PayPal beat market expectations on both revenue and earnings per share in Q1 2026, TPV grew at a double-digit pace and the company continues to generate billions of dollars in free cash flow. Still, the numbers show that growth is more moderate than dynamic, and operating margins continue to retreat - non-GAAP margins have fallen below nineteen percent, while transaction profit is growing significantly slower than payment volume.

Into this comes new CEO Enrique Lores, who is kicking off a "new era of PayPal" by cutting costs, reorganising into three clearer business pillars and a focus on AI and modernising key services like Venmo. In the short term, the company's story thus revolves less around rapid growth and more around whether Lores can make the platform an attractive growth business again, not just a solid cash-cow under pressure from competitors like Apple Pay and other checkout alternatives.

Q1 2026 results: modest growth at the top, margin pressure at the bottom

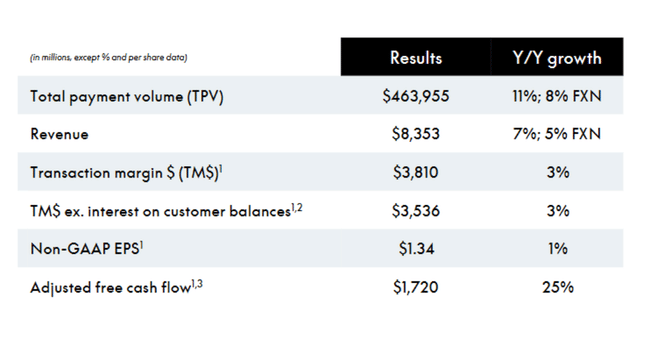

PayPal's $PYPL revenue reached $8.35 billion in Q1 2026, up 7% year-over-year and roughly 5% at constant currency. Meanwhile, consensus was expecting revenues of around 8.05-8.12 billion, so it's a clear beat. Total TPV (Total Payment Volume) rose 11% to $464 billion, or 8% in constant currency, and the number of payment transactions added 7% to 6.5 billion.

At the profitability level, however, the picture is more mixed. GAAP operating income fell 3% to $1.49 billion and non-GAAP operating income fell 5% to $1.54 billion. GAAP operating margin narrowed from 19.6% to 17.8% (down 182 bps), non-GAAP margin fell from 20.7% to 18.4% (-229 bps). GAAP net income fell 14% to $1.11 billion, GAAP EPS fell 6% to $1.21, due to, among other things, negative revaluation of the investment portfolio and cryptocurrencies (-0.08 dollars per share versus +0.03 last year).

On a non-GAAP basis, EPS rose slightly from $1.33 to $1.34 (+1%), beating consensus of around $1.27, but earnings per share growth is clearly much slower than TPV growth. Transaction margin dollars (TM$) rose 3% to $3.81 billion, TM$ excluding interest on client balances also rose 3% to $3.54 billion, clearly below the 11% growth rate in TPV - so monetization of transactions is growing slower than volume.

Operational metrics: volume OK, account activity weaker

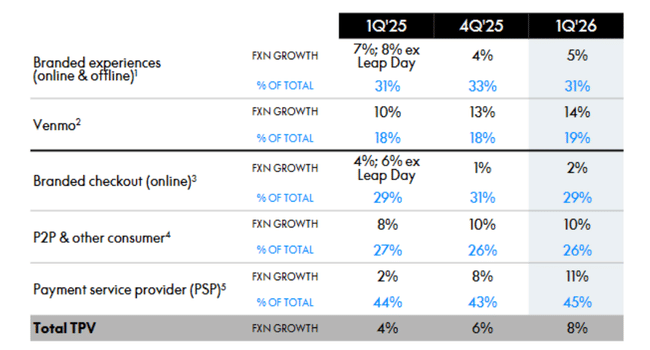

Total TPV grows 11% y/y, a decent number in an environment of increased competition and weaker e-commerce, but TPA (transactions per active account) remains a weakness: on a 12-month basis, it falls 1% to 58.7, while ex-PSP TPA (excluding PSP and unbranded card processes) grows 6%. This shows that where PayPal has its brand and a direct relationship with the customer, it has been able to increase activity, while the pressure is greater in unbranded processing.

The number of active accounts grew just 1% year-on-year to 439 million, and even declined slightly sequentially by 0.2 million accounts. Management has been saying for some time that it is switching from playing the "net number of accounts" game to "quality and engagement," but from a market perspective, this means PayPal can't tell the classic story of rapid user base growth.

Cash flow, balance sheet and capital allocation

Operating cash flow in Q1 2026 was $1.13 billion, slightly below last year's $1.16 billion (-2%). Free cash flow fell from $964 million to $903 million (-6%), while adjusted free cash flow (adjusted for BNPL portfolio timing) jumped 25% to $1.72 billion. This is an important signal to investors - cash generation is still strong, even if headline FCF suffers from the structure of BNPL and other products.

On the balance sheet, PayPal has $13.5 billion in cash, equivalents and investments (short-term and long-term) and total debt of $11.6 billion. Thus, the company remains in a net cash position, albeit less significant than in the past.

PayPal is sparing no capital allocation: in Q1 2026 it spent $1.5 billion on buybacks (34 million shares) and repurchased $6 billion of stock (100 million shares) on a 12-month basis. The board also pays dividends ($0.14 per share per quarter) - a relatively low dividend yield, but a signal that PayPal sees itself in part as a cash-generator.

What the new CEO says and strategic news

Enrique Lores, who joined from HP and has been in the CEO role since March 2026, makes it clear in his comments that the main task is to "improve execution, accelerate growth and simplify the organization." He talks about three main lines:

Improve strategy

simplify the structure of the company

and improve growth and cost base by investing only where it has the greatest impact

One concrete step is the newly announced strategic reorganisation, which divides the firm into three clearly defined pillars:

Checkout Solutions & PayPal

Consumer Financial Services & Venmo

Payment Services & Crypto

The goal is to accelerate decision-making, bring product teams closer to business outcomes and eliminate overlap in today's complex structure. Lores also outlines the next steps in cost optimization - PayPal has historically had robust SG&A and technology spend where it sees room for savings.

Outlook 2026: no acceleration, more stabilization

PayPal's 2026outlook just confirms it is not lifting it despite a beat in Q1.

For Q2 2026, management expects a mid-single digit year-over-year decline in GAAP EPS, and a roughly high-single digit decline in non-GAAP EPS (around -9%) compared to $1.40 in Q2 2025.

For the full year 2026, management expects GAAP EPS with a mid-single digit decline (versus $5.41 in 2025) and non-GAAP EPS in a range of moderate decline to moderate growth versus last year's $5.31.

That said, while Q1 beat expectations, PayPal isn't officially saying "the year will be better than we thought" but rather "we're on track so far, the environment is difficult." Combined with margin contraction, this tells investors that 2026 will be a transition year - a time for restructuring and rebuilding, not accelerated growth.

Why the stock is more likely to lose after the results (despite the beat)

Reasons:

Margins are deteriorating, even on an adjusted basis

active accounts are stagnating/slightly declining

Outlook does not suggest a visible acceleration in 2026

market hoping for a more aggressive reset of expectations or a clearer growth story after CEO replacement

So the results are not bad - on the contrary, the numbers are better than estimates, but they are not leading investors to rewrite their medium-term outlook upwards. PayPal remains a company that generates a lot of cash, but it hasn't yet shown that it can return growth and margins to where they were in a fiercely competitive environment (Apple Pay, checkout competition, local payment methods).

Key numbers

Q1 2026 revenue: $8.35B, +7% y/y, ~5% FX-neutral, beat vs ~$8.05-8.12B expectations.

TPV: USD 464bn, +11% y/y (8% FX-neutral).

GAAP operating margin: 17.8% (vs. 19.6% last year), non-GAAP 18.4% (vs. 20.7%).

GAAP EPS: $1.21 (-6% y/y), non-GAAP EPS: $1.34 (+1% y/y), beat vs. consensus of $1.27.

Transaction margin dollars: +3% y/y, TM$ ex-interest: +3% y/y (below TPV growth).

Active accounts: 439 mln, +1% y/y, sequential -0.2 mln; TPA -1% (TPA ex-PSP +6%).

FCF: $0.9bn (-6% y/y), adjusted FCF $1.72bn (+25% y/y).

Buybacks Q1 2026: USD 1.5bn (34m shares), USD 6.0bn (100m shares) over the past 12 months.