally in terms of structure.

However, if we move to adjusted earnings (excluding these one-off effects), the picture is more stable. Adjusted net income was down only about one to two percent at around $6.6 billion, and adjusted earnings per share were $2.70, versus $2.77-$2.77 last year. Importantly, the $2.70 is above the average analyst estimate, which was expecting something around $2.66-$2.68. In other words, margins are under modest pressure, but operating performance is within or slightly above expectations.

Free cash flow was weaker this quarter - estimates are talking about $1.5 billion, compared to about $3.4 billion last year. This is mainly related to the timing of investments, working capital and some payments; more important to JNJ is its full-year ability to generate stable cash, which has been very strong over the long term. The balance sheet remains robust, with low debt and plenty of room for dividends and acquisitions.

As commented by management

In the press release and presentation , CEO J. Duato talks about the "strong start to 2026" and that the company is "delivering the year of accelerated growth" that it promised. He singles out in particular:

Nearly 10 percent revenue growth

strong momentum in innovative medicine

Confirmed and newly approved products to support growth through the end of the decade

and, finally, the lifting of the full-year outlook

J&J now expects 2026 revenues of roughly between $100.3 billion and $101.3 billion, with the midpoint of the $100.8 billion range slightly above market consensus. Adjusted earnings per share should be between $11.45 and $11.65 - the midpoint of $11.55 corresponds to about seven percent growth versus 2025 and roughly in line with what the market was expecting. Overall, then, management is sending the signal, "we're growing faster than before, we're raising guidance, and the plan to achieve double-digit growth by the end of the decade is on track."

The stock reacted with a slight upward move after the results. There are two reasons for this:

A good outlook for the rest of the year

Expectations of success for a number of products

JNJ's long-term results

The annual numbers for the past four years confirm that J&J is a typically stable company - sales and profits have been growing over the long term, although acquisitions, divestitures and one-off items occasionally speak between years.

Revenues have moved from roughly $80 billion in 2022 to just over $94 billion in 2025 in four years, growing about six and a half percent to $85 billion in 2023, a little over four percent to $88.8 billion in 2024, and more than six percent to $94.2 billion in 2025. That's a very solid pace for a healthcare giant, especially when you consider the spin-off of the consumer business.

Gross profit grew at an even faster rate - roughly 55.4 billion in 2022, 58.6 billion in 2023, 61.4 billion in 2024 and 68.6 billion in 2025. This suggests that the product mix is improving (more high-margin drugs and better medtech portfolios) and that the company is able to keep the cost of goods sold under control.

Operating expenses (research, sales, administration) grew a bit faster - from about 34.4 billion in 2022 through 35.2 billion in 2023 to 39.2 billion in 2024 and 43.0 billion in 2025. Operating profit still grew - around 21.0 billion in 2022, about 23.4 billion in 2023, dropping slightly to 22.1 billion in 2024 (due to one-time factors) but jumping to $25.6 billion in 2025.

Net income is heavily influenced by one-time items - jumping to over $35 billion in 2023 (double that of 2022), falling to about $14.1 billion in 2024, and rising to $26.8 billion in 2025. Importantly, adjusted (normalized) earnings are growing more steadily, so it makes more sense for an investor to track the trend in adjusted EPS and cash flow. For example, the supplemental materials show that normalized adjusted EPS grew from roughly $10.8 in 2025 toward an estimated $11.5 in 2026.

Share count has been declining slightly in recent years due to share repurchases (from about 2.66 billion shares in 2022 to about 2.43 billion in 2025), so some of the EPS growth is attributable to financial policy, but the main driver is business and margin growth. EBITDA is on an upward trend over that period, with a significant jump in 2025 when EBITDA approaches $32.6 billion.

Shareholders

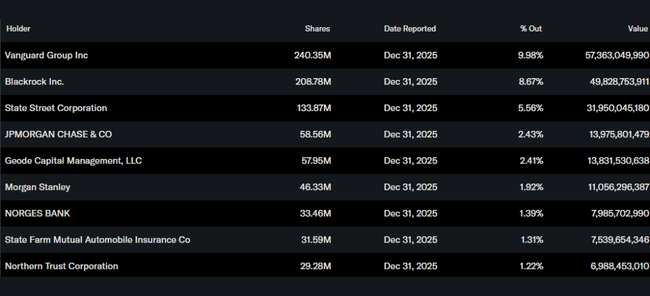

Insider holdings (management, board) account for only about 0.06% of shares - a negligible amount. Institutional investors hold roughly 75-76% of the stock and free float. The rest is held by a broad base of retail investors and smaller institutions.

The largest shareholders are large fund groups:

Vanguard holds around 240 million shares (roughly 10%)

BlackRock about 209 million (about 8.7%)

State Street about 134 million (about 5.6%)

JPMorgan and Geode Capital each hold about 2.4% of the shares.

That said, the price performance depends heavily on how the large index and actively managed funds view J&J. If they believe that J&J has a quality drug pipeline, a stable medtech business, and the ability to grow the dividend and earnings over the long term, they are willing to hold the stock despite temporary swings in GAAP numbers. Should sentiment toward healthcare or valuations in general deteriorate, pressure could come despite the fact that the results themselves look good.

News and strategic moves

New approved drugs and indications - J&J has strengthened its portfolio in areas such as dermatology and oncology. It mentions the approval of ICOTYDE as the first targeted oral peptide for psoriasis, the expansion of indications for the TECVAYLI + DARZALEX FASPRO combination in multiple myeloma, and other moves to ensure that the failure of older blockbusters (e.g., Stelara) won't be fatal for the company.

Medtech innovations - in medical technology, the company is launching products such as VARIPULSE Pro for faster ablations in cardiology and the TECNIS PureSee intraocular lens for cataract patients in the US. These products expand the addressable market and help lift margins in the medtech segment.

Increased full-year outlook - J&J raised its full-year revenue and earnings estimates during Q1. It now expects sales of about $100.8 billion and adjusted EPS of about $11.55, which is slightly above the previous forecast and in line or slightly above consensus. This confirms the company has "visibility" for the rest of the year.

Strategic focus post-Kenvue - after spinning off the consumer business, J&J is purely "healthcare" - innovative pharmaceuticals and medtech. Management reiterates that the goal is to achieve double-digit annual growth by the end of the decade, and Q1 2026 is presented as confirmation that they are on that trajectory.

Planned Enterprise Business Review - the company has announced a plan for December 2026 to show investors in more detail its medium-term strategy, capital allocation and innovation pipeline. This is a signal that it is preparing for the next "chapter" after Kenvue with an emphasis on transparency to the market.