Consumer staples finished 2025 with a simple test. Pricing power was harder to lean on, volumes were uneven, and costs did not fully normalize. In that setup, investors cared less about a single flashy number and more about whether a company could keep profit growth steady while the consumer environment stayed mixed.

PepsiCo’s Q4 2025 delivered that kind of stability. The company accelerated revenue growth and improved operating efficiency, which supported a double-digit increase in earnings per share. Management also reaffirmed its 2026 outlook and raised the dividend again, extending its long history of dividend growth. The broader message is that PepsiCo’s mix across regions and categories helps it balance weaker conditions in North America with stronger momentum in emerging markets.

How was the last quarter?

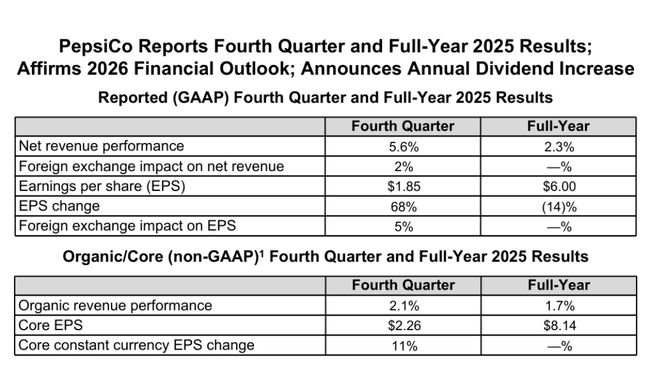

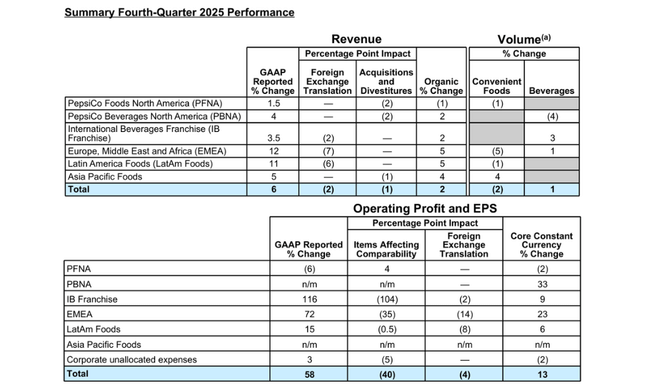

The fourth quarter of 2025 delivered 5.6% year-over-year revenue growth on a GAAP basis, with organic growth of 2.1%. More importantly, however, was the acceleration in momentum from previous quarters, which management specifically identified as sequential acceleration. This was driven by both the North American business and international operations, which has long been a key stabilizing element for PepsiCo $PEP.

Profitability has improved significantly more than sales alone. GAAP earnings per share jumped to $1.85, up 68% year-over-year, while adjusted earnings per share reached $2.26, up 11% year-over-year at constant currencies. This difference clearly demonstrates how strongly one-off items factored into last year's results, particularly on a 2024 comparative basis.

From a segment perspective, the quarter was characterised by significant divergence. PepsiCo Foods North America faced a 6% decline in operating profit, mainly due to higher operating expenses, restructuring charges and the absence of exceptional positive items from the prior year. Conversely, the Beverage Division in North America benefited from the unwinding of depreciation and an improved price mix. The international segments, particularly Europe, Middle East and Africa, recorded very strong operating profit growth, supported by a combination of pricing, savings and favourable currency developments.

Overall, the quarter is evidence that PepsiCo can sustain profitability growth in an environment of slowing demand, primarily through cost discipline and selective price increases.

CEO commentary

In his comments, CEO Ramon Laguarta highlighted in particular the acceleration in sales growth and operating margins, which he said confirmed the soundness of the strategic moves made in recent years. He highlighted the strong productivity savings that have made it possible to finance investments in brands and innovation without negatively impacting profitability.

Laguarta said the company enters 2026 with a clear plan: to reinvigorate key global brands, expand product innovation in functional and "better for health" categories, and offer consumers more attractive value in an environment of increasing price sensitivity. It also announced a 4% increase in its annual dividend, marking PepsiCo's 54th consecutive year of dividend growth, underscoring its position among the most stable dividend-paying stocks in the market.

Outlook for 2026

Management reaffirmed guidance that calls for organic revenue growth in the range of 2-4% and adjusted earnings per share growth of 4-6% at constant currencies. Including the favourable currency effect and acquisitions, this outlook implies overall revenue growth of around 4-6% and EPS growth of around 7-9%.

PepsiCo also expects capital expenditures to remain below 5% of sales and free cash flow conversion to exceed 80%. It plans to return about $8.9 billion to shareholders in 2026, most of which will be in dividends, supplemented by a smaller amount of buybacks.

Long-term results

A look at 2021 to 2024 shows a very consistent growth profile. Revenue has increased from just under US$79.5 billion in 2021 to almost US$91.9 billion in 2024, with growth driven by both volumes and a successful long-term pricing strategy. Gross profit grew even faster than sales, reflecting the company's ability to pass on higher costs to consumers while optimizing manufacturing processes.

Operating profit increased from roughly $11.2 billion to nearly $12.9 billion during the period, with margins improving steadily despite inflationary pressures. Net profit grew steadily, from US$7.6 billion in 2021 to US$9.6 billion in 2024, and earnings per share increased from US$5.51 to US$6.98. An important element of this development is the gradual reduction in the number of shares outstanding, which supports EPS growth even at a more moderate rate of net income growth.

Over the long term, it is evident that PepsiCo is not an explosive growth company, but rather a defensive compounder that combines low single-digit growth rates with high cash flow stability and regular dividend increases.

Shareholder structure

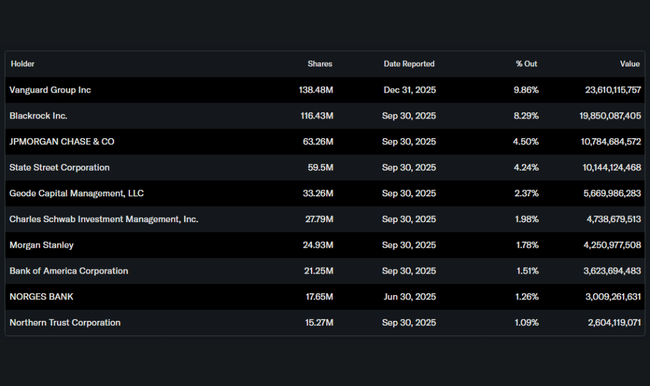

The ownership structure remains very stable and institutionally oriented. Approximately 80% of the shares are held by institutional investors, with Vanguard, BlackRock, JPMorgan and State Street among the largest. Insider participation is minimal, which is typical for a company of this size and maturity.

Analyst expectations

Analysts generally view PepsiCo as a stable title with limited risk but also limited growth potential. The consensus focuses on continued low-to-mid single-digit revenue growth, stable margins and an attractive dividend yield. Expectations for 2026 are near management's confirmed guidance, with the evolution of consumer demand in North America and the company's ability to continue to offset cost pressures with pricing and productivity remaining key drivers.