Snowflake finished the quarter with clear signs that demand is not slowing. Revenue growth remained strong, and existing customers continued to expand their spending, which is one of the most important signals for a usage-based software company. At the same time, the company reported a sharp rise in contracted future revenue, which suggests the sales engine is still working well for the coming quarters.

Investors also liked the “quality” side of the results. Snowflake generated strong free cash flow and showed a very high cash margin, which supports the idea that growth is becoming more efficient. On top of that, management’s outlook for the full year came in above what analysts expected, which is usually the detail that decides whether a good quarter turns into a positive re-rating.

How was the last quarter?

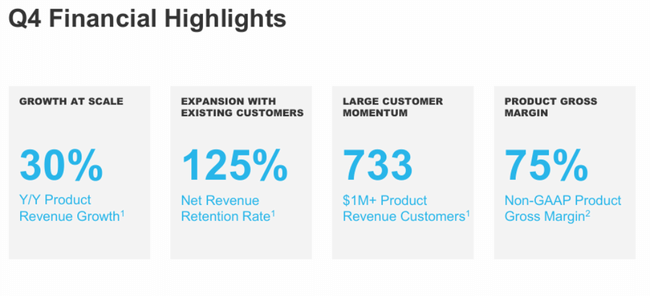

In the fourth quarter, Snowflake $SNOW delivered two numbers that can be read as direct evidence that the company is stabilizing after a turbulent year: 30% growth in core services revenue and, at the same time, 42% growth in contracted future revenue. The $1.28 billion in revenue isn't just a "nice round" number - it's mainly that the growth isn't built on one big customer, but on a broad base. The company added 740 net new customers, up 40% year-over-year, while continuing to grow its depth of relationships: 733 customers are already spending over $1 million a year, and the number of large customers over $10 million a year has reached record levels.

The second layer is the quality of the revenue. Revenue retention of 125% means that the average customer already using the platform continues to expand usage - and that's the healthiest type of growth in practice because it's cheaper than hunting for new names. This is backed up by the fact that contracted future revenues have jumped to $9.77 billion. For an investor, this is like a "future bill stock": contracted future consumption that will only gradually translate into reported sales.

The third layer is profitability and cash. After adjustments, Snowflake reported $139 million in operating profit and an 11% operating margin in the quarter, with core services gross margin of 75% after adjustments. At the same time, it's worth a fair explanation of the difference between profit and loss and cash: under standard accounting, the company reports an operating loss (-318 million in the quarter), but cash flow is very strong - operating cash of 781 million and free cash of 765 million. This is important, because with Snowflake, the market has long wondered whether it can grow while not "burning through" costs. Q4 shows that the cash engine is already significantly more robust than a year ago.

Top points of the results

Revenue in the quarter of $1.28 billion, +30% year-over-year.

Core services revenue of $1.23 billion, +30% YoY.

Revenue retention of 125%.

740 net new customers in the quarter, +40% year-over-year.

733 customers with annual core service revenues of over $1 million, +27% year-over-year.

Contracted future revenue of $9.77 billion, +42% year-over-year.

Core services gross margin after adjustments of 75% in the quarter.

Free cash of $765 million ( $782 million after adjustments), roughly 60% cash margin.

Full fiscal year 2027 outlook: core services revenue $5.66 billion(+27%).

CEO commentary

CEO Sridhar Ramaswamy builds the story on the fact that Snowflake is the infrastructure on which companies are building the use of AI safely and at scale. Crucially, it doesn't just rely on marketing: the leadership team backs its argument with numbers - rapid growth in contracted future revenue, steady retention of 125% and accelerating new customer inflows. CFO Brian Robins then puts the emphasis on two things the market wants to hear: the ability to bring in new customers in bulk while deepening relationships with existing ones, as seen in the growth of customers over a million dollars a year as well as the record number exceeding ten million.

Outlook

The outlook is really the "material" part of the report this time. For the first quarter of fiscal year 2027, Snowflake expects core services revenue of $1.262 billion to $1.267 billion, which equates to roughly 27% growth. For the full fiscal year, the company is targeting $5.66 billion in core services revenue, again roughly 27% growth, and that was above the market consensus cited by Reuters.

What's important about the outlook "between the lines": Snowflake is no longer just talking about revenue growth, but giving a framework for profitability and cash. The company is targeting a 75% core services gross margin after adjustments, as well as a 12.5% operating margin after adjustments for the full year (it expects 9% in Q1). In addition, it gives a target for free cash after adjustments of 23% for the full year. Translated into investor-speak: the growth rate is holding high, but the company wants more of it to gradually translate into "cleaner" operating discipline.

Long-term results

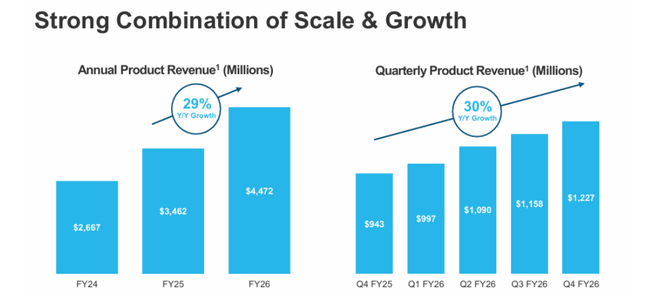

Snowflake has been growing rapidly and relatively regularly for the last four years, which is still exceptional in the enterprise data market. Revenues have risen from $2.07 billion (year ending January 31, 2023) to $2.81 billion (2024), $3.63 billion (2025) and now $4.68 billion (FY 2026). The growth rate may be gradually slowing from the upper thirties towards less than thirty percent, but it is still growth that most large software companies would take with all ten hands. At the same time, gross profit is also growing, showing that the underlying "machine" is working: gross profit has moved from $1.35 billion to $3.15 billion over the same period.

But the long-term picture is more complex at the operational level, and here it's important to be specific. The operating result according to standard accounting is negative over the long term, and even growing in absolute terms: roughly -0.84 billion (2023), -1.09 billion (2024), -1.46 billion (2025) and -1.44 billion (2026). The main reason is simple: operating costs are growing rapidly (around $4.58 billion in 2026) as the company invests in development, sales and support at scale. That's also why it's so crucial for investors to track "after adjustments" metrics and, most importantly, cash at Snowflake. And this is where we see improvement: in fiscal 2026, free cash reached $1.12 billion and $1.19 billion after adjustments, meaning that even with a book loss, the company can generate very decent cash.

The big change of the last year is the "shape of growth": the company is no longer relying only on expansion with existing customers and is accelerating the acquisition of new ones. That's important because 125% retention is great, but that alone won't explain long-term sustainable growth if the inflow of new business slows. Q4 brought 740 net new customers while growing the number of those spending over $1 million per year. That's a combination that usually increases the likelihood that growth will not be a "temporary blip" but rather a more stable trend.

A final important point for the long-term outlook is contracted future consumption. Contracted future sales grew 42% to $9.77 billion, significantly faster than current sales growth. This often means that the company has a very strong business pipeline and that some of the growth has yet to "spill over" into reported numbers in future quarters. If this ratio holds, Snowflake can continue to grow at a high rate in 2027 without having to aggressively worsen pricing.

News

Three areas stand out from the report: rapid expansion of AI capabilities (the company lists over 9,100 accounts using these features), accelerating product development (over 430 new capabilities per year), and strengthening partnerships with major model vendors to give customers choice. It is also adding acquisitions in operational monitoring and systems reliability to expand the use of the platform beyond pure data analytics towards operations and application management.

Shareholding structure

Snowflake is a distinctly "institutional" title. The institution holds roughly 78% of the shares (and over 80% of the free float), with insiders holding around 3.4%. The largest holders are Vanguard and BlackRock (both around 8-9%), followed by Fidelity (FMR) and Jennison.

Analysts' expectations

Reuters mentions that the core services revenue outlook for the year ($5.66 billion) was above the average market expectation and that the outlook for the first quarter was also above consensus. This is usually the main trigger for a positive reaction at a company where investors are most worried about a slowdown in consumption. At the same time, however, the market will continue to keep an eye on two things: whether the 125% retention will hold, and whether operating discipline will continue to improve as indicated by the margin and cash outlook.