UnitedHealth Group enters 2026 as the world’s largest health insurer by scale, yet the latest results show that size alone no longer guarantees comfort. 2025 delivered double-digit revenue growth and solid cash generation, but it also exposed a growing imbalance between volumes and profitability. Medical cost inflation, regulatory pressure, and weaker margins in key segments are now front and center.

The market is treating 2026 as a transition year. Management talks about tighter discipline and a reset, but guidance suggests that a return to prior profitability levels will take time. UnitedHealth remains a high-quality franchise, but investors are grappling with a risk profile that looks less predictable than it did in recent years.

How was the last quarter?

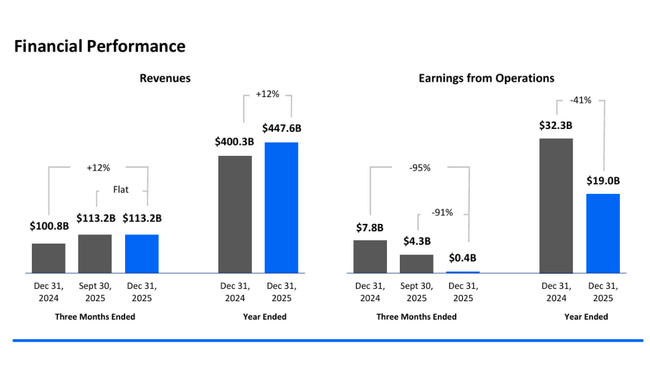

The fourth quarter of 2025 was the weakest quarter for UnitedHealth Group $UNH in terms of profitability in several years, although revenues remained strong. Revenues in the quarter were approximately $113.2 billion, representing year-over-year growth of approximately 12%, driven primarily by continued growth in the number of insureds in the Medicare and Community & State segments and volume growth in Optum Rx. Thus, at the revenue level, the company is not facing a demand problem, but a cost structure problem.

Operating profit in the fourth quarter, however, fell to just $0.4 billion, down from $4.3 billion in the same period last year. The main reason was a one-time charge of $1.6 billion after tax, which included final costs related to the cyberattack, portfolio restructuring, exits from unprofitable businesses and revisions to loss-making insurance contracts. After including these items, reported earnings per share were only $0.01, an extreme drop from the company's historical norm.

On an adjusted basis, earnings per share came in at $2.11, which better reflects the normal performance of the business, but even that figure fell short of what investors have long been accustomed to at UnitedHealth. The key negative factor remains the medical care ratio, which rose to 88.9% on an adjusted basis, up from 85.5% a year earlier. This 340 basis point increase represents a significant deterioration in profitability leverage - for every dollar of premium, significantly more is now spent on health care itself.

The operating expense ratio was 12.9% on an adjusted basis and remained roughly stable year-over-year, suggesting that the problem lies not in administrative costs but in the cost of care provided. Cash flow from operations in the quarter remained solid, but its structure was impacted by the timing of payments that would normally fall in 2026.

Outlook for 2026

The outlook for 2026 is solid at first glance, but on closer reading rather defensive. The company expects revenue to exceed $439 billion, which would imply only low single-digit growth over 2025. Operating profit is expected to exceed $24 billion and adjusted earnings per share are expected to be above $17.75, with the low end of reported EPS at $17.10.

The key takeaway is that this outlook already fully reflects higher healthcare costs, the impact of the Inflation Reduction Act, lower Medicare funding from CMS, and continued margin pressure in the UnitedHealthcare segment. In other words, management openly admits that a return to the old 2021-2023 margins is not realistic.

The efforts to price discipline and reprice insurance products are positive signs, but these steps will be delayed. Thus, 2026 will be a year of stabilisation rather than growth acceleration.

Management comment

CEO Stephen Hemsley described 2025 as a watershed year in that the company "faced the challenges head on" and took painful but necessary steps. In particular, he highlighted Optum's reorganisation, management turnover and return to integrated value care. According to management, it is the second half of 2025 that lays the foundation for more sustainable growth in the years ahead.

At the same time, however, management does not appear overly optimistic. The language of communication is cautious, with an emphasis on discipline, transparency and cost management rather than expansion or aggressive growth. This in itself explains why the market reacted restrainedly after the results.

Long-term results

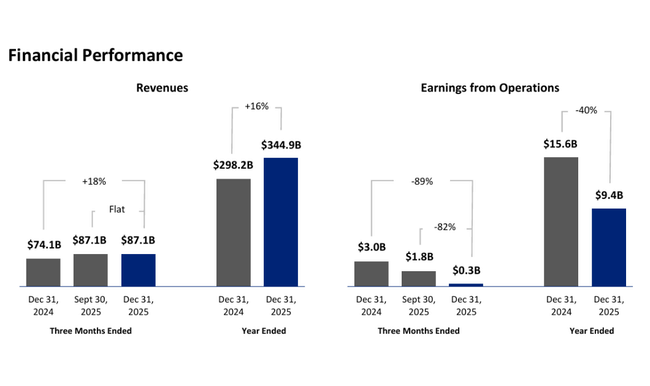

Looking at UnitedHealth Group's long-term development, it is evident that the company has dramatically increased its scale over the past four years, but 2024 marked a turning point in the quality of that growth. Revenues grew from $287.6 billion in 2021 to $324.2 billion in 2022, then to $371.6 billion in 2023, and reached $400.3 billion in 2024, a cumulative growth of more than 39% in three years. This growth has been driven by a combination of acquisitions, demographic trends and the expansion of public health programs.

However, the cost side grew even faster. Cost of revenues increased from $217.9 billion in 2021 to $244.5 billion in 2022, $280.7 billion in 2023, and up to $310.9 billion in 2024. As a result, costs grew nearly 11% year-over-year in 2024, while revenues grew only 7.7%. This led to gross profit falling to US$89.4 billion, a 1.7% year-on-year decline, the first real drop in gross profitability after years of expansion.

Operating profit was flat in 2024 at US$32.3 billion, virtually unchanged from 2023, despite strong revenue growth. This clearly shows a loss of operating leverage. An even more pronounced deterioration can be seen at the level of net profit, which fell to US$14.4 billion in 2024 from US$22.4 billion in 2023, a drop of more than 35%. Earnings per share fell from US$24.12 to US$15.64, a fundamental change in the profitability profile of the entire group.

EBITDA declined to US$28.1 billion in 2024, down nearly 23% year-on-year, while growing at a double-digit rate between 2021 and 2023. This development confirms that UnitedHealth has entered a phase where volume growth no longer automatically means profit growth, and the ability to control healthcare costs and adapt pricing to the regulatory environment is becoming a key issue.

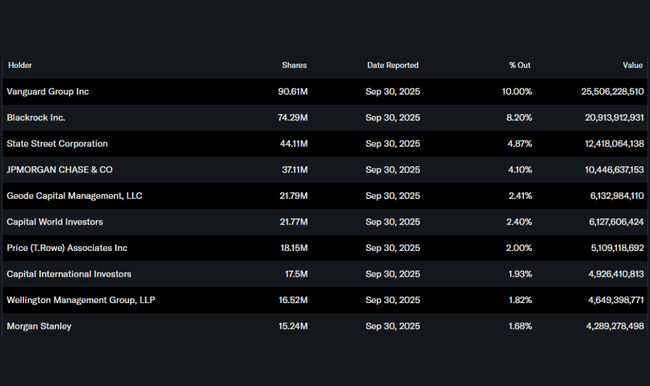

Shareholder structure

UnitedHealth has a stable institutional base. The institution holds roughly 84% of the stock, with the largest shareholders being Vanguard (10.0%), BlackRock (8.2%) and State Street (4.9%). Insider ownership remains low, which is standard for a company this large.