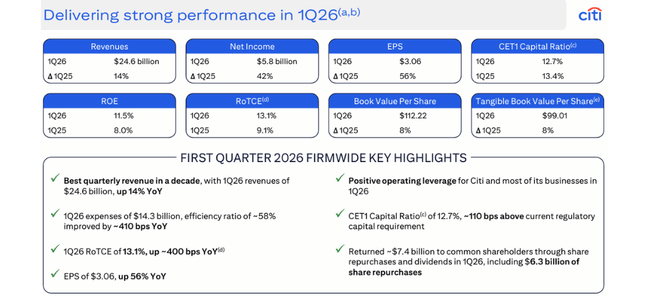

Citigroup’s Q1 2026 looks like the kind of result shareholders have been waiting years for. Revenue jumped 14% to 24.6 billion dollars, net income surged 42% to 5.8 billion and diluted EPS climbed from 1.96 to 3.06 dollars, pushing return on common equity to 11.5% and return on tangible common equity to 13.1% as all five core businesses plus the legacy portfolio contributed. Cost discipline is finally visible in the numbers, with the efficiency ratio improving to 58.1%, credit losses edging down and management signalling that 90% of its large “Transformation” programmes are now at or near their target state after years of restructuring.

What makes the quarter stand out even more is how generous Citi was with its success. The bank returned about 7.4 billion dollars via dividends and buybacks in the period – a payout ratio of 134% of earnings – funded from a still‑comfortable CET1 capital ratio of 12.7% and a tangible book value just over 99 dollars per share. For investors, that combination of double‑digit profit growth, a long‑awaited move of ROE into the low‑teens and capital returns that temporarily exceed what the bank earns is a powerful narrative, but it also underlines that Q1 sits closer to “harvesting the benefits of a clean‑up” than to a sustainable new baseline Citi can repeat quarter after quarter.

How Q1 2026 turned out

For the first quarter, Citi $C made $24.6 billion, versus $21.6 billion in the same period in 2025. That's 14% growth, and it's built on a broad base - all five core businesses and the remaining "legacy" franchises are growing. It's not that the bank has made one big one-off number somewhere in trading, but the opposite: the model is starting to behave as CEO Jane Fraser has been promising for several years, as an interconnected whole.

Net profit climbed to $5.8 billion from $4.1 billion last year. This is a roughly 42% year-over-year increase, driven mainly by three factors: higher sales, a lower effective tax rate (around 21%, down from 25% last year), and the bank having fewer shares due to buybacks. As a result, earnings per share moved from $1.96 to $3.06, with about a third of the improvement coming from lower taxes and fewer shares, and the rest coming from actual improved operating performance.

Costs rose to $14.3 billion, up seven percent from a year ago. They're being pulled up by higher wages, including severance, the impact of foreign exchange rates, as well as higher cost-related expenses (such as commissions, fees and other items tied to revenue growth). On the other hand, we are already seeing savings - productivity, lower legal costs, the gradual unwinding of "stranded" costs following the sale of foreign franchises, and lower transformation expenses at headquarters.

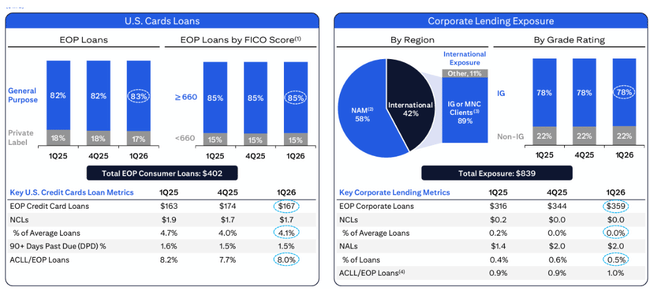

The cost of risk was $2.8 billion. Of this, 2.2 billion is net charge-offs, about the same as last year, and about 0.6 billion is net reserve additions. So the bank is still pricing in a not risk-free environment - factoring in worse macro scenarios and a change in portfolio mix - but at the same time it no longer needs to increase reserves as aggressively as in past years. Net charge-offs are even down 10 percent year-over-year, mainly due to better U.S. credit and markets.

The balance sheet continues to firm up. Loans were around $762 billion at the end of the quarter, averaging $755 billion - up about nine percent from a year ago. Deposits grew to about $1.4 trillion, up about ten to eleven percent year-over-year, primarily due to growth in the corporate and institutional services segment.

For shareholders, this quarter was exceptional. Citi returned approximately $7.4 billion in dividends and share repurchases - roughly $1.1 billion in dividends and $6.3 billion through buybacks. That translates to a payout ratio of 134%, more than the bank earned in the period. It's a clear signal that management is confident in the capital position and wants to lift returns to shareholders quickly, but also something that can't be taken as a new long-term standard.

What Jane Fraser says and how to think about the results

Citi boss Jane Fraser described the results as "an exceptionally strong start to the year". There are three key messages from her comments.

The first - growth is across the board. Fraser teases out that revenue is up fourteen percent and net profit up 42%, with all major divisions growing: services (Services) +17%, markets (Markets) over seven billion in revenue, banking (Banking) with fee growth of 12% and a record first quarter in M&A, wealth management with eleven percent revenue growth, and US credit cards with four percent growth and returns of around 20%. This is not the Citi of the post-crisis era, which was riding on one strong leg, but a fairly well-balanced model.

Two - the transformation is in its final stages. According to Fraser, Citi is in the "final stages" of divesting foreign retail franchises and 90% of its transformation programmes are said to be "at or close to target". That said, the weight of transformation costs should gradually ease over the next few years and the bank should be more defined by standard operating results. Translated: it should no longer be a perpetually rebuilding bank, but a normally operating profit machine.

Third - capital and returns. Fraser stresses that the target for this year is a return on tangible common equity (RoTCE) in the 10-11% range. In the first quarter, Citi achieved a 13.1% RoTCE and is therefore beating the 2026 target rather than just catching up. This is a marked difference from previous years, when the bank often missed the target. It also implicitly says: the Q1 result is above "normal", other quarters may be weaker, but 2026 should still look better than previous years.

At Investor Day in May, Citi wants to better show investors in detail what this new phase will look like - what exactly they should expect from each business, what the capital policy will look like, and what returns the bank can deliver over the long term. This will be even more important for valuation than the Q1 number itself.

Long-term results

The annual results over the last few years show that Citi is gradually picking itself up from the deep downturn, but still stands somewhere between "done" and "more to do".

Revenues were around $100 billion in 2022, $155 billion a year later, and have already hit $170.7 billion in 2024. 2025 then brought a slight drop to 169.2 billion - a roughly one percent respite after very strong growth in the previous two years. It can be seen that part of the story was driven by the normalisation of rates and interest income after a period of zero rates, and part of it is attributable to the trading and fee business.

Operating profit (EBIT) was around $18.8 billion in 2022, dropping to around $12.9 billion in 2023, rising to $17.0 billion in 2024 and moving to $20.2 billion in 2025. It's a typical "turnaround" picture where costs, restructuring and depreciation come first, then savings and a new business mix take effect.

This makes net income look similarly zigzag. Citi earned roughly $14.8 billion in 2022, dropped to $9.2 billion in 2023, jumped to $12.7 billion in 2024, and moved to roughly $14.1 billion in 2025. Earnings per share (diluted) were about $7 in 2022, then fell to about $4.0 in 2023, rose to $5.95 in 2024 and $6.99 in 2025.

Yet two trends are clear:

Net income and EPS rise steadily after the 2023 decline.

at the same time, the number of shares is shrinking due to share buybacks - from around 1.96 billion shares in 2022 to around 1.87 billion in 2025

This means that some of the EPS growth is "financial engineering" via buybacks, but a substantial portion is going after actual profitability growth. Q1 2026 fits into that picture - 42% earnings growth and $3.06 EPS in one quarter give Citi a chance to move up another "step" this year unless the environment deteriorates dramatically.

Shareholders

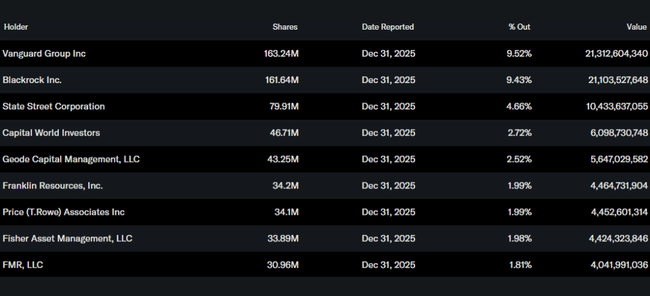

Citigroup is a pure institutional title. The insider stake (management and board) is roughly a quarter of a percent of the stock, virtually negligible. Over 82% of the shares are held by institutions - large funds, pension and insurance companies.

The largest shareholders are Vanguard and BlackRock, each with a stake of about 9.5 percent, followed by State Street with nearly five percent and Capital World Investors with less than three percent. In other words - Citi's course is in the hands of the big fund houses. As soon as their collective view of Citi shifts, whether through better results or a change in strategy, the stock reacts quickly.

This is important in the context of the current payout ratio of 134%. If the big players believe that Citi can sustain such a generous capital policy for at least a few years with a stable ROE of around 11-12%, they will be willing to rewrite valuations to the upside. If, on the other hand, they see this as a one-time "reward" in a good year, they will remain more cautious and want to see more quarters of similar numbers.

News and strategic moves

The first quarter of 2026 is not just about the numbers, but also about where Citi is moving strategically.

The bank is in the final stages of divesting foreign retail franchises, including Russia, and is moving toward a model that rests on five interconnected pillars - Services, Markets, Banking, Wealth Management and the U.S. consumer. The goal is to have a business that is less complex, more manageable and more capital efficient than the old Citi, spread across 20 retail banking markets.

The transformation costs and risks associated with "legacy" portfolios should gradually decline, leaving room for business as usual - growing loans, fees and services to large corporations and institutions. At the same time, Citi is dramatically paying down capital so that shareholders will finally see the benefit of sitting in a bank that now carries significantly more capital than the regulatory minimum.

From an investor's perspective, the Q1 2026 results look like really good news - Citi is no longer just a "perpetual turnaround" but a bank that, for all the noise around transformation, can deliver double-digit revenue growth, more than 40 percent earnings growth, and a return on capital above its own target. The question for the next few quarters is whether this quarter will become the new normal or just a happy combination of a favorable environment and a restructuring still in progress.