Alphabet entered 2026 in style - revenue shot up by more than a fifth, earnings per share more than doubled thanks to a combination of strong operating performance and investment gains, and Google Cloud experienced a sharp acceleration. Growth is not driven by one segment: high double-digit growth in Search, YouTube and subscriptions, and the cloud is showing for the first time how strong demand for AI solutions and infrastructure can be.

Sundar Pichai talks about a "terrific start" and points out that AI investments and a fully integrated "full stack" approach (models, infra, products) now permeate the entire business - from Search to Gemini for consumers and businesses to cloud AI services. But at the same time, the results are not just about the AI story: Alphabet delivered its 11th consecutive quarter of double-digit revenue growth and improved operating margin, signaling to the market that it can grow profitably, even though the investment in AI infrastructure is enormous.

Q1 2026 results: strong revenue, margin and profit growth

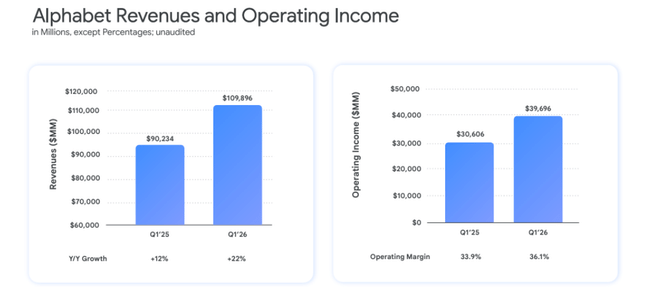

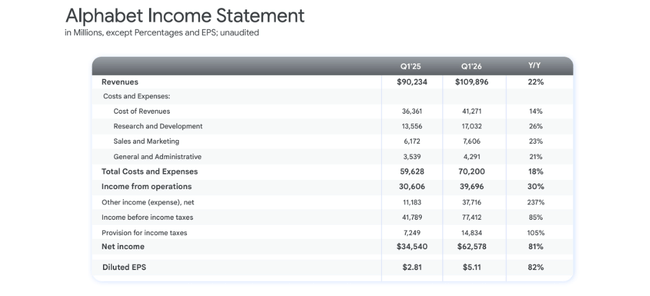

Alphabet's consolidated $GOOG revenue reached $109.9 billion in Q1 2026, up 22% year-on-year (19% at constant currency) from $90.2 billion in the same quarter of 2025. This is the fastest growth rate since 2022 and the 11th consecutive quarter of double-digit growth.

Operating profit rose from $30.6 billion to $39.7 billion, up 30%, and operating margin improved from 34% to 36.1%, showing strong operating leverage - costs are growing slower than revenue. R&D, sales and marketing, and administrative expenses are growing, but at a lower rate than revenue, and a portion of shared AI costs are charged to "Alphabet-level activities" outside of pure segment results.

Net income jumped from $34.5 billion to $62.6 billion (+81% y/y) and diluted EPS jumped from $2.81 to $5.11 (+82% y/y). The important factor is the "Other income" line, which includes a net gain of $37.7 billion, mostly from unrealized remeasurements of non-traded equity holdings - mainly in AI and tech startups. These gains do not provide the same quality as operating cash flow, but they boosted capital and EPS in the quarter.

Google Services and Google Cloud segments.

Google Services

The advertising and consumer business (Google Services) earned $89.6 billion, up +16% y/y. Inside this segment:

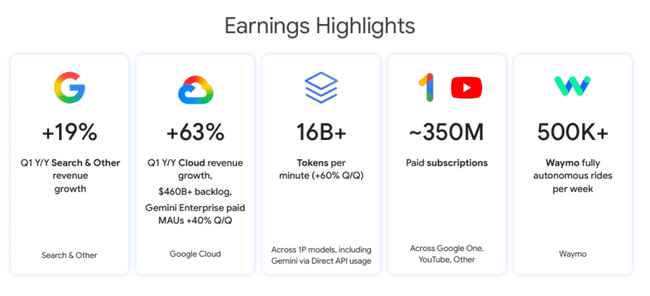

Google Search & other: $60.4 billion (+19% y/y) - Search had a very strong quarter, with management explicitly saying that AI experiences (AI Overviews, Gemini in Search) are increasing queries and engagement, rather than cannibalizing traditional clicks.

YouTube ads: $9.9 billion (+11% y/y), driven by higher ad demand and growth in premium subscriptions within the YouTube ecosystem.

Google Network: $7.0bn (down slightly from $7.26bn), reflecting structural pressure on network partners and a shift of advertising budget directly to Google's own platforms.

Google subscriptions, platforms and devices: $12.4bn (+19% y/y) - this mainly includes paid subscriptions such as YouTube Premium, YouTube Music, Google One and some devices.

Overall, Alphabet reports that the number of paid subscriptions (across YouTube, Google One and other services) reached 350 million, further evidence that it is building more stable recurring revenue beyond pure advertising.

Google Cloud

Google Cloud is the main growth star. Revenue grew to $20.0 billion, up +63% year-over-year (from $12.3 billion), with growth driven primarily by Google Cloud Platform (GCP) - enterprise AI Solutions, enterprise AI Infrastructure and core GCP services. Demand for AI infrastructure and models (Gemini, Vertex AI, other services) has led to backlog (remaining performance obligation) nearly doubling quarter-over-quarter to over $460 billion.

Google Cloud's operating profit grew from $2.18 billion to $6.60 billion, so not only revenue but profit tripled. This suggests that the cloud business is starting to benefit from scale - fixed costs for datacenters and infrastructure are dissolving into higher volumes, even as Alphabet simultaneously invests aggressively in additional capacity.

Other Bets and Alphabet-level activities

Other Bets took in $411 million (vs. $450 million last year) and generated an operating loss of $2.10 billion (-1.23 billion last year). Sundar Pichai highlighted Waymo, which surpassed 500,000 fully autonomous rides per week, a signal that this "moonshot" is approaching a more commercial phase.

"Alphabet-level activities" posted an operating loss of $5.39 billion (vs. -3.03 billion last year), reflecting more extensive shared AI research and infrastructure costs not allocated to specific segments.

Cash flow, balance sheet and capital allocation

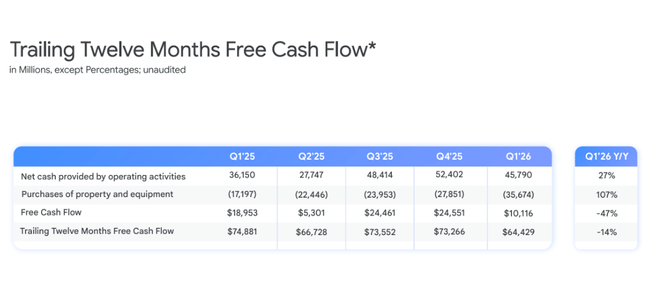

Operating cash flow in the quarter was $45.8 billion, up from $36.2 billion in Q1 2025. Free cash flow (after investments) is not directly reported in the release, but the cash flow statement shows that Alphabet is investing massively - asset purchases (property & equipment) reached $35.7 billion, roughly double the $17.2 billion last year.

On the balance sheet, we see:

$126.8 billion in cash and marketable securities

Non-marketable securities (investments in private companies, often AI and tech) $106.9 billion, up from $68.7 billion at the end of 2025 - an increase partly due to revaluation, partly due to new investments

Tangible assets (property & equipment) rose to $281.0 billion from $246.6 billion in just three months

Alphabet issued $31.1 billion of new unsecured net revenue bonds in the quarter for general corporate purposes - de facto financing a portion of capital expenditures or general capital structure. Long-term debt rose from $46.5 billion to $77.5 billion.

The dividend was raised by 5% to $0.22 per share for the quarter, a rather symbolic but psychologically positive move for some investors given the size of cash and cash flow.

Management Commentary and AI News

In his commentary, Sundar Pichai repeatedly highlights AI as a key driver of growth:

AI in Search: new AI experiences (AI Overviews, AI Mode) led to an increase in queries and user engagement, which is behind the 19% revenue growth in Search & other.

Gemini and consumer AI: Q1 was the strongest quarter ever for "consumer AI plans", driven by Gemini; the number of paid subscriptions (YouTube, Google One, others) reached 350 million.

Gemini Enterprise: has very strong momentum with 40% quarter-on-quarter growth in paid monthly active users in the enterprise segment.

Infrastructure and models: first party AI models (Gemini) are processing more than 16 billion tokens per minute via APIs, up 60% from last quarter - this shows the giant scale of AI usage in real-world applications.

Waymo: surpassing 500,000 fully autonomous rides per week underscores that Alphabet has "physical AI" (autonomy) in advanced stages alongside digital AI.

Management also suggests that capex on AI and cloud will be high in the years ahead, with the CFO commenting that capex is expected to increase "significantly" in 2027 versus 2026 as the company prepares for even greater demand for AI workloads in the cloud. This wraps up a similar story to what we're seeing at Meta - massive investment today to monetize tomorrow.

Why the stock is up 7% after earnings

Revenue growth of 22% to $109.9 billion significantly beat consensus, which was around $106.9 billion - a beat of about $3 billion.

EPS of $5.11 vs. consensus of about $2.63-$2.68 is a huge beat, although a large part of that is a gain from investment revaluation.

Google Cloud, with 63% growth and almost double backlog, beat market expectations of about 40-45% growth - AI demand is clearly stronger than expected.

Operating margin rose from 34% to 36%, which the market has not taken for granted in an environment of massive AI investment - showing that Alphabet is managing to balance growth and profitability for now.

The dividend increase (albeit small) and the relatively conservative use of newly issued debt is being read by the market as a signal of management's confidence in long-term cash flow.

The stock is up roughly 7% post-earnings because the quarter delivers a triple signal:

a significant beat on revenue and EPS vs. consensus

clear evidence that AI is helping the growth of Search, YouTube and the cloud, rather than cannibalizing them

better-than-expected margins despite a significant increase in AI investment

The market is essentially reassessing two fears with this: that AI will destroy the advertising business in Search (so far, it's helping the opposite) and that cloud/AI investments won't translate into growth - Q1 2026 shows that demand for AI cloud and Gemini is very strong in real terms.

Key numbers

Revenue: $109.9bn (+22% y/y; +19% at constant currency).

Operating profit: USD 39.7bn (+30% y/y); margin 36.1% (+2 p.p.).

Net profit: USD 62.6bn (+81% y/y); EPS USD 5.11 (+82% y/y), including USD 37.7bn gain on revaluation of non-tradable securities.

Google Services revenue: USD 89.6bn (+16% y/y); Search & other USD 60.4bn (+19%), YouTube ads USD 9.9bn (+11%), subscriptions/platforms/devices USD 12.4bn (+19%).

Google Cloud revenue: $20.0bn (+63% y/y), operating profit $6.60bn (vs. $2.18bn last year); backlog >$460bn, nearly double q/q.

Capex: USD 35.7bn in Q1; management expects another significant increase in 2027 vs. 2026.

Cash + securities: $126.8bn; long-term debt $77.5bn; non-traded investments $106.9bn.

Dividend: up 5% to $0.22 per share per quarter.