Amazon is off to a very strong start in 2026, confirming that the restructuring of the last two years (cost cutting, streamlined logistics, discipline in investments) has translated into significantly higher profitability across all segments. Revenues are growing at double-digit rates in all major regions, AWS is accelerating growth and still holding very high margins, while the North American and international e-commerce business is already firmly established in profit. At the same time, however, free cash flow has fallen sharply in the trailing twelve months, reflecting a spike in infrastructure and data centre investment - a cycle of "invest first, harvest later" rather than a structural problem.

Management's presentation and commentary highlighted in particular the continued acceleration of AWS, growth in AI workloads and strong momentum in the advertising business, but also continued cost optimization in logistics and retail. The overall picture is this: Amazon is banking on a combination of robust revenue growth (c. mid-teens), rising operating margins, and a clear thesis that heavy investments in AI and cloud today are set to deliver significant cash flow in the years ahead.

Q1 2026 results: revenues in the high-teens, operating profit growing even faster

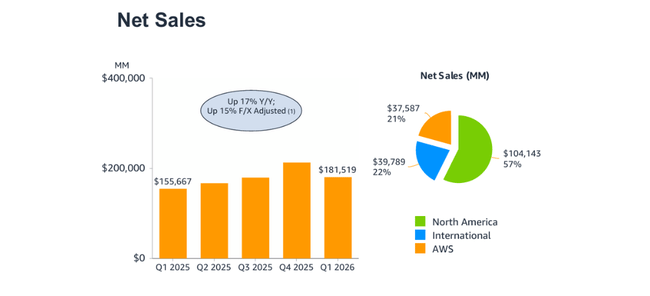

Amazon's net sales in Q1 2026 were $181.5 billion, up roughly 17-18% from the same period last year (c. $155.7 billion). Adjusted for currency effects, sales grew 15% - a solid "high-teens" pace even without currency effects. In terms of structure, the North America segment accounts for the largest portion, followed by International and AWS.

At the trailing twelve-month level, revenue was $742.8 billion, up 14% from $650.3 billion a year earlier (13% after adjusting for FX). This shows that the acceleration from recent quarters is not a one-off, but is dragging full-year metrics as well.

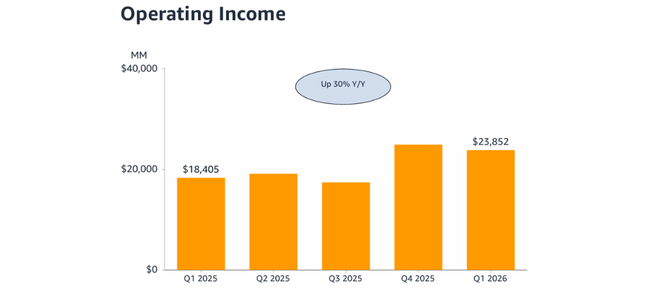

Operating profit in Q1 2026 was $23.85 billion compared to $18.41 billion a year earlier, an increase of roughly 30%. That said, not only is revenue growing, but profit is growing faster than revenue - margins continue to improve, thanks in large part to the higher profitability of AWS and profitable e-commerce. At trailing twelve months, operating profit came in at $85.4 billion, up 19% from $71.7 billion.

Four-quarter net income rose to $90.8 billion from $65.9 billion, up 38% y/y, but the quarterly net income is impacted by a one-time factor - a $16.8 billion gain from the revaluation of the Anthropic investment, which is recorded in non-operating income. That inflates the headline net income number, but it is the growth in operating profit and segment margins that is more important from a core business perspective.

North America, International and AWS segments.

North America

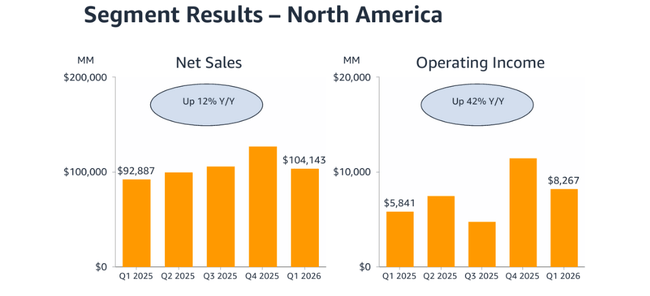

The North America segment generated $104.1 billion in revenue in Q1 2026, up 12% year-over-year to $92.9 billion. Segment operating profit grew from $5.84 billion to $8.27 billion, up 42% y/y, indicating a significant improvement in margins. This is due to a combination of scaling logistics, a better product mix (more custom advertising and higher margin services) and a focus on efficiency. At trailing twelve months, North America generates $437.6 billion in revenue (+12% y/y) and $32.0 billion in operating profit (+42% y/y).

International

The International segment reported sales of $39.8 billion in Q1 2026, up 19% from $33.5 billion a year ago, or 11% after adjusting for currency. Operating profit increased from $1.02 billion to $1.42 billion (+40% y/y), while trailing twelve months International generated $168.2 billion in revenue (+40% y/y) and $5.2 billion in operating profit (+significant growth, over 6% y/y after FX adjustments). Thus, the International business is no longer a "perpetual loss-making expansion" but a steadily profitable pillar.

AWS

The AWS cloud segment had a very strong quarter. Revenue in Q1 2026 was $37.6 billion, up 28% from $29.3 billion a year ago (26% after adjusting for FX). AWS operating profit grew from $11.55 billion to $14.16 billion, up 23% y/y, confirming that AWS can grow while maintaining high margins even as capital requirements rise in the AI era.

At trailing twelve months, AWS generates $137.0 billion in revenue and $48.2 billion in operating profit. That means AWS carries roughly a third of Amazon's total operating profit, although it makes up a smaller share of revenue than retail. From an investment perspective, AWS is still a key valuation driver - growth of around 25-30% and high margins are exactly what the market wants to see from the "AI cloud" leader.

Free cash flow, investments and shares

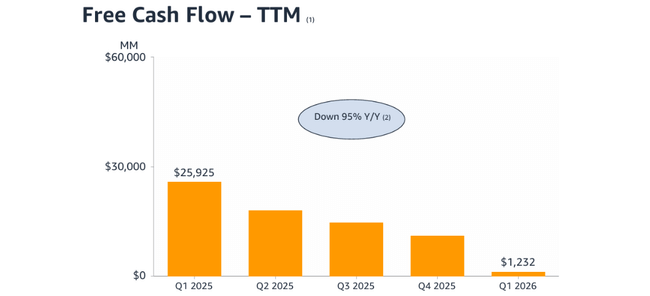

Trailing twelve-month free cash flow (operating cash flow minus capex) fell from $25.9 billion in Q1 2025 to $1.23 billion in Q1 2026, down 95% y/y. The reason is not a collapse of the business, but a combination:

Operating cash flow admittedly rose from $113.9 to $148.5 billion (+30% y/y),

but investment in assets (primarily data centres, logistics and infrastructure) increased even faster - from $88.0bn to $147.3bn.

So Amazon $AMZN is investing massively in the short term, especially in its AI and cloud infrastructure base, squeezing free cash flow. Management has long declared that the goal is to optimize free cash flow, not maximize it in one year - deliberately investing in capabilities that should bear returns in future years.

The number of common shares outstanding, including converted stock-based awards, is around 10.9 billion, and the presentation shows a desire to manage dilution - stock-based awards are relatively stable, not an uncontrolled dilution scenario.

Management commentary and key news

Several key highlights emerge from the presentation and management communication(CEO Andy Jassy):

AWS and AI - Management emphasizes that AWS growth is driven primarily by AI workloads and classic cloud business, with customers accelerating migration while adding new types of workloads. Amazon is building AI not only as a service (models, inferencing services) but also as something that improves its own internal efficiency (logistics, recommender systems, advertising).

Retail and logistics - management talks about the continued improvement of the delivery network (regional fulfillment, warehouse automation) and the growth of margins in retail, which is particularly visible in the North America segment.

Advertising and other services - comments suggest that advertising is one of the main drivers of retail profitability as it carries high margins and is linked to growing traffic and engagement.

Infrastructure investment - the sharp increase in capex is presented by management as a conscious bet on long-term growth in AWS and AI, not a cost issue.

The overall tone of management is confident - Amazon is presented as a company that has moved from the "defense and optimization" phase (2023-2024) to the "invested growth" phase - stable margins, double-digit revenue growth, and targeted investments in AI/chips/datacenter and logistics.

Why the share price is rising by around 3% after the results

Amazon stock is up about 3% post-earnings because the market is seeing a combination of what it wanted: double-digit revenue growth above 15%, accelerating AWS with very strong margins, management's clear focus on AI as an engine for future growth, and continued improvement in retail profitability in North America and internationally. Although free cash flow on a TTM basis is temporarily falling due to aggressive infrastructure investments, investors are reading this as a pro-growth move rather than a problem - operating cash flow is growing and the company has great freedom to allocate capital. Moreover, results are in line or slightly above expectations and the outlook contains no negative surprises, so the market is "rewarding" confirmation of the story, not challenging it, after previous growth.

In its outlook for Q2 2026, Amazon expects net sales to reach $194-199 billion, which corresponds to a 16-19% year-over-year growth from Q2 2025. The company also expects operating profit in the $20-24 billion range, while it achieved an operating profit of $19.2 billion in Q2 2025, so it is projecting a year-over-year improvement on profitability as well. This outlook already incorporates the assumption that Prime Day will fall just into the second quarter this year, and assumes a slightly negative currency effect (about 10 basis points on revenue growth).