Philip Morris International closed the year 2025 as a company that had one of the most successful chapters in its modern history. The company not only managed another year of volume growth in an environment of structural decline in the conventional tobacco market, but more importantly, clearly confirmed that the smokeless transformation has become a major source of revenue, margins and long-term shareholder value. The fourth quarter and full year results show that PMI is able to combine stable cash flow from its traditional business with the fast-growing IQOS, nicotine sachets and e-vapor product segments.

From an investment perspective, the key is that this transition is taking place without losing financial discipline. The company is generating high operating profits, increasing earnings per share at a double-digit rate while maintaining one of the most attractive dividends among global consumer titles. Thus, 2025 is not just a good year in the cycle, but a confirmation of a structural change in the business model.

How was the last quarter?

The fourth quarter of 2025 delivered $PM solid, balanced growth across its core businesses. Total revenue reached $10.4 billion, up 6.8% year-over-year, or 3.7% when adjusted for currency effects. Growth was driven primarily by the smokeless portfolio, which continues to increase its share of both revenue and gross profit.

Gross profit in the quarter rose to $6.8 billion, up 8.3%, confirming that new products have a higher margin profile than traditional cigarettes. Operating profit was $3.4 billion and grew 4.5% on an organic basis, despite continued investment in smokeless category expansion and marketing of key brands.

Profitability was positively reflected in earnings per share. Reported diluted earnings per share were $1.37, while adjusted diluted EPS was $1.70, up nearly 10% year-over-year. Excluding currency effects, EPS growth was around 9%, a very strong result in a mature consumer market environment.

In terms of volumes, the trend is quite clear. Total shipments grew only marginally, by 0.1%, but smokeless products grew by 8.5%, while volumes of conventional cigarettes fell by 2.2%. Thus, even in quarterly terms, the PMI clearly demonstrates that volume growth is now exclusively the domain of smokeless categories.

CEO commentary

In his comments, CEO Jacek Olczak described 2025 as an exceptionally strong year, not only in terms of results, but above all in terms of the company's strategic shift. He highlighted that Philip Morris has achieved its three-year targets for growth in operating profit and earnings per share in just two years, which he said clearly confirms the soundness of the transformation towards smoke-free products.

Olczak also pointed out that the company is at a stage where the smoke-free portfolio is no longer an add-on, but a core pillar of the business. More than 40% of sales and nearly 43% of gross profit now come from smokeless products, with the share exceeding 50% in a number of key markets and even 75% in some. Management believes this fundamentally changes the company's risk profile and long-term growth potential.

At the same time, the CEO openly acknowledged that the regulatory environment and pricing pressures will be more challenging in the coming years, but he believes the company is able to meet these challenges without disrupting its dividend policy thanks to strong brands, geographic diversification and high margins.

Outlook

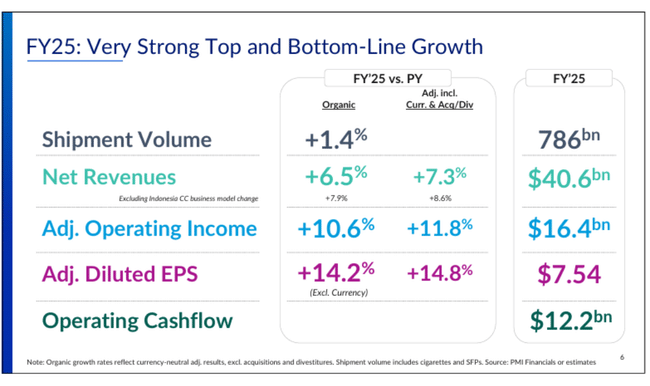

The outlook for 2026 confirms that PMI is entering its next phase of growth with very solid visibility. The company expects reported diluted earnings per share in the range of $7.87 to $8.02, with adjusted EPS of $8.38 to $8.53 after adjusting for one-time items. That translates into expected year-over-year growth of 11% to 13%, an exceptionally strong pace for a company of this size.

Excluding currency effects, PMI is targeting EPS growth of 7.5% to 9.5%, showing that even in a more conservative scenario, the company is still generating high single-digit growth. At the same time, management expects organic revenue growth in the range of 5% to 7% and operating profit growth of 7% to 9%.

Operationally, cigarette volumes are expected to continue to decline by approximately 3%, more than offset by high single-digit to low double-digit growth in smokeless products. Capital expenditures of $1.4 billion to $1.6 billion remain fully focused on supporting the smoke-free portfolio, not on sustaining a declining traditional business.

Long-term results

A look at Philip Morris International's long-term trajectory from 2021 to 2024 shows a company that has gone through a challenging business model transformation, with short-term swings in profitability, while gradually laying the groundwork for a qualitatively different growth profile. In 2021, revenues were roughly $31.4 billion, and the revenue structure at the time was still heavily dependent on conventional cigarettes. Gross profit was around $21.4 billion, operating profit just under $13 billion and margins were stable, but already facing long-term volume pressure in the traditional tobacco segment.

2022 represented a watershed but difficult period. While sales rose slightly to $31.8 billion, gross profit fell year-on-year and operating profit declined by more than 5%. This development was not a sign of weaker business, but the result of a deliberate management decision to accelerate investment in smokeless products, technology development, manufacturing and marketing. At the same time, results were negatively impacted by currency effects, tax items and one-off restructuring costs. Earnings per share stagnated in the year, which raised questions at the time about the short-term profitability of the entire transformation.

The year 2023 can be described as a transition phase between the investment cycle and the return of operating leverage. Revenues have already grown significantly, by more than 10% to $35.2 billion, mainly due to the rapidly growing share of smokeless products. Gross profit was up nearly 9.5%, the first clear sign that the new product mix is starting to improve the company's margin profile. Still, operating profit fell nearly 6% year-on-year as PMI continued to absorb the high costs associated with the expansion of IQOS, ZYN and other smokeless brands into new markets. The year was an uncomfortable one in terms of results, but a strategically crucial one - the company sacrificed some short-term profitability in favor of future dominance in high-growth categories.

The turning point came in 2024. Revenues reached nearly $37.9 billion, a 7.7% year-over-year growth rate, but this time the growth was no longer bought down by margin pressure. Gross profit rose more than 10% to $24.5 billion, while operating expenses grew at a significantly slower rate than sales. This led to an increase in operating profit of almost 16% to $13.4 billion and a clear return of operating leverage. EBITDA even grew by almost 18%, confirming that the investment phase of the transformation was largely complete.

From an earnings per share perspective, the long-term picture is more complex. Between 2021 and 2024, EPS fluctuated due to tax changes, one-off costs and currency effects, but adjusted performance gradually accelerated. Crucially, the quality of profits has improved significantly, with an increasing proportion of profits coming from smokeless products with higher margins, lower long-term capital intensity and greater price flexibility than conventional cigarettes.

News

2025 was an exceptionally strong year in terms of product portfolio. PMI's smokeless products are now available in 106 countries and have over 43 million users. The IQOS brand maintains its dominant position in the heated tobacco category and continues to increase share in key European and Asian markets.

ZYN nicotine sachets have become one of the fastest growing nicotine products in the US and beyond, gradually building a global brand with high price discipline. E-vapor products under the VEEV brand are approaching operational profitability and expanding their presence into new markets without the company resigning to strict regulation and control of the target audience.

Shareholding structure

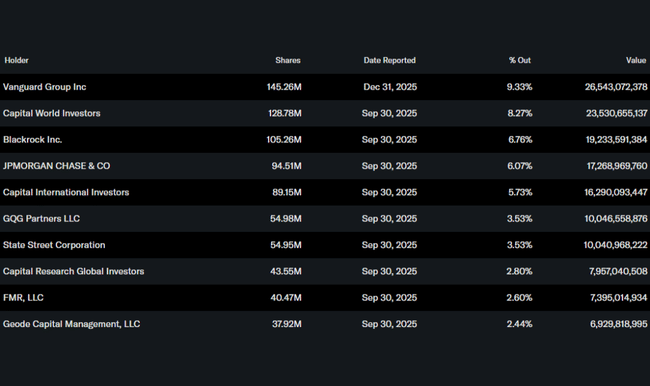

The ownership structure remains highly stable. Over 82% of the shares are held by institutional investors led by Vanguard, Capital World Investors and BlackRock. This creates long-term pressure to maintain strong cash flow, earnings per share growth and a consistent dividend policy, which is fully in line with PMI's current strategy.

Analyst expectations

Analyst consensus views Philip Morris International's results as mostly positive. In particular, experts praise the company's ability to translate the structural downturn in the cigarette market into long-term sustainable growth through smokeless products. The outlook for double-digit growth in adjusted EPS and the confirmation of long-term targets for the 2026-2028 period are also viewed positively.

On the other hand, analysts warn of regulatory risks, particularly in terms of taxes and marketing restrictions, and a possible slowdown in consumer demand in some emerging regions. Nevertheless, Philip Morris is often cited as the best-positioned player in the sector, able to combine growth, high profitability and an above-average dividend.