Coca‑Cola starts 2026 looking more like a growth compounder than a sleepy staple. Unit case volume is up 3%, reported revenue jumps around 12% to roughly 12.5 billion dollars and organic sales grow about 10%, as an 8% increase in concentrate sales on top of a 2% price/mix lift shows that the company can still add both volume and pricing after several years of strong list‑price moves. The top line lands roughly 300 million dollars above what the Street had pencilled in, extending a pattern in which Coke slightly outgrows its own mid‑single‑digit algorithm while keeping the brand portfolio tight and marketing spend disciplined.

Profitability improves even faster than sales. Operating income rises close to 19%, pushing the operating margin up from about 32.9% to 35.0%, as concentrate economics, moderating input costs and ongoing refranchising benefits add operating leverage on top of revenue growth. Diluted EPS increases about 18% to 0.91 dollars, or 0.86 dollars on a comparable basis, meaning investors are effectively getting high‑single‑digit organic growth and high‑teens earnings growth from a business that still converts roughly 90–95% of its profit into free cash flow and guides to around 12.2 billion dollars of FCF for the full year.

Q1 2026 results

For the first quarter 2026, Coca-Cola $KO reported:

Net sales of $12.5 billion (+12% y/y)

Organic sales +10% (analysts expected approx. +7%)

Global unit case volume +3%, driven by China, US and India

Concentrates sales growth of 8% and price/mix improvement of 2%

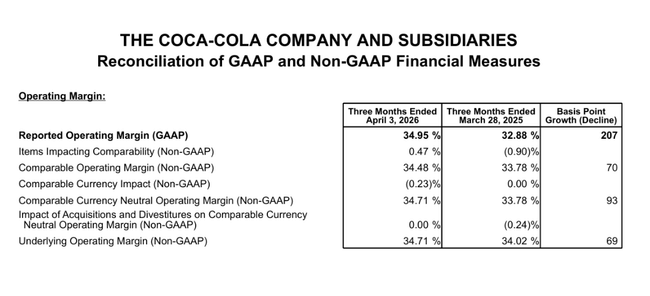

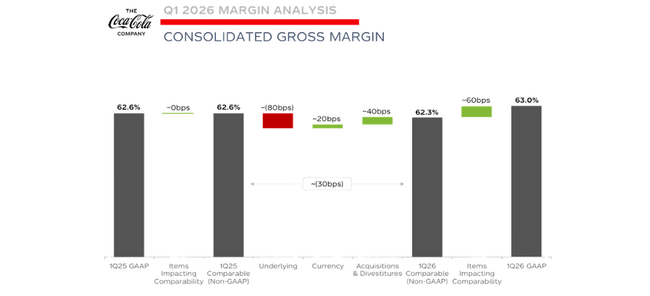

Operating margin improved from 32.9% to 35.0%, comparable (non-GAAP) margin improved from 33.8% to 34.5%. Operating profit growth of 19% is a combination of strong sales, improved cost discipline and favourable exchange rate which added about one percentage point.

Net earnings per share (EPS) rose 18% to $0.91, while comparable EPS was $0.86. In both cases, EPS also benefited from the currency impact, which added about 3-6 percentage points to the growth, but even after filtering out the currency impact, it was still a double-digit increase. This is important: profitability growth is not just based on rates or accounting items, but on real business.

Cash flow from operations in Q1 was US$2.0 billion, free cash flow US$1.8 billion. This is a typical Coca-Cola picture: even with a relatively weaker seasonal quarter, it generates very solid cash, which it uses to fund the dividend, investments and buyouts.

Management commentary

New CEO Henrique Braun describes Q1 as a "strong start to the year", building on three pillars: being close to the consumer, execution at a local level and the ability to manage the complexity of the global portfolio. He stresses that even in an environment where beverage prices are at record levels globally, Coca-Cola can sustain growth in both volume and revenue.

Management talks of "more balanced growth": after a period where much of the growth was driven by price, the company wants to build more on volume and mix - that is, bringing in new consumers, new products and new packaging formats, and only then building value on top of that.

Braun also mentions that Coca-Cola is targeting "culturally significant moments" - Chinese New Year, Ramadan, Carnival in Brazil, March Madness in the US - and connecting them with digital campaigns, AI and personalised marketing. This isn't just pretty marketing speak: the company says directly that it has increased the number of weekly consumers and gained value share globally in NARTD (non-alcoholic ready-to-drink beverages) as a result.

Regions and product mixes

Results by region:

EMEA: sales +13%, organic +11%, volume +2%, price/mix +5%. Profitability grew double digits, with the company gaining share in Germany and Nigeria.

Latin America: sales +14%, organic +9%, volume +1%, price/mix +1%. Higher sales and profitability, supported by strong positions in Brazil and Argentina.

North America: sales +12%, organic +12%, volume +4%, price/mix +1%. Operating profit in the region up 20%, up 17% on a comparable basis, driven by strong execution and cost discipline.

Asia Pacific: sales +6%, organically +5%, volume +5%, price/mix -6%. The region grew in volume, but the company had to work more with price and availability here, so margins are under more pressure.

In terms of categories, Coca-Cola Zero Sugar performed best, growing 13% across all regions in Q1.

Long-term numbers

Revenues have been growing for four years in a row: from roughly $38.7bn in 2021 to $47.1bn in 2024. That's a cumulative growth of around 22%, but the pace has gradually slowed - after a strong 11% in 2022 came around 6% in 2023 and less than 3% in 2024. So the company is still growing, it's just not accelerating anymore, rather it's riding in the stable, low single-digit range that's pretty typical for a mature global brand.

Gross profit is growing faster than revenue itself: from roughly $23.3 billion to $28.7 billion. This means that gross margins are gradually improving - Coca-Cola is able to increase price, shift the mix towards higher margin products, while keeping direct costs under control. Simply put: for every dollar of sales, it's making a little more in gross profit than it did a few years ago.

Operating profit, however, is a slightly different story. It stays in the $10-11.3 billion range from 2021, but drops from $11.3 billion to $10.0 billion in 2024. Yet gross profit continues to grow. This means that the problem is not "at the top" (prices, volumes) but "in between" - in operating costs.

On a net level, the picture is surprisingly calm. Net profit is around USD 9.5-10.7 billion, without much fluctuation. EPS lies roughly between $2.2 and $2.5. We see one stronger year (2023) where EPS jumps due to a combination of higher earnings and slightly lower share count, and 2024 where EPS falls slightly despite still very decent absolute numbers.

Outlook for 2026

Coca-Cola updated the outlook only slightly after Q1, but basically confirmed it:

Organic sales growth continues to be expected in the 4-5% range.

Comparable earnings per share are expected to grow 8-9% this year from last year's $3.00.

Currencies should add about 3% to EPS growth, while acquisitions and divestitures should take about 1% off.

The company expects free cash flow of about $12.2 billion ($14.4 billion from operations minus $2.2 billion CAPEX).

New to the outlook is a more detailed description of the impact of the pending sale of Coca-Cola Beverages Africa (CCBA), which is expected to close in the second half of 2026. This will reduce revenue in the short term (about 4% headwind to comparable sales) but should improve capital efficiency and slightly boost margins.

Shareholders

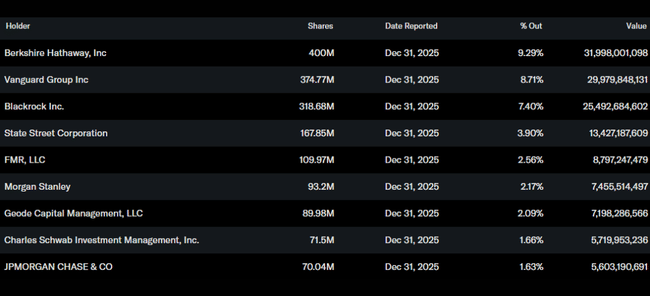

Coca-Cola is one of the most classic "institutional" titles, but with a significant anchor in the form of Berkshire Hathaway. According to data from Yahoo Finance:

Insider the stake is about 9.9% of the stock.

The institution holds about 66.6% of the stock and about 73.9% of the free float.

The stock is held by more than 4,400 institutions.

Largest shareholders:

Berkshire Hathaway: about 400 million shares, about 9.3% of the company.

Vanguard: about 375 million shares, about 8.7% of the company.

BlackRock: about 319 million shares, about 7.4%.

State Street: about 168 million shares, just under 4%.