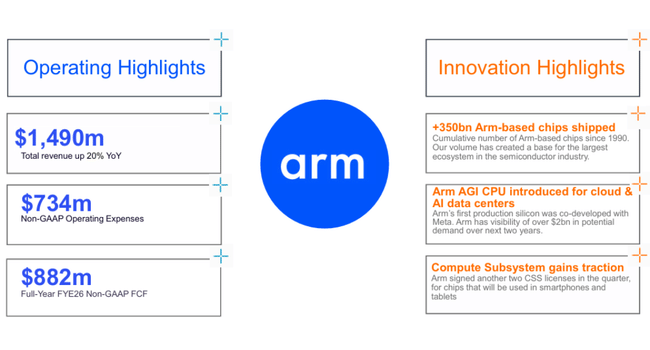

Arm ended the fiscal year with a quarter that would look almost textbook on paper: fourth-quarter revenue grew roughly 20% to $1.49 billion, double-digit growth in both licenses and royalties, and adjusted earnings per share beat the midpoint of the corporate range and market estimates. For the full year 2026, revenue grew 23% to $4.92 billion, non-GAAP EPS increased to $1.77, and the company had its third straight year of double-digit growth combined with strong margins.

Yet the stock is down about 6% after the results. Valuations have long reflected a "pure AI story" and the market is extremely sensitive to any hint of a stall. The commentary warns that the smartphone market remains weak, while also showing how rapidly R&D costs are rising - Arm is buying future AI growth at the cost of short-term pressure on profitability. All of this combined means that even a very good set of numbers is no longer enough to fuel further euphoria.

Q4 and full year results: strong growth, higher costs

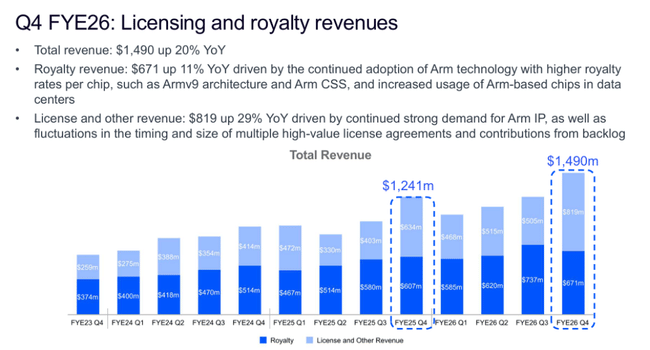

In the fiscal fourth quarter, Arm earned $1.49 billion, up about a fifth from a year ago and slightly above the midpoint of the previously communicated range of around $1.47 billion. Licensing revenue grew 29% to $819 million - the company benefited from new data center designs, with high-performance client chips and edge AI also gaining strength. Royalty revenue grew 11% to $671 million, reflecting strong deployment of designs in endpoint devices across cloud, edge and embedded worlds.

For the full fiscal year 2026, Arm revenue reached $4.92 billion, of which $2.61 billion is royalty and $2.31 billion is licensing and other revenue. In absolute terms, profits are up, but margins are under pressure: non-GAAP operating margin has fallen to around 43% as operating costs, mainly R&D, have risen by more than 30%. Management frames this as a deliberate "upfront" investment in AI generation architectures - it takes a few percentage points off margins in the short term, but it should strengthen Arm's position in the next phase of the AI cycle.

Where growth is coming from: AI data centers, edge and phones

The structure of growth is key to this story. On the licensing side, two areas are mainly behind the numbers: data centers and next-generation client/edge chips. In datacenters, Arm has become the de facto standard for many server CPUs and specialized accelerators - from the big cloud players' own designs to traditional manufacturers' chips. Licenses here tend to translate into future royalties with a lag, so today's licensing numbers are also a signal of the future royalty base.

The royalty part is already starting to reflect this dynamic: management reports double-digit growth in so-called Edge AI, physical AI (embedded) and cloud AI, and talks of more than doubling year-on-year for datacenter royalties. Put simply - AI servers, edge devices and other smart electronics with Arm cores are selling in real terms and generating share for the company from every unit.

But on the other hand, Arm openly says the smartphone market is subdued and remains a short-term drag. Without the AI contribution, overall growth would have been much weaker, illustrating how much the center of gravity of the story has shifted: from the world of "Arm = mobiles" to the world of "Arm = AI infrastructure + edge", with mobiles now being one piece, rather than the whole picture.

Management comment: 'We are at the core of AI infrastructure'

Management reiterates in the shareholder letter and on the call that Arm is "at the core of AI infrastructure" today - whether it's cloud servers, edge devices or dedicated accelerators, Arm's architecture is present in virtually every major AI stack. This position is a major argument for the explosive growth in R&D spending. The company is accelerating the development of new generations of CPU cores, system platforms and collaborations with large customers on custom solutions to increase the value of licenses and royalties going forward.

At the same time, management is presenting long-term scenarios to the investment community - for example, the possibility that an ecosystem of chips built on Arm could generate roughly $15 billion in annual revenue for partners around 2031, and that Arm itself could eventually grow to more than $9 earnings per share. But he's quite frank in saying that these are model projections with a number of assumptions: the rate of AI adoption, the evolution of the mobile market, competitive pressures, and the bargaining power of large customers.

Why the stock is down 6% after earnings

The market reaction looks paradoxical at first glance - strong revenue growth, a beat on earnings, the AI story in full force - and yet the stock loses after the results. But it makes sense in the context of where Arm started from. After the previous rally, the company was one of the most expensive "AI names" in the market, trading on multiples that implicitly factored in long-term double-digit to higher double-digit growth with no visible stumbles.

In such a setup, "just" a very good quarter is no longer enough. Investors are rigorously watching for any sign of weakness, and here are a few: a weak mobile market, fast-growing R&D, slightly declining operating margins, and the fact that the outlook for the next few quarters, while holding a 20 percent pace as a baseline, does not promise significant acceleration. Therefore, the results are more conducive to earnings realization and reevaluation expectations than to further vertical rate growth. Fundamentals are not breaking, but the scope for disappointment appears very small at such a valuation.

Risks and scenarios

What may push the story down: prolonged phone stagnation, potential slowdown in AI investment after the current wave, pressure from large customers on licensing/royalty pricing, and strengthening of alternative architectures. In such a scenario, growth may return to low double or single digits, while high R&D costs would keep margins lower than the market expects.

What strengthens the story, on the other hand, is: additional years of revenue growth of at least 20%, continued strengthening of datacenter royalty, the ability to increase average license value with AI customers, and the return of solid growth in client segments due to AI capabilities in PC and mobile. In such an environment, current development investments would begin to return and today's valuations would look less exorbitant.