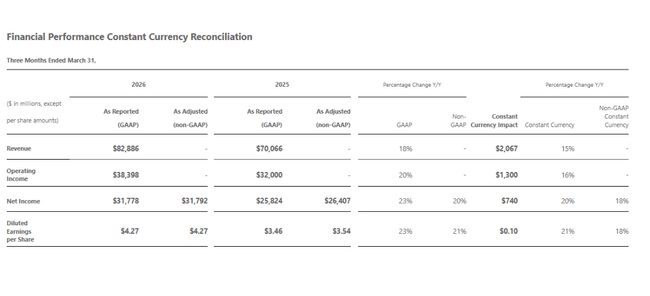

Microsoft delivered another very strong set of numbers for the third fiscal quarter of 2026, confirming that cloud and AI are the main drivers of growth. Revenues grew 18% to $82.9 billion (15% at constant currency), operating profit 20% to $38.4 billion and net income 23% to $31.8 billion, with earnings per share up to $4.27 (+23% y/y).

The AI business as a standalone area has already reached an annual revenue run rate of $37 billion, up 123% Y/Y, according to Satya Nadella, clearly showing that generative AI and agent-based solutions are not just a "promise of the future" but a real source of revenue.

Q3 FY 2026 results: revenue, profit and margin growth

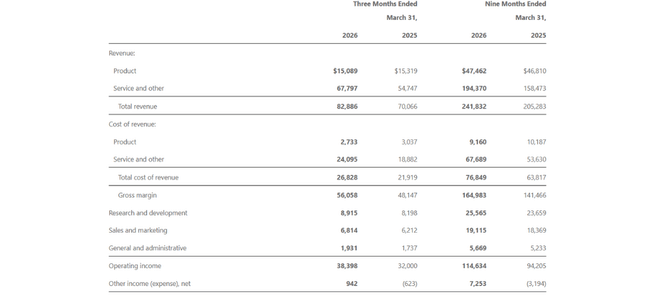

Microsoft's $MSFT revenue in the quarter ended March 31, 2026 was $82.9 billion, up 18% from $70.1 billion in the same period last year, or 15% when adjusted for currency effects. Gross margin increased from $48.1 billion to $56.1 billion, primarily reflecting strong growth in services and cloud, which carry higher margins than the pure product business.

Operating profit increased from $32.0 to $38.4 billion (+20% y/y, +16% at constant currency), so profit is growing faster than revenue and operating leverage is working. R&D expenses grew 9% (from 8.2 to 8.9 billion), sales and marketing expenses 10% and general and administrative expenses 11%, all at a lower rate than sales, so margins are improving slightly despite continued investment in AI.

GAAP net income rose to $31.8 billion from $25.8 billion, up 23%, and diluted EPS increased to $4.27 from $3.46 (+23%). On a non-GAAP basis (which strips out the impact of the OpenAI investment), net income grew 20% and EPS grew 21% (+18% in constant currency), so the difference between GAAP and non-GAAP is minimal this time - the impact of the OpenAI investment is only -$14 million on net income in the quarter.

Productivity, Intelligent Cloud and More Personal Computing segments.

Productivity and Business Processes

The Productivity and Business Processes segment (Office, Microsoft 365, LinkedIn, Dynamics) earned $35.0 billion, +17% y/y (13% at constant currency).

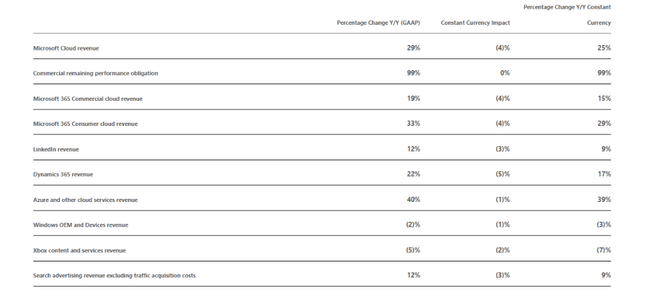

Microsoft 365 Commercial cloud revenue grew 19% (15% at constant currency).

Microsoft 365 Consumer cloud revenue grew 33% (29% at constant currency), reflecting strong demand for Office subscriptions and additional services in the home.

LinkedIn grew 12% (9% at constant currency).

Dynamics 365 sales grew 22% (17% at constant currency), an above-average pace for enterprise applications.

Intelligent Cloud

Intelligent Cloud is a key growth driver. Revenue was $34.7 billion, +30% y/y (28% at constant currency).

Azure and other cloud services grew 40% y/y, or 39% at constant currency, an acceleration from some previous periods of slower growth.

In addition to Azure, the server business and enterprise services are also contributing, but it is clear that the key driver is the adoption of generative AI, agent solutions and cloud services for businesses of all sizes. While segment margins are not explicitly stated in the text, given the company-wide operating profit growth and the high capitalization of Azure/AI, it is safe to say that cloud continues to lift overall profitability.

More Personal Computing

The More Personal Computing segment (Windows, Devices, Xbox, search advertising) earned $13.2 billion, a slight decline of 1% y/y (-3% at constant currency).

Windows OEMs and Devices: revenues declined 2% (-3% at constant currency).

Xbox content and services: sales down 5% (-7% at constant currency).

Search advertising excluding TACs (traffic acquisition costs): sales up 12% (9% at constant currency).

This is a segment where traditional business (Windows, Xbox) is stagnating or slightly declining, but search advertising and services are partially offsetting this decline. In terms of Microsoft as a whole, this segment is already smaller and less growing than cloud and productivity.

Management commentary and AI news

Satya Nadella puts the entire quarter in the context of "agent computing" - an era where AI agents will actively perform tasks and optimize outcomes for customers. He highlights that the AI business (across products) achieved an annual revenue run rate of $37 billion, up +123% y/y. This means that AI is no longer a marginal add-on, but a significant part of the overall cloud.

Amy Hood points out that the results beat expectations on revenue, operating profit and EPS, thanks to strong demand for Microsoft Cloud. Management also notes that cloud growth is being driven not only by AI, but also by the continued migration of traditional IT workloads to Azure, the expansion of Copilot in Microsoft 365, and the adoption of AI services in Dynamics and other enterprise products.

In terms of strategic news, the quarter includes hundreds of product enhancements, but it's essentially about deepening AI integration across platforms - from Azure (models, infrastructure, security) to Microsoft 365 Copilot to developer tools. At the same time, the company's balance sheet shows sharp growth in invested capital in property & equipment ($283.2 billion vs. $205.0 billion nine months ago), reflecting heavy investment in datacenter and AI hardware.

The outlook and why the stock's reaction is lukewarm

Microsoft doesn't provide a specific outlook in the press release itself - it says it will provide forward-looking guidance on the conference call. But according to subsequent comments from Cal (summarized in analyst articles), management is counting on continued solid growth in Microsoft Cloud, continued strong Azure momentum (though the pace may normalize gradually), and continued high investment in AI infrastructure.

The stock reacts only moderately positively after the results, with virtually no significant movement since:

the numbers are very good, but broadly in line with what the market was expecting - no surprisingly higher growth rates or dramatically better margins

AI and cloud metrics are strong (Azure +40%, AI run rate 37 billion), but the market had already largely factored in these numbers after previous quarters and Microsoft's valuation is aligned with that

the outlook, as investors read it from the call, contains neither a major positive "upgrade" nor a negative surprise - rather, it confirms the current growth trajectory, so there is no significant change in expectations

In other words, Microsoft delivered what it was supposed to: strong revenue and profit growth, accelerating Azure, robust AI numbers, and stable margins. The market is rewarding this with a slight plus, but without much euphoria because it's more about confirming the story than taking it to the next level.

Key numbers

Revenue: $82.9bn, +18% y/y; +15% at constant currency.

Operating profit: USD 38.4bn, +20% y/y; +16% at constant currency.

Net profit: USD 31.8 billion, +23% y/y (GAAP); non-GAAP +20% y/y.

EPS (diluted): $4.27, +23% y/y (GAAP); non-GAAP +21% y/y.

Microsoft Cloud revenue: $54.5 billion, +29% y/y; +25% at constant currency.

Azure and other cloud services: +40% y/y; +39% at constant currency.

Productivity and Business Processes revenue: $35.0 billion, +17% y/y; +13% in constant currency.

Intelligent Cloud sales: USD 34.7 billion, +30% y/y; +28% in constant currency.

More Personal Computing sales: USD 13.2 billion, -1% y/y; -3% in constant currency.

Return of capital to shareholders: USD 10.2bn in dividends and buybacks in Q3 FY26.