In cybersecurity, the cleanest signal is whether customers keep expanding spend, not only renewing contracts. CrowdStrike delivered that type of quarter, with net new recurring revenue hitting a record level. That suggests buying decisions are still active and budgets are not freezing.

Profitability also moved in the right direction. The company reported a positive GAAP net income for the quarter and kept an upbeat tone for FY2026, implying it expects growth to continue rather than fade. For investors, it reads as a business that is scaling and starting to show more “real” earnings.

How was the last quarter?

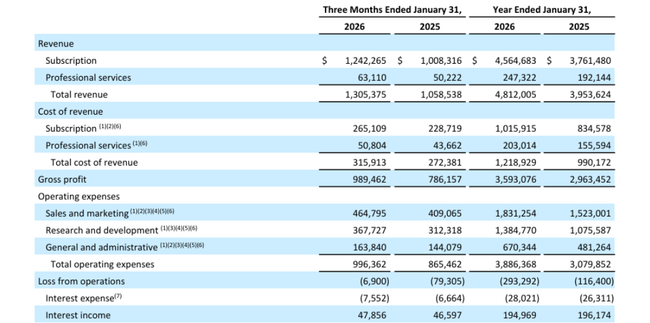

The fourth quarter stands to show that CrowdStrike $CRWD did not slow down, but instead "stepped on the gas" in the metric that best describes the health of the business: in net additions to recurring annual revenue. The company added $331 million, a record, while pushing total recurring annual revenue to 5.25 billion. In practice, this means that CrowdStrike not only retained existing customers, but was able to expand them while adding new contracts at a record pace.

Revenue in the quarter rose to $1.31 billion, with subscriptions accounting for $1.24 billion. Subscription margins remain very high: 79% on an accounting basis and 81% after adjustments. That's important because at that margin, every additional dollar of revenue quickly increases operating profit as long as the company keeps costs under control.

Profitability is visibly shifting. Under accounting rules, operating profit is only slightly negative (loss from operations of $6.9 million), but net income is already positive at $38.7 million. After adjustments, the company generates a very solid operating profit of 325.8 million and a net profit of 289.1 million. This is an important transition for investors: the company remains growth, but at the same time the "quality" of growth through earnings and cash increases.

Cash is almost as important as recurring revenue in this report. Operating cash was $497.9 million and free cash was $376.4 million. There's $5.23 billion of cash on the balance sheet, which gives the company room to continue making acquisitions and buying back stock (the company has already bought back about $50.6 million worth of stock after year-end).

CEO commentary

George Kurtz frames 2026 as the best year in the company's history and backs that up with specific milestones: 5.25 billion in annual recurring revenue and 1.01 billion in full-year net income. Importantly from an investment perspective, management explicitly links continued growth to how companies are adopting artificial intelligence to increase the attack surface and security requirements across the infrastructure.

CFO Burt Podbere goes even further, saying that the combination of accelerating growth, rising profitability and record cash ranks the firm as an outlier in the software market. He also adds a specific "target beacon": a long-term goal of 20 billion in annual recurring revenue by 2036. For an investor, this is important mainly because such a target assumes that the firm believes in a long-term expanding market and its own ability to maintain its leadership position.

Outlook

The Q1 outlook calls for revenue of $1.360 billion to $1.364 billion and recurring annual revenue of roughly $5.502 billion. For the full year 2026, the company expects sales of 5.868 to 5.928 billion and recurring annual sales of 6.466 to 6.516 billion. Reuters notes that the revenue outlook is above market estimates.

Interpretation: the firm is allowing itself to maintain a high growth rate while pushing earnings after adjustments - the earnings per share after adjustments outlook of $4.78 to $4.90 is well above what would be consistent with a "pure growth" firm without discipline. Another important detail is that the firm expects continued strength in the business stack into Q1 2026, suggesting that the acceleration in Q4 was not a one-off.

Long-term results

CrowdStrike shows the classic trajectory of a firm that grows quickly but also hints at how much it invests in expansion. Revenue has moved from $2.24 billion (2023) to $3.06 billion (2024), $3.95 billion (2025) and $4.81 billion (2026) in four years. The rate of growth is gradually slowing from the high thirty percent towards the low twenties, which is natural with a growing base, but it is still an above-average rate within big software.

Gross profit is growing along with sales (3.59 billion in 2025), but the long-term issue is operational efficiency. Under accounting rules, operating profit is still negative and is even worse in 2025 than in 2024, which is related to the cost structure and what is included in the accounting results. That's why investors at CrowdStrike typically look at earnings after adjustments and cash flow first and foremost. This is where the picture is significantly more positive: free cash flow for 2025 was 1.24 billion, higher than the previous year (1.07 billion). In other words: even though the income statement looks "worse" by accounting rules, the company is generating more cash - and that is crucial in this model.

Another long-term trend is "customer expansion". The firm discloses what proportion of customers use six or more modules, seven or more modules, eight or more modules. This is practically a metric that explains why recurring revenue can grow faster than the number of customers: customers are gradually buying more features and moving more parts of security onto the platform.

News

The most significant thing from operations is that the company is pushing to extend the platform into identity and browser (the SGNL and Seraphic Security acquisitions) while expanding sales through partner channels (expanded collaboration with Microsoft through the marketplace). It is adding new regional cloud deployments in the Middle East and Asia. These moves make strategic sense: security is shifting from "endpoint" to identity, browser, data and cloud traffic.

Shareholding structure

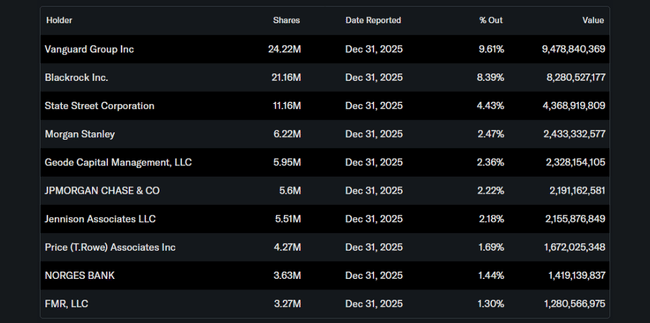

The institution holds around 75.7% of the shares and the insider share is around 3.3%. The largest holders include Vanguard, BlackRock, State Street and Morgan Stanley. In practice, this means high liquidity as well as sensitivity to how large funds read the outlook for recurring revenue growth and cash margin.

Analyst expectations

Post-earnings summaries are showing mostly positive sentiment. Investopedia reports that most analysts have a "buy" recommendation and mentions a consensus target price of around $542 (before the post-earnings updates). TipRanks post-report lists a consensus "slightly positive" and an average target price of around $510, with estimates to be updated after earnings.