Dell’s latest quarter confirms that the company is no longer defined by the old rhythm of PCs and traditional servers. What once looked like a mature, cyclical hardware business is increasingly transforming into a critical pillar of the global AI build-out. The momentum is not coming from a temporary demand spike, but from Dell’s deep integration into large-scale data center deployments where speed, reliability, and execution matter more than brand visibility.

The real shift is strategic. Dell has positioned itself at the intersection of hyperscale computing, enterprise AI adoption, and mission-critical infrastructure. As AI workloads grow in complexity and scale, customers are prioritizing partners who can deliver complete systems, not just components. Q3 highlights that Dell is capturing this demand at an accelerating pace, reshaping both its revenue mix and its long-term investment profile.

How was the last quarter?

In the third quarter of fiscal year 2026, Dell Technologies $DELLrevenue reached $27.0 billion, representing 11% year-over-year growth and the highest level of revenue the company has ever reported in a third quarter. Growth was primarily driven by the Infrastructure Solutions Group segment, which benefited from unprecedented demand for AI servers and networking solutions.

Operating profit grew 23% year-over-year to $2.1 billion and net income reached $1.55 billion, up 32%. Earnings per share rose 39% to $2.28, while adjusted (non-GAAP) EPS reached a record $2.59. This development clearly shows that revenue growth is not being bought out by dramatic margin pressure, but instead is delivering operating leverage.

Cash flow is also a very important element of the quarter. Operating cash flow was $1.2 billion and adjusted free cash flow was $1.67 billion, more than double the same period last year. The company is thus generating enough cash not only to fund growth but also to return capital to shareholders. In the third quarter alone, Dell returned $1.6 billion to investors through dividends and buybacks.

A segment view: where growth is born

The segment was a key driver of results Infrastructure Solutions Group (ISG). Revenues for this segment were $14.1 billion, representing 24% year-over-year growth. Even stronger was the development in the server and networking segment, where sales grew 37% to $10.1 billion. It is here that the AI infrastructure boom is in full effect.

Dell reported record AI server orders of $12.3 billion in the quarter, and total AI order backlog reached $18.4 billion. Moreover, the five-quarter pipeline is many times higher than the current backlog, indicating that demand is far from ending. Moreover, the customer structure is diversified - it includes neocloud players, government projects and traditional enterprise clients.

Segment Client Solutions Group (CSG) achieved revenues of $12.5 billion, up 3% year-over-year. The commercial segment grew 5%, while the consumer segment declined 7%. Operating profit remained virtually unchanged year-over-year, confirming that the PC business is stable but no longer the main source of the company's growth or investment story.

Management commentary

CFO David Kennedy called the third quarter a confirmation that fiscal 2026 will be a record year for Dell. The company raised its AI server shipment estimate to about $25 billion, which implies year-over-year growth of more than 150%. According to management, Dell has become the partner of choice for customers who need to rapidly deploy large-scale AI clusters while requiring global support.

COO Jeff Clarke emphasized that Dell's key competitive advantage is not just the hardware itself, but the ability to design, deliver and operate complex, customized solutions. It is this capability that is critical in an environment where AI infrastructure is becoming a critical part of customers' businesses.

Outlook

The company's outlook remains very strong. For the full fiscal year 2026, Dell expects revenue in the range of $111.2 billion to $112.2 billion, which would represent 17% year-over-year growth. Adjusted earnings per share are expected to reach approximately $9.92, representing 22% growth.

For the fourth quarter, the company expects sales of around USD 31.5 billion, up more than 30% year-on-year. These estimates reflect not only a strong backlog, but also the continued acceleration of AI investments across the market.

Long-term results

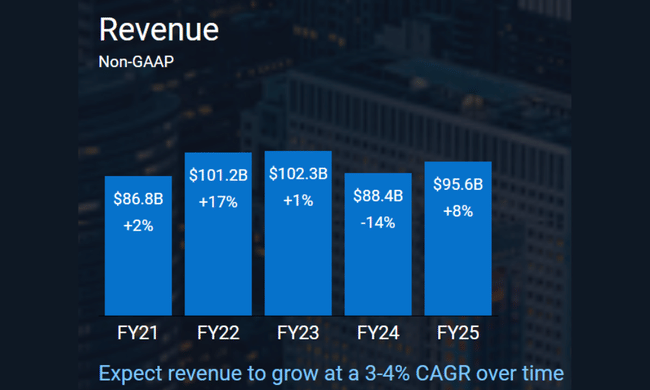

A look at the long-term numbers clearly shows that Dell has undergone a fundamental transformation. Between 2021 and 2024, revenues were mostly in the $85-102 billion range, with strong cyclical trends. In 2024, the company came under pressure due to the downturn in the PC market, which translated into a decline in sales and margins.

However, profitability remained relatively stable. Operating profit has fluctuated between $3.7 billion and $5.8 billion over the past four years, while EBITDA has long oscillated between $8 billion and $12 billion. The key difference from the past is now the structure of growth - instead of volumes in the PC business, Dell is growing through higher value-added infrastructure.

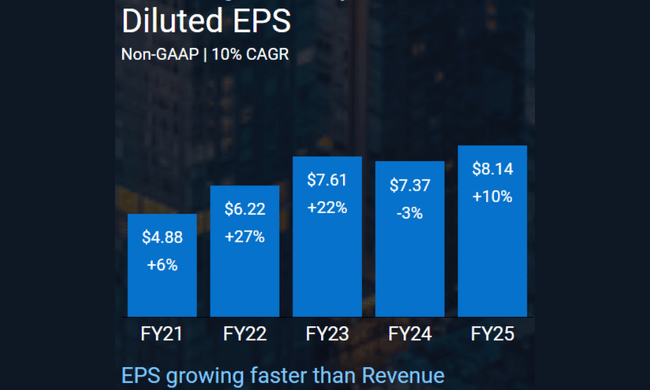

Net income in 2024 was $3.39 billion and EPS was $4.71. However, with the current momentum of the AI segment, these historical numbers are becoming less consistent with the company's future potential. Importantly, Dell has also been systematically reducing the number of shares outstanding, which has supported EPS growth and return on equity.

Shareholder structure

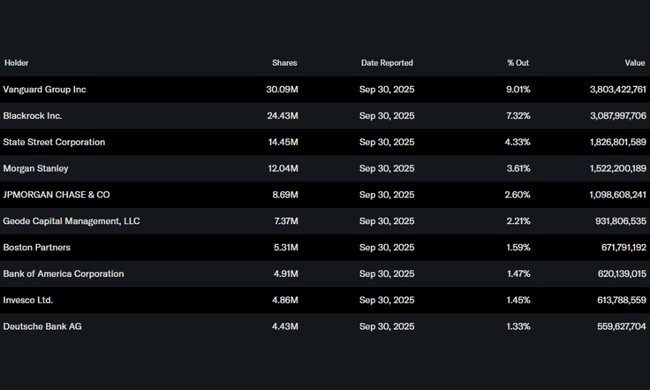

Dell has a strong institutional base. Institutional investors hold approximately 74% of the stock, with Vanguard, BlackRock, State Street and Morgan Stanley among the largest. Insider ownership of 6.5% ensures a relatively good alignment of management interests with shareholders.

Analyst expectations

Analysts increasingly agree that Dell is one of the purest "AI infrastructure plays" among traditional technology firms. The key question remains the sustainability of current growth rates and margins in an increasingly competitive environment. However, results to date show that Dell can not only capture the AI boom, but also monetize it effectively.