NVIDIA entered the new fiscal year as the sovereign leader of the entire AI infrastructure, and Q1 2027 only underscored that status. The company is capitalizing on an unprecedented wave of investment in "AI factories" - giant data centers built specifically for AI computing - and is gradually pivoting from a chip maker to a complete platform for compute, networking, software, and the AI ecosystem.

At the same time, the company has rolled out one of the most aggressive capital return programs in the market. In Q1, it returned approximately $20 billion to shareholders in the form of buybacks and dividends, raised the quarterly dividend from $0.01 to $0.25 per share, and added a new authorized buyback framework of $80 billion (on top of the $38.5 billion already remaining). Cumulatively, it has authorized buybacks of over $118 billion with no time limit. In the context of FCF of USD 48.6bn in one quarter and a verbal commitment to return ~50% of FCF to shareholders, this is a very strong signal that management believes in the sustainability of cash generation.

Key numbers and performance dynamics

P&L: growth from another planet

For Q1 FY27 NVIDIA reports (GAAP):

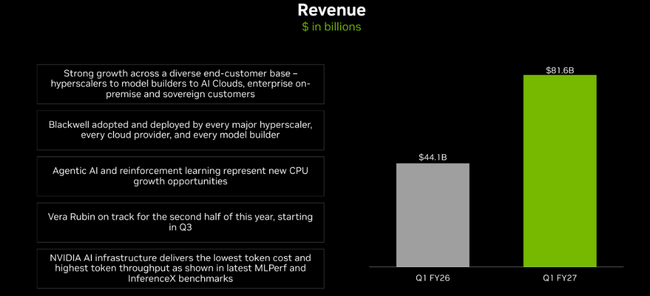

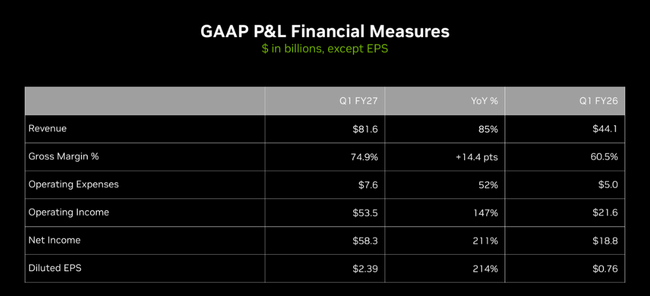

Revenue: $81.6 billion (Q/Q +20%, Y/Y +85%)

Gross Margin: 74.9% (Y/Y 60.5%)

Operating expenses: USD 7.6 billion (+52% Y/Y, but well below revenue growth)

Operating profit: USD 53.5 billion (Q/Q +21%, Y/Y +147%)

Net profit: USD 58.3 billion (Q/Q +36%, Y/Y +211%)

Earnings per share (diluted): USD 2.39 (Q/Q +36%, Y/Y +214%)

On a non-GAAP basis (already including stock compensation, the latter is now excluded):

Gross margin: 75.0%

Operating profit: USD 53.8 billion

Net profit: USD 45.5 billion (Y/Y +139%)

Non-GAAP EPS: $1.87 (Q/Q +18%, Y/Y +140%)

The difference between GAAP and non-GAAP this time around is mostly about the revaluation of the securities portfolio - roughly $15.9 billion of unrealized gains on equities are "extra" in GAAP, but excluded in non-GAAP. But even after this clean-up, earnings and margin growth remains extremely strong.

Segments: datacenters dominate, Edge "just" grows nicely

At the same time, NVIDIA is transitioning to new reporting by two major platforms - Data Center and Edge Computing.

Datacenters

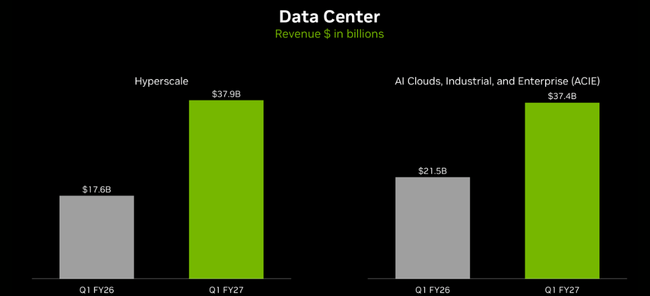

Revenue: $75.2 billion, Q/Q +21%, Y/Y +92%.

Under the old breakdown:

Compute: $60.4 billion (+77% Y/Y, +18% Q/Q)

networking: USD 14.8bn (+199% Y/Y, +35% Q/Q).

Driven by hyperscale cloud providers (AWS, Azure, Google Cloud, etc.) and large internet platforms building "AI factories". In addition, NVIDIA is launching a new sub-segment of ACIE (AI Clouds, Industrial & Enterprise) to capture the growth of dedicated AI datacenters across industries and countries.

Edge Computing

Revenue: $6.4 billion, Q/Q +10%, Y/Y +29%. This includes everything "at the edge": RTX PCs, consoles, workstations, automotive, robotics, AI-RAN, etc. Growth is significantly lower than datacenters, but still above average compared to the rest of the market.

Management commentary: 'AI factories' as the new infrastructure of the world

Jensen Huang frames the quarter with a very aggressive narrative: "The construction of AI factories - the largest infrastructure expansion in human history - is accelerating at an extraordinary pace." He highlights the shift from merely generative AI to so-called "agent AI" - autonomous agents that do real work, generate value, and scale rapidly across companies and industries.

Key message:

NVIDIA is "the only platform" that runs in all clouds, supports all key frontier and open-source models, and scales from hyperscale datacenters to the edge, according to the company.

The company no longer sees itself as just a GPU maker, but as a complete "AI infrastructure": chips (Blackwell, Vera CPU, BlueField-4 STX), network (NVLink, networking), software (CUDA, cuDNN, Nemo, Dynamo, Nemotron, BioNeMo, Ising models), agent tools (NeMoClaw, OpenShell, Agent Toolkit), and an extensive partner ecosystem (Google Cloud, Marvell, Corning, Lumentum, Coherent, etc.).

CFO Colette Kress confirms in an investor commentary that growth is still primarily driven by hyperscale customers, but ACIE (enterprise and industrial AI) is growing rapidly from a smaller base and is set to be another long-term pillar. Importantly, NVIDIA is also not counting any Data Center compute revenue in China in the Q2 outlook - so any future business in China would be "extra" relative to now.

Product and ecosystem news: consolidating the "moat"

Datacenters and AI platform

In the quarter, NVIDIA announced and advanced a number of key building blocks:

Vera Rubin platform - including the Vera CPU, the first ever CPU designed specifically for agent AI, and BlueField-4 STX for accelerated storage infrastructure for AI factories.

Dynamo 1.0 - open-source software that boosts generative and agent inference performance on Blackwell GPUs by up to 7X, already with broad adoption by global players.

NeMoClaw, OpenShell, Agent Toolkit - a suite of tools and open-source platforms for building enterprise AI agents with an emphasis on security and privacy.

Extensions to the Nemotron, BioNeMo and Ising family of models - including the "Nemotron Coalition", an alliance of global AI labs focused on open frontier models and accelerating the development of quantum computers.

Expanding collaboration with Google Cloud - new A5X instances with Vera platform, deploying Gemini models on Google Distributed Cloud running on Blackwell and Blackwell Ultra GPUs.

Strategic partnerships with Marvell, Coherent, Corning and Lumentum in optics, NVLink Fusion and silicon photonics - aiming to take AI datacenter scaling to the next level.

Edge Computing, Gaming, Automotive and Physical AI

On the NVIDIA "edge" front:

Launched DLSS 4.5 and showed DLSS 5, a new AI-driven rendering model that is set to be the biggest graphics breakthrough since ray tracing in 2018

Optimized local agent models (Gemma 4, Qwen, Mistral, Nemotron) for RTX and edge devices

Advances autonomous driving - new Alpamayo 1.5 open model and Omniverse NuRec for scaling L4 systems; expanded partnerships with Hyundai, Kia and Uber on the DRIVE Hyperion platform; BYD, Geely, Isuzu and Nissan are building L4-ready vehicles on the same platform, complete with the new Halos OS safety operating system

Advance physical AI - NVIDIA Cosmos, Isaac GR00T, new simulation frameworks, general availability of IGX Thor, and partnerships with leading players in robotics and industrial software

Launched collaborations with T-Mobile, Nokia and other telco leaders on AI-RAN and future 6G networks built as "AI-native" platforms

These moves reinforce the argument that NVIDIA isn't "just" dependent on the current generation of GPU datacenters - it is actively preparing for the next wave of demand (automotive, robotics, edge inference, 6G, industrial AI).

Cash flow, buyback and dividend: what's in it for the shareholder

Q1 FY27 is extremely strong from a cash flow perspective:

Operating cash flow: $50.3 billion (vs. $27.4 billion a year ago)

Capex + investment in intangible assets: approx. USD 1.8 billion

Free cash flow: USD 48.6 billion (Y/Y +86%)

Of this cash, NVIDIA used the following in the quarter:

~$19.3 billion for share repurchases

~$0.24 billion in dividends (at the old dividend of $0.01 per share)

plus ~$2.1 billion for taxes on employee stock plans

The newly approved dividend of $0.25 per share (to be paid on June 26, 2026, record date June 4) implies a nominal dividend yield of a tenth of a percent, but it is mainly a psychological signal - NVIDIA is moving from a "token" dividend to a more realistic level and explicitly confirming that it intends to systematically return a significant portion of FCF to shareholders.

The addition of USD 80bn to the buyback framework (on top of the remaining USD 38.5bn as of 1Q) is again a signal of management's belief that the current valuation is not a "bubble that will burst tomorrow", but that the cash generated can cover these buybacks in the long term.

Outlook for Q2 2027: growth continues

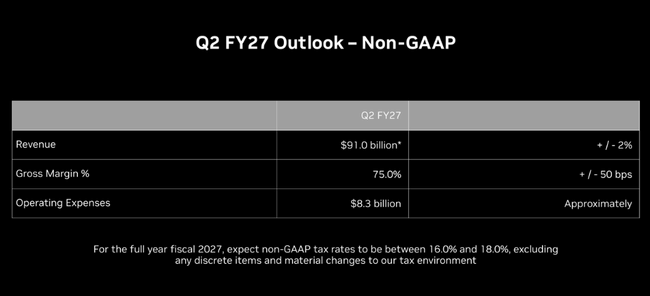

Q2 FY27Outlook:

Revenue: $91bn ±2% - roughly +11% Q/Q from an already record base

Gross margin (GAAP / non-GAAP): ~74.9% / 75.0% ±50 bps

Operating expenses: GAAP ~$8.5bn, non-GAAP ~$8.3bn

FY27 tax rate: 16-18% (GAAP and non-GAAP, excluding one-offs)

Key investor note: NVIDIA does not expect any Data Center compute revenue from China in this outlook. That said:

the risk of further regulatory tightening in China is already largely "in the numbers" - any further compute shortfalls would not hurt as much

a possible return/restoration of the product for China would, on the other hand, represent a positive surprise beyond the current outlook

How to read this as an investor: strengths and risks

What's most important:

NVIDIA continues to overwhelmingly outperform already high market expectations - both on revenue, earnings and cash flow.

Growth is primarily driven by datacenters where the combination of compute + networking shows that demand is not just for GPUs, but for the entire AI infrastructure.

The company is actively expanding its ecosystem (Google Cloud, Marvell, telco, automotive, robotics), building a "moat" beyond silicon itself.

Capital allocation is very aggressively pro-shareholder: high buyback, sharp dividend increase, commitment to return ~50% of FCF.

Key risks and issues:

Sustainability of pace - 85% revenue growth and 200%+ earnings growth per year is not sustainable over the long term; pace will inevitably slow, just not clear when and how sharply.

Concentration on the AI cycle - the company is heavily dependent on the investment cycle of "AI factories"; any overstatement of the return on these investments or a longer pause in CAPEX of hyperscalers would quickly eat into growth.

Regulation and geopolitics - especially China, export controls and pressure on "local champions" in individual countries. NVIDIA is trying to diversify, but risk remains.

Valuation - despite massive earnings growth, the stock often trades at very challenging multiples; the story must continue to deliver for valuations to "hold".