Mining is often judged as if every dollar of higher EBITDA automatically means more cash for shareholders. Rio Tinto’s 2025 is a good reminder that the link breaks when a company moves into a heavier investment phase. The operating picture improved, but the cash left after spending shrank.

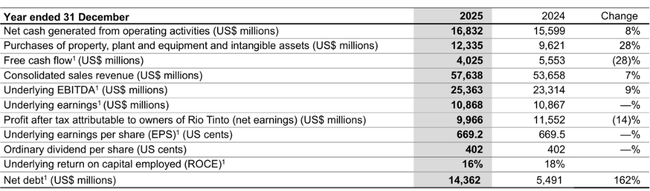

Rio reported revenue of $57.6B (+7%) and EBITDA of $25.4B (+9%). The mix mattered: copper and aluminum carried more of the momentum, while iron ore was less of a simple profit engine, helped by tighter cost control. Net profit was $10.9B and operating cash flow reached $16.8B, supporting the dividend profile. The trade-off shows up below the line: free cash flow dropped 28% to $4.0B as capex jumped 28% to $12.3B. Net debt rose sharply to $14.4B from $5.5B, reflecting that the company is funding future growth—copper, lithium and new projects—while accepting lower near-term cash and higher cycle sensitivity.

What was 2025 like?

The company built on 3 pillars last year: a record iron ore run rate from the Pilbara since April, the completion of the Oyu Tolgoi underground and the first iron ore ship from Simandou in December. These are three specific milestones that explain why Rio $RIO is highlighting +8% CuEq (copper equivalent) production growth and why EBITDA grew faster than revenue.

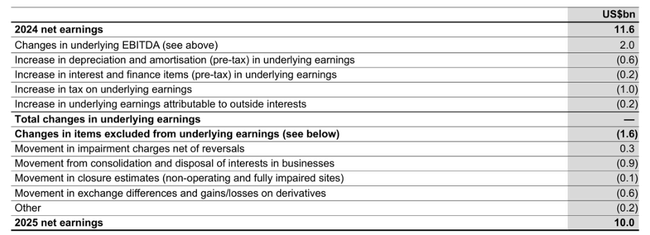

On a purely financial basis: operating cash flow was $16.8 billion (+8%), underlying EBITDA was $25.4 billion (+9%) and underlying earnings were essentially unchanged at $10.9 billion. Net income attributable to shareholders declined 14% to about $10.0 billion, a typical picture of a year in which the pricing environment is changing while reflecting taxes, royalties and one-time items differently in the accounts than in the "underlying" metrics. At the capital discipline level, the most visible jump is in investments: capex of $12.3 billion (+28%) pulled free cash flow down to $4.0 billion (-28%). And that's the difference between "operating performance" and "cash to shareholders" in any given year.

In terms of operational reasons, the company explicitly attributes the improvement mainly to the ramp-up of Oyu Tolgoi and the performance of Pilbara. In the background, on the other hand, it's clear that iron ore no longer forms as dominant a cushion as it used to and that Rio has to rely more on diversification into copper, aluminium and now lithium. This is a structural change that may stabilize cash flow across the cycle over time, but also means a higher investment phase today.

CEO commentary

Simon Trott openly builds communication on two lines. The first is safety and reputational risk: following the fatal incident at the Simandou project, he stresses "safety first" and full investigation, which is also critical for mining companies in terms of licensing and regulatory relations. The second is "stronger, sharper, simpler" corporate governance: tougher cost discipline, simplification of the organisational structure and moving decision-making closer to operations. Between the lines, it is a signal that Rio wants to translate volume growth into higher margins and that it does not want to run the investment cycle "on debt" with no return.

Outlook

The outlook for 2026 is built on iron ore stability and that new resources (Simandou) will start to add volume. Rio forecasts total iron ore sales at 343-336 million tonnes, with Pilbara (on a 100% basis) forecast at 323-338 million tonnes. Simandou is expected to contribute 5 to 10 million tonnes (on a 100% basis) for the first time, which is mainly a confirmation to the market that the project is moving from "story" to top-line.

For copper, the outlook is 800 to 870 thousand tonnes (on a consolidated basis), which in the company's context is more about "keeping the momentum" after a strong year and continuing to ramp up sharply where we can. Aluminium and bauxite are more normalising: bauxite 58 to 61 million tonnes, aluminium 3.25 to 3.45 million tonnes. Lithium (LCE) 61 to 64 thousand tonnes suggests Rio wants to ramp up this pillar faster - and it will be the part that will be most under the microscope, as lithium is both cyclical and capital intensive.

Long-term results

Rio Tinto's performance over the past four years clearly shows how sensitive the bottom line is to the commodity cycle and how important it is that the portfolio shifts towards copper and other metals. Revenues have fallen from $63.5 billion in 2021 to $55.6 billion in 2022 and held around $54 billion in 2023 and 2024, which is typical after an extremely strong post-covide period. Revenues pick up to 57.6 billion in 2025, but the quality of the growth is more important than the number itself: higher contributions from copper and aluminum partially offset pressure from iron ore.

At the profitability level, we see a gradual return of operating leverage: EBITDA rose to $25.4 billion in 2025, according to the company report, while underlying earnings remained stable at around $10.9 billion. In practice, this means that Rio is improving its operations and cost base, but net profit is still impacted by taxes and revenue structure across segments. That said, the biggest "volatility" going forward will not just be in pricing, but also in how quickly new projects translate into stable cash flow.

But the key detail of the last year is capital intensity. Capex has grown to $12.3 billion and free cash flow has fallen to $4.0 billion. From an operating leverage perspective, this makes sense: the company is investing in a pipeline to lift CuEq production by about 3% a year through 2030, but in the short term this reduces the "cash cushion" for buybacks or extraordinary payouts. This is the main axis of the Rio story for investors for several years to come.

News

The year 2025 was very much about project execution for Rio. The Oyu Tolgoi underground is complete, Simandou managed its first shipment in December and the Western Range opened on time and on budget in the Pilbara. On top of that, the company has kicked off construction of additional brownfield replacement mines in the Pilbara, exactly the type of investment to keep volumes and costs under control in the key cash cow segment.

Lithium is also strategically important: the Arcadium acquisition closed in March and Rio is framing it as a path to deliver capacity of around 200,000 tonnes of LCE per year by 2028. That's a big bet - potentially value-creating, but also cyclical and investment-intensive. The other significant thing is the productivity program: management cites annualized savings of $650 million (part already realized, the rest delivered by the end of Q1 2026) and a structural target to improve unit costs over the long term.

Shareholder structure

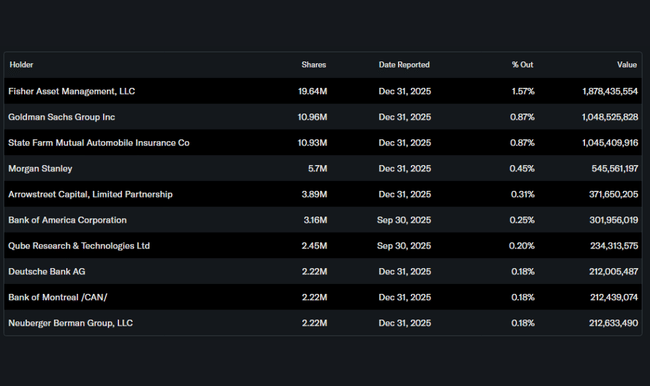

According to the data, the insider share is negligible and institutional holdings come out relatively low relative to how large and globally tracked Rio is. Practically, however, the main thing that matters to an investor is that it is a very liquid title with a broad shareholder base, where much of the capital flow is from global funds and index managers. The largest institutional holders cited include Fisher Asset Management, Goldman Sachs, State Farm and Morgan Stanley.

What this means in practice: with Rio, it is typically not decided by "one activist player" but rather how the market as a whole reads the commodity cycle, Chinese demand, cost developments in Australia and the pace of copper-lithium delivery.