At first glance, the latest quarter looks like a familiar Apple storyline: a blockbuster iPhone cycle, record profitability, and a surge in cash generation. But the more important signal sits beneath the headline numbers. After a muted phase in 2023–2024, Apple is no longer relying on isolated product strength to stabilize growth. The recovery appears broader, more synchronized across regions, and structurally stronger.

What stands out for investors is the ecosystem effect. Hardware demand translated into higher services revenue, a growing active installed base, and operating leverage that reinforced margins rather than diluted them. This combination reframes the quarter from a one-off peak to a potential reset point. The implicit question is not whether Apple can repeat such results every quarter, but whether this breadth of performance restores long-term confidence in the growth engine itself.

What was the last quarter like?

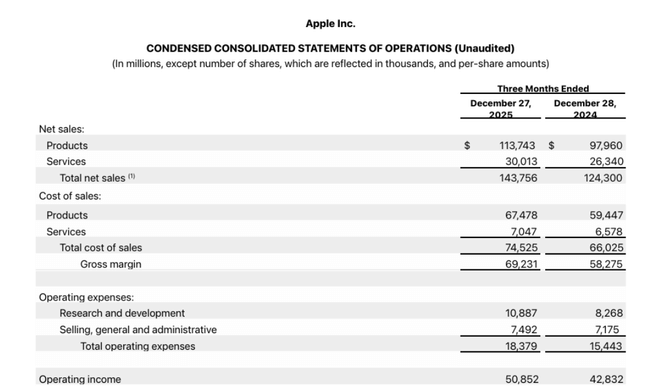

Apple $AAPL reported fiscal Q1 2026 revenue of $143.8 billion, up 16% year-over-year. This is an all-time record quarterly revenue for the company. Products were the main driver, with sales growing from $98.0 billion to $113.7 billion, up more than 16% YoY, while the services segment continued its steady double-digit growth rate, reaching $30.0 billion, up +14% YoY.

Profitability remained exceptionally strong. Gross profit rose to USD 69.2bn compared to USD 58.3bn a year ago, while gross margin remained at a very high level despite rising manufacturing and development costs. Operating profit reached USD 50.9 billion, up almost 19%, and net profit rose to USD 42.1 billion, up 16% year-on-year.

Earnings per share underlined the quality of these results. Diluted EPS came in at $2.84, up 19% year-over-year, despite an already very high comparative base from last year. The positive impact was not only from the growth in operating profit, but also from the continued reduction in the number of shares outstanding as a result of massive share buybacks.

Looking at the individual product categories in more detail, iPhone in particular stands out, with sales jumping from USD 69.1 billion to USD 85.3 billion, up more than 23% YoY. iPhone had its best quarter ever, across all geographic segments. At the same time, services maintained its role as a stable pillar with high margins and increasing revenue predictability.

CEO commentary

CEO Tim Cook called the quarter a record one and highlighted that results significantly exceeded internal expectations. He said iPhone's growth was driven by unprecedented demand across all regions, while also seeing another all-time high in services. Also of critical note was that Apple's installed base now exceeds 2.5 billion active devices, further reinforcing the long-term monetization potential of the ecosystem.

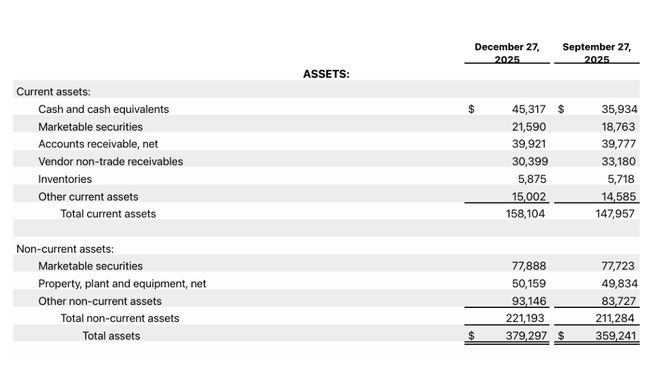

CFO Kevan Parekh added that the combination of record revenue and high margins led to an all-time high EPS for a single quarter. He said Apple generated nearly $54 billion of operating cash flow during the quarter, which allowed it to return nearly $32 billion to shareholders through dividends and buybacks.

Long-term results

A look at Apple' s long-term results shows that the company has regained a path to sustainable growth after a weaker 2022-2023 period, thanks largely to a combination of pricing power, service expansion and disciplined cost management. Revenues in fiscal 2025 reached $416.2 billion, up 6.4% year-over-year after a virtually flat 2024. This return to growth came in an environment where global demand for consumer electronics remained subdued, underscoring Apple's relative resilience to cyclical market swings.

2022 was still a reverberation of the exceptionally strong demand for electronics from the pandemic years. Revenues reached $394.3 billion, but even then there was a noticeable slowdown - particularly for iPhone and Mac. Operating profit was USD 119.4 billion and net profit was USD 99.8 billion. Margins remained high, but Apple faced pressure from rising costs, disrupted supply chains and a strong dollar. EPS was around $6.15, with the positive effect of buybacks no longer able to fully offset slowing revenue growth.

2023 marked the first full year of decline. Revenues fell 2.8% to USD 383.3 billion, operating profit declined to USD 114.3 billion and net profit to USD 97.0 billion. This was not due to a loss of market position, but to normalising consumer demand, weaker Mac and iPad sales and more conservative consumer behaviour in a high interest rate environment. However, Apple maintained an exceptionally high operating margin and continued to aggressively repurchase shares, which kept EPS virtually stable around $6.16. This was a key signal that the business was structurally resilient.

The year 2024 brought stability. Revenue increased slightly to USD 391.0bn (+2.0%), operating profit rose to USD 123.2bn and net profit reached USD 93.7bn. Growth was driven primarily by the services segment, which increased its share of total revenue and improved margin quality. Cost discipline improved and Apple began to benefit from operating leverage again. EPS may have stagnated around $6.11 year-over-year, but looking at the structure of the results, it was clear that the company was setting the stage for a return to more dynamic growth.

News

The most significant operating news is the crossing of the 2.5 billion active devices mark, further increasing the value of the Apple ecosystem. This milestone reinforces the long-term story of services benefiting from high user loyalty. At the same time, the company announced another dividend payout and continued massive returns on capital that make Apple one of the most attractive companies in terms of the combination of growth and stability.

Apple's results come at a time when the company is significantly accelerating its strides in artificial intelligence. Shortly before the earnings release, news emerged that Apple was buying the startup Q.AI for about $2 billion. The company's technology focuses on reading the subtle micro-movements of facial expressions, which may pave the way for Apple to create a new type of interaction between the user and the AI assistant. In practice, this is a move towards "non-verbal communication", where the device could respond not only to voice or text but also to subtle visual cues, which fits into Apple's long-term strategy of combining hardware, software and user experience.

Even more fundamental from an investment perspective is the strategic collaboration with Google. Apple and Google have jointly confirmed that Apple will leverage Gemini models and Google's cloud infrastructure to bolster its AI capabilities, including a heavily personalized version of Siri that is due to arrive later this year. The move shows Apple's pragmatic approach: instead of trying to develop the entire AI stack entirely in-house, the company is combining its own ecosystem with the best available third-party technology. This can significantly shorten the time it takes to bring competitive AI features to market and reduce the risk of Apple falling behind competitors in this area.

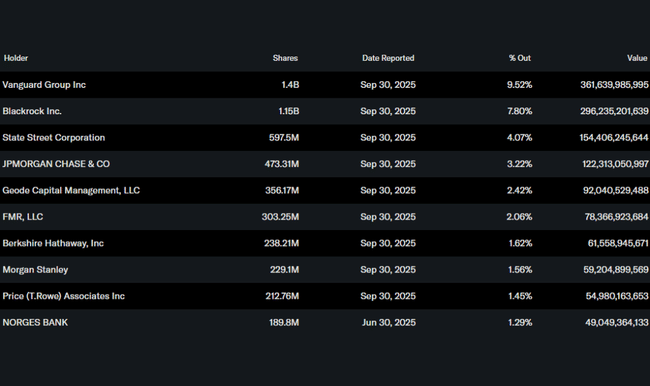

Shareholding structure

Apple's shares are heavily represented by institutional investors, who hold approximately 65% of the outstanding shares. The largest shareholders include Vanguard Group, BlackRock and State Street, confirming the perception of Apple as a key long-term pillar of the portfolios of large global asset managers.

Analyst expectations

The analyst consensus continues to improve following these results. In particular, the market is pricing in a return to double-digit revenue growth, record iPhone performance and exceptionally strong cash generation. Apple continues to be viewed as a combination growth and defensive stock that can generate stable earnings, high cash flow and attractive returns on capital at various stages of the cycle.