The first quarter of 2026 confirmed that SoFi is moving beyond being "just" an online lender and is gradually transforming into a universal digital financial platform. The company delivered record net sales, a record number of new members and products, while posting its tenth consecutive quarter of GAAP earnings. The growth engine is built on a combination of the lending business, fast-growing financial services (accounts, investments, cards) and the technology platform, although the latter is going through a temporary weaker phase this quarter due to the exit of a large client.

In terms of strategy, SoFi continues to push the breadth of the ecosystem: it is entering the digital asset space through its own stablecoin SoFiUSD, rolling out "Big Business Banking" for corporate clients, and innovating end-user products - from investments and cryptos to savings accounts to simplified AI-powered personal loan and home loan applications. This breadth of offerings reinforces the Financial Services Productivity Loop: a customer comes in for one product, but uses multiple services over time, reducing acquisition costs and increasing lifetime customer value.

Q1 2026 results: revenue, profit and profitability growth

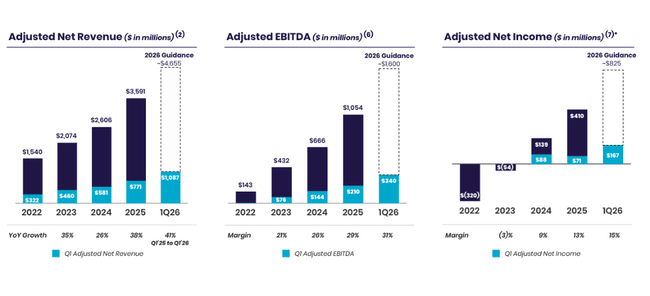

For the quarter ended March 31, 2026, SoFi $SOFI achieved record GAAP net sales of $1.10 billion, up 43% from $771.8 million a year ago. Adjusted net revenue, which excludes certain one-time items, was $1.09 billion, up 41% year-over-year from $770.7 million. This continues the company's high growth rate of previous years, but combined with increasing profitability.

Adjusted EBITDA increased 62% to a record $340 million, up from $210 million a year ago. This brings the EBITDA margin to approximately 31%, a very solid level for a fast-growing fintech. At the same time, SoFi reported its 18th consecutive quarter of beating the so-called Rule of 40 with a score of 72% - the sum of revenue growth rate and EBITDA margin, showing a combination of high growth and already decent profitability.

At the GAAP net income level, the company reported $166.7 million, with earnings per common share (diluted EPS) of $0.12 versus $0.06 a year ago - a 100% increase. Adjusted net income and diluted EPS are essentially flat as there were no significant one-time charges in the quarter that significantly distorted GAAP earnings.

Another important source of improvement is the strong growth in net interest income, which reached $693 million in the first quarter, up 39% year-over-year. This was driven by both a 41% increase in average interest-earning assets and a 48bps decline in the cost of funds, even though the return on assets fell 63bps, so SoFi is benefiting more from being able to finance more cheaply. Net interest margin (NIM) rose to 5.94%, up 22bps from the previous quarter.

SoFi's share price is down after the results mainly because even though the company showed record revenue, profit and member growth, the market was expecting more in the way of outlook - management didn't raise full-year guidance after such a strong quarter, leaving investors feeling that the Q1 momentum may not last for the rest of the year. The stock had been rising strongly ahead of the results, so it went into them with high expectations, and the reaction is typical "sell the news": the numbers are great, but they weren't enough beyond what was already priced in.

Growth in members, products and loans

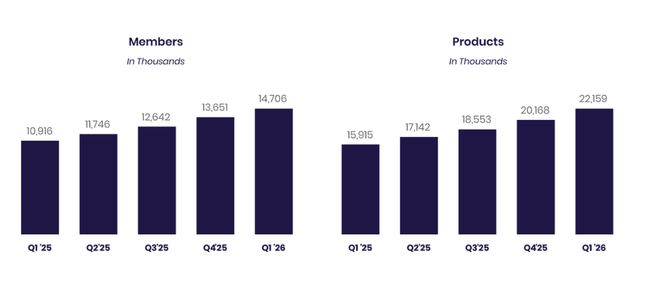

SoFi continues to rapidly ramp up its client base. A record 1.055 million new members were added in the first quarter, bringing the total to 14.7 million, up 35% from 10.9 million a year ago - and the third straight quarter of 35% membership growth. The number of products grew even faster: the company added 1.8 million new products, bringing the total to 22.2 million, up 39% year-on-year. Another interesting sign of the strength of the ecosystem is that 43% of new products came from existing members, expanding the relationship with the customer.

The credit business experienced a record quarter in terms of origination volume. Total new loans reached $12.2 billion, up $1.7 billion from the previous quarter. Personal loans were the driving force with a record $8.3 billion in new loans, followed by student loans with a record $2.6 billion (2.2 times more than last year) and mortgage loans with $1.2 billion, approximately 2.4 times more than a year ago. Loan Platform Business - that is, third-party lending and referral business - grew 90% year-over-year and added $3.6 billion in commitments with three new partners during the quarter.

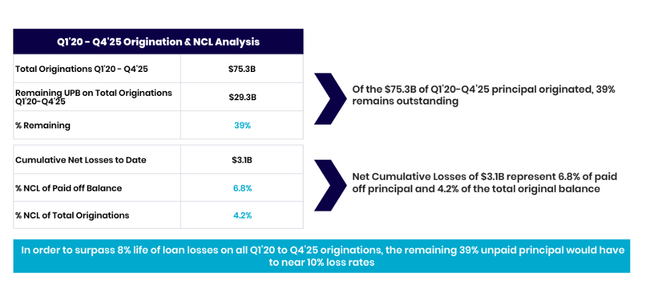

Credit quality remains strong and in line with expectations across all loan types, according to management. There was even improvement in personal loans, with annualized net charge-offs down 28bps year-over-year, which looks positive in an environment of higher rates and tight consumer credit. This suggests that scoring, targeting more creditworthy clients and risk management are working and SoFi is not chasing growth at any cost.

Segments: financial services, technology and margins

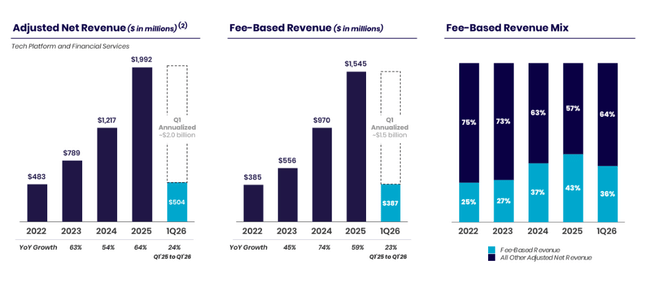

Financial services (accounts, investments, cards, deposits) are becoming an increasingly important leg of the business. The Financial Services segment reported revenue of $428.5 million in Q1 2026, up 41% from a year ago. Non-interest income (fees, commissions) rose 55% to $200.8 million, while net interest income here rose 31% to $227.7 million, driven mainly by growth in customer deposits. Segment contribution profit was $195.6 million, up $47.3 million from last year, and segment margin was 46%, though down slightly from 49% year-over-year as the firm invests more in growth.

Meanwhile, Financial Products is growing very fast: the number of Financial Services products grew to 19.3 million, +40% y/y. SoFi Money reached 7.3 million products, Relay also reached 7.3 million and SoFi Invest reached 3.7 million products. Total deposits increased $2.7 billion to $40.2 billion in the quarter, primarily driven by retail deposits. This is key to funding the loan portfolio, as the average rate on deposits is 155bps lower than the cost of funding through warehouse lines, which the company says translates into annual interest cost savings of around $622 million.

The technology platform(Galileo and others) had a weaker quarter. Technology Platform segment revenue fell 27% year-over-year to $75.1 million, primarily due to one large client completing its exit from the platform at the end of 2025. Segment contribution fell to $12.0 million and margin fell to 16% from 30% a year ago. The number of "enabled accounts" on the technology platform declined 16% year-over-year to 133 million, however, 4 million accounts were added quarter-over-quarter, suggesting that the large client exit is primarily a one-time shock and the market as a whole continues to grow.

Innovation, digital assets and brand

CEO Anthony Noto stresses that continuous product innovation is behind the numbers. In the first quarter, the firm started to benefit from SoFiUSD, its US dollar-backed stablecoin, while developing settlement capabilities and interoperability between digital assets and fiat currencies via partners such as Mastercard, which should enable SoFiUSD to be used across global payment networks. It has also launched Big Business Banking - an extension of the platform to enterprise clients, further diversifying revenue from the technology and infrastructure side of the business.

On the retail side, SoFi relaunched cryptocurrency investing (SoFi Crypto) and in April relaunched SoFi Plus with enhanced benefits - such as a 4.5% annual interest rate on deposits up to $20,000 and a 1% match on investment and crypto purchases. In lending, it deployed an AI-built Personal Loan Doc Coach tool to streamline the application process and launched a fully digital home equity line of credit (HELOC) process.

Meanwhile, the brand is clearly going from strength to strength: spontaneous awareness (unaided awareness) has reached an all-time high of 10%. In the J.D. Power 2026 rankings for investor satisfaction in the DIY investing category, SoFi came in first place and was also named the "#1 U.S. Bank" in the World's Best Banks by Forbes. This supports the narrative that SoFi is moving from a "start-up" to an established financial brand with growing public trust.

Capital and Outlook

During the quarter, shareholders' equity increased by $322 million to $10.8 billion, bringing book value per share to $8.44. Even more interesting for shareholders is the development of tangible book value: it increased by $336 million to $9.2 billion and tangible book value per share rose to $7.21 from $4.58 a year ago, up 57% y/y. Thus, the growth in profitability translates in real terms into a strengthening of the capital base.

CEO Anthony Noto in a commentary highlights that growth is "resilient and returns strong" thanks to innovation and brand building. He says entering new areas such as digital assets, along with strong growth in existing businesses, strengthens and diversifies the platform so that SoFi can reinvest in better products and experiences for members and corporate clients over the long term. The firm is also leaning on a combination of strong revenue growth, increasing profitability (on both a GAAP and non-GAAP basis) and an improving capital position, an unusual and attractive combination for investors in this segment.

Key numbers

Net revenue (GAAP) $1.10 billion, +43% y/y; adjusted net revenue $1.09 billion, +41% y/y.

Adjusted EBITDA $340mn. USD, +62% y/y; margin approx. 31%.

GAAP net profit 166.7 mln. USD 0.12 vs. USD 0.06 a year ago (+100%).

Total new loans USD 12.2bn: personal loans USD 8.3bn, student loans USD 2.6bn (2.2x y/y), mortgage loans USD 1.2bn (2.4x y/y).

Membership 14.7m, +35% y/y; total products 22.2m, +39% y/y, of which Financial Services products 19.3m, +40% y/y.

Total deposits $40.2bn (+2.7bn q/q), NIM 5.94%, +22bps q/q.

Technology Platform sales of 75.1 mil. USD (-27% y/y), margin 16%, enabled accounts 133mn (-16% y/y, +4mn q/q).