Warner Bros. Discovery is showing two businesses moving in opposite directions. Streaming keeps adding subscribers and has now passed 131 million users, which confirms real demand for the digital product. But the older engine is still shrinking. Linear TV is losing viewers and cable subscribers, advertising is weaker, and that pressure shows up in the financials. Q4 revenue fell to $9.5 billion and adjusted EBITDA dropped to $2.2 billion.

The more balanced view is that the company is not falling apart, it is changing shape. Streaming and studios were the stronger parts of 2025, and free cash flow stayed positive at $3.1 billion for the year. Management is also focused on reducing leverage, even though net debt remains high at about $29 billion and leverage is around 3.3x. The investment question is timing: digital growth is real, but it still has to grow enough to offset the decline in traditional TV.

How was the last quarter?

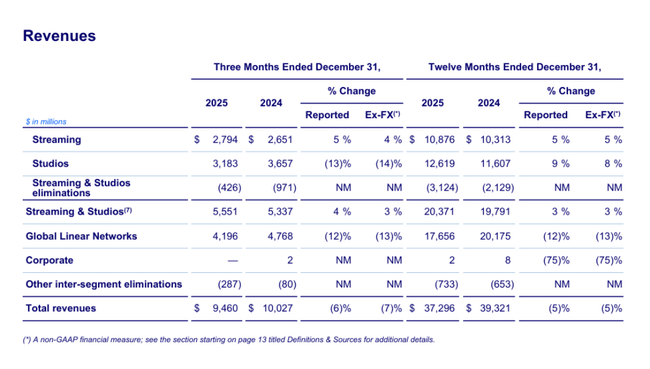

In the fourth quarter, $WBD revenue fell to $9.46 billion (-6% year-over-year), with pressure in virtually every major revenue line outside of streaming. Distribution revenue was down 3%, advertising was down 7% and content sales were down 9%. Executives at advertising openly say that the growth of cheaper ad-supported fare in streaming wasn't enough to offset the decline in viewership on traditional TV, plus the NBA was missing year-over-year, which itself took roughly 4 percentage points off the growth rate.

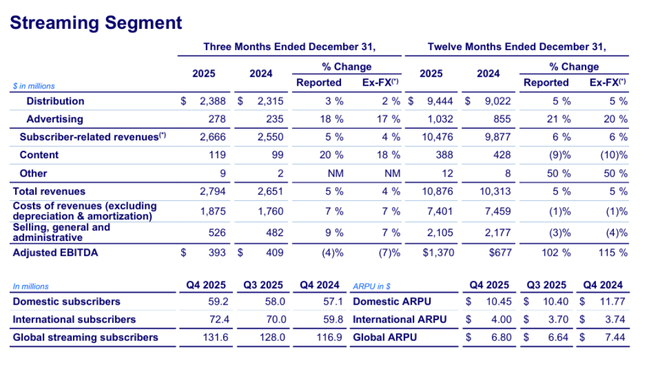

Adjusted operating profit before depreciation and amortization fell to $2.216 billion (-19% year-over-year), and the main culprit was the TV networks, where adjusted operating profit fell 27% to $1.405 billion. While streaming continues to grow in revenue, profitability deteriorated slightly to $393 million in the quarter as the company increased content and marketing costs due to global expansion.

Net loss attributable to shareholders was $252 million. It's important to add that the income statement was heavily weighed down by accounting and restructuring items: the firm reported roughly $1.3 billion in pre-tax amortization of intangible assets, content revaluation and restructuring costs. That's why WBD's cash is the main thing to watch: operating cash was 1.8 billion and free cash was 1.4 billion, although it was down significantly year-over-year.

From an investment perspective, the clearest signal is in subscriber numbers: streaming ended the quarter at 131.6 million, +3.5 million vs. Q3. At the same time, however, average revenue per user declined as the company grows mainly abroad, while the US was hit by a change in its distribution agreement. Translated: volumes are up, but monetization per user is weaker, which is exactly why the market will continue to want to see margins improve in streaming.

Top points of the results

Revenue in the quarter of $9.5 billion, -6% year-over-year.

Adjusted operating profit before depreciation and amortization of $2.2 billion in the quarter, -19% year-over-year.

Free cash in the quarter of $1.4 billion, -43% year-over-year (impaired by approximately $0.6 billion of one-time items).

Streaming: revenue in the quarter of $2.8 billion(+5%), but adjusted operating profit of $393 million (down slightly).

Studios: sales in the quarter of $3.2 billion(-13%), adjusted operating profit of $728 million(-23%).

Television Networks: sales in the quarter of $4.2 billion(-12%) and adjusted operating profit of $1.4 billion(-27%).

Streaming subscribers at quarter-end 131.6 million, +3.5 million quarter-over-quarter.

Average revenue per user globally declined to $6.80 ( -9% y-o-y), mainly due to the decline in the US and growth in cheaper foreign markets.

Full year 2025: revenue 37.3 billion(-5%), free cash 3.1 billion(-30%), net debt 29.0 billion.

Management commentary

In the company's materials, the tone is clear: streaming is to be the growth engine, studios are to bring back creative "reach" and TV networks are to be optimized to generate cash for as long as possible. In the 'shareholder letter', management also emphasises the balance sheet work and confirms that it expects strong operating profit to cash conversion in 2026 too, with only the additional transaction and separation costs still running in the first half of the year and the first quarter tending to be seasonally weakest due to the timing of content payments.

Outlook

In 2026, it expects profit-to-cash conversion to remain strong, while acknowledging additional transaction and separation costs mainly in the first half of the year and noting that the first quarter is typically the weakest for free cash. This is important for investors as cash can "look worse" in the short term without impairing the core business.

Long-term results

Warner Bros. Discovery in recent years is a textbook example of a company where accounting earnings must be separated from real cash. In 2022-2024, results were significantly impacted by the accounting effects of the merger and depreciation in value. In 2024, the company reported $39.3 billion in revenue but ended up with a huge accounting loss of $11.3 billion and a negative operating result. At the same time, however, it reported EBITDA of 22.4 billion, showing how different the same year can look by the metrics.

The year 2025 already looks "cleaner" on a current year basis: sales fell to 37.3 billion (-5% year-on-year), adjusted operating profit before depreciation and amortisation fell just 3% to 8.7 billion, but more importantly it reaffirmed where the pressure is coming from. TV Networks (Global Linear Networks) fell year-on-year in both revenue (-12%) and adjusted operating profit (-21%), while streaming and studios grew. Overall, the streaming segment doubled adjusted operating profit to 1.37 billion for 2025, and studios jumped to 2.55 billion. This is the key trend: the "new" digital business is growing stronger, but the "old" TV business still makes up a big chunk of the results and its decline cannot yet be completely overcome.

At the same time, the cash story is tougher than on paper. Free cash is down 30% to $3.1 billion in 2025, with the firm explicitly saying it was negatively impacted by separation and transaction items of roughly $1.35 billion. That's an important distinction for investors to make: part of the decline is "one-off" but part is structural - TV advertising and a decline in cable subscribers.

And then there's the balance sheet, which puts the whole thesis in context. Net debt of 29 billion and debt of 3.3 times mean that WBD is not a "risk-free" story: the company needs to keep a handle on cash because high debt in the media cycle limits room to maneuver. Management is showing that it is paying down debt and wants to maintain strong cash generation in 2026, but the market will be tight: for this title, the pace of debt decline and streaming's ability to grow profits, not just subscriber growth, will be critical.

News

The biggest "operational" news is the continued growth in streaming: +3.5 million subscribers for the quarter and a move to 131.6 million for the year. But at the same time, the company admits pressure on average revenue per user, especially in the US. Alongside this, the company's materials include an emphasis on boosting studio and network efficiency - i.e. a drive to raise the quality of content while extracting maximum cash from linear TV at a time when its audience is declining.

Shareholding structure

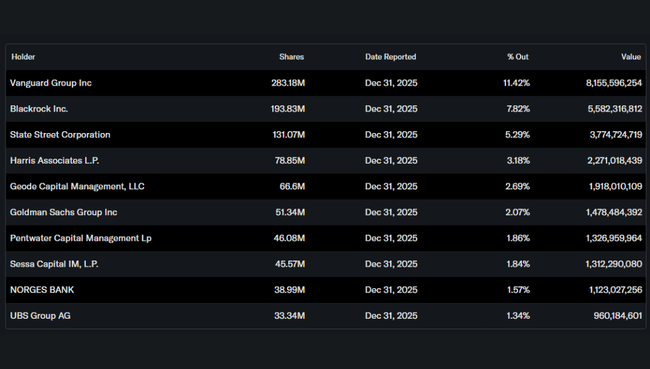

WBD is typically an institutional title: the institution holds around 73.8% of the shares and the insider share is around 4.5%. The largest holdings are Vanguard (about 11.4%), BlackRock (7.8%), State Street (5.3%) and Harris Associates (3.2%). This typically means two things: high liquidity and also that sentiment can change quickly as large funds reassess debt risk and the pace of the shift toward streaming.