The energy sector has experienced a major boom in the past year due to a combination of macroeconomic factors. One would have expected that there would be nothing interesting here. But that would be a big mistake.

The energy sector has been in the investors' sights all last year and was one of the few to withstand the big market downturn. This has been due to a confluence of macroeconomic, political and meteorological influences. Investors might say that all the opportunities here are gone and they need to move elsewhere. But that would be a big mistake. Indeed, such companies often thrive in almost any situation, and the recent decline in the sector's popularity could present interesting opportunities.

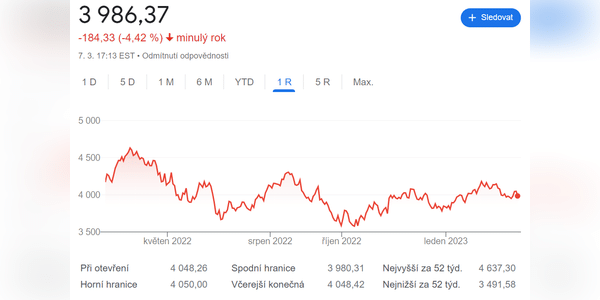

ConocoPhillips $COP

ConocoPhillips is a diversified oil and gas producer. It operates around the world and uses several methods to extract oil…