Qualcomm has had a quarter that doesn't look bad at first glance, but is more about stability than growth. Sales, while over $10.6 billion, are down slightly year-over-year and core profitability (non-GAAP) is weaker than last year. Meanwhile, the company continues to massively return capital to shareholders, is ramping up business in automotive and IoT, and is preparing to enter the data center space, so the story is very much about transformation from a pure "mobile" player to a broader AI/Edge/Data Center platform.

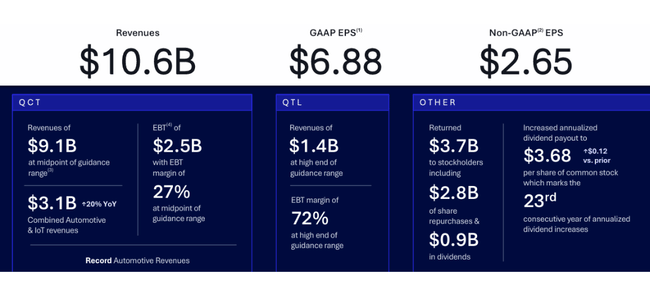

The other side of the coin is that headline GAAP EPS of $6.88 is driven by a one-time tax benefit of over $5 billion - without it, earnings per share are around $2.65, down a bit year-over-year. Qualcomm delivered results "in line with expectations" but not above, and the outlook for the next quarter counts on pressure from memory supply constraints and weaker Chinese handset shipments.

Qualcomm's share price shot up about 12% after the results because the market was expecting a much worse scenario - results were "only" slightly weaker year-over-year but in line with expectations, key automotive and IoT segments are growing at double-digit rates, management clearly outlined new growth engines in AI and data centers, and added a strong signal to shareholders in the form of a new buyback program.

Q2 FY 2026 results: stable revenue, weaker core earnings

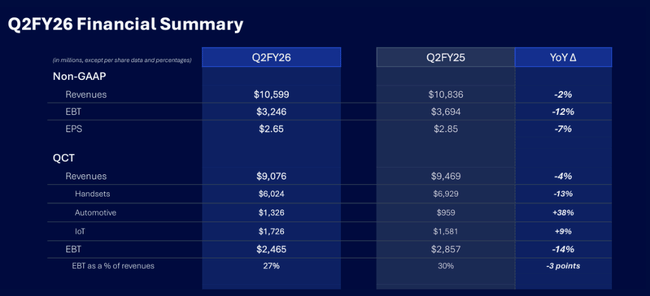

Qualcomm's fiscal second quarter 2026 $QCOM revenue was $10.6 billion, down 3% on a GAAP basis, or 2% on a non-GAAP basis, from $11.0 billion in the prior year. In terms of expectations, management says the results were "in line," meaning no significant positive or negative surprises.

GAAP earnings before taxes (EBT) fell to $2.2 billion (-28%) from $3.1 billion, but GAAP net income jumped to $7.37 billion from $2.81 billion, or +162% y/y. The reason is not the boom in business, but the $5.7 billion one-time tax benefit from the release of a valuation allowance on deferred tax assets, as the company expects to actually use these assets following the new interpretation of the minimum tax rules. This inflated GAAP EPS to $6.88 (+173% y/y), but this effect is explicitly excluded from the non-GAAP numbers.

On an adjusted (non-GAAP) basis, which better reflects current operations, the dynamics look more sobering: non-GAAP EBIT fell 12% from $3.69 billion to $3.25 billion and non-GAAP net income fell 10% from $3.17 billion to $2.84 billion. Adjusted earnings per share declined 7% from $2.85 to $2.65. Margins are under pressure - a combination of weaker handset and higher R&D and sales overhead costs as we transform toward AI and data centers.

Segments: weakening handsets, record automotive, solid QTL

At Qualcomm's core is the QCT (chips and platforms) segment, where second-quarter revenue was $9.08 billion, down 4% year-over-year (from $9.47 billion). QCT's pre-tax profit fell 14% from $2.86 billion to $2.47 billion, and EBT's margin declined from 30% to 27%. This was mainly due to a weaker handset business and a costlier environment (development, go-to-market) in new areas.

Detail by QCT sub-segments:

Handsets: sales of $6.02 billion, down 13% from $6.93 billion.

Automotive: sales of $1.33 billion, up 38% from $959 million - an all-time record quarter.

IoT: sales of $1.73 billion, up 9% from $1.58 billion.

Thus, the handset part is still dominant but weakening and the volatility of the smartphone market is showing, while automotive and IoT are generating more stable, structural growth. The combination of automotive + IoT revenues yields 20% year-on-year growth, which management explicitly highlights as evidence of diversification beyond mobile.

The QTL (patents) licensing segment had a good quarter. QTL revenue rose to $1.38 billion from $1.32 billion, up 5%, and EBT was up 7% to $994 million. QTL's EBT margin improved to 72% from 70%, so the licensing business remains very profitable and helps stabilize the company's overall profitability even with the fluctuations in the chip business.

Cash flow, balance sheet and capital allocation

Cash flow from operations for the first half of fiscal 2026 was $7.4 billion, slightly above the $7.1 billion in the same period of 2025, although net income (excluding the tax effect) was not significantly higher. Inventory rose from $6.53 billion to $7.37 billion, which may be related to preparing for new products (AI, datacenters, automotive), but it also ties up some capital.

As of March 29, 2026, Qualcomm had $5.44 billion in cash and equivalents and another $4.36 billion in marketable securities, or roughly $9.8 billion in liquid assets. Long-term debt is $14.77 billion and short-term debt is $498 million, for a total of about $15.3 billion in debt, while equity is $27.3 billion. The balance sheet remains solid, although the company returns a significant portion of cash flow to shareholders.

In the first half of fiscal 2026, Qualcomm completed $5.44 billion in share repurchases while paying out $1.90 billion in dividends. In the second quarter alone, $3.7 billion was returned to shareholders - $945 million in dividends ($0.89 per share) and $2.8 billion in repurchases of 19 million shares. In addition, the board of directors approved a new buyback program of up to $20 billion, showing confidence in its own long-term story and a willingness to aggressively reduce the number of shares outstanding.

Outlook: pressure in mobile, AI and datacenters as the new engine

In the commentary, management openly admits that the company is going through a "period of profound transformation" where the emergence of AI agents is changing the product roadmap across platforms. At the same time, Qualcomm is entering the data center space - a custom silicon project for a leading hyperscaler is mentioned, with first shipments expected as early as the end of this calendar year. A more detailed presentation of opportunities in datacenters and so-called Physical AI is to come at Investor Day on June 24.

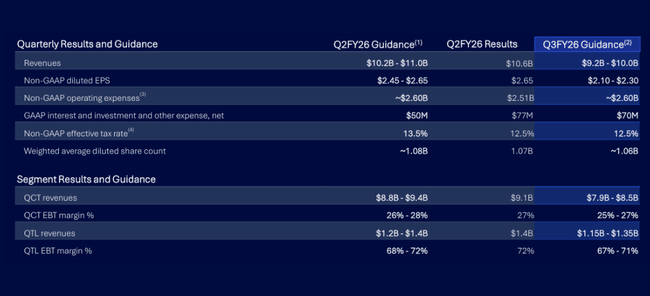

In the short term, however, the numbers will be affected by the problem in the handset segments. In the current outlook for Q3 2026, management is anticipating the impact of limited memory supply and related pricing on demand from several handset manufacturers. It expects total sales in the range of $9.2-10.0 billion, QCT sales between $7.9-8.5 billion and QTL between $1.15-1.35 billion. Non-GAAP EPS is expected to be in the range of $2.10-2.30 per share.

Important detail: Qualcomm says QCT handset revenue in China should bottom out in Q3 and return to sequential quarter-on-quarter growth in the following quarter. That's a key signal - they're actually saying that the current pressure is cyclical and should be transitory, but will still hurt in the short term.

Key numbers

Revenue of $10.6 billion (-3% y/y GAAP; -2% y/y non-GAAP).

GAAP EPS of $6.88 (+173% y/y) mainly due to a one-time tax benefit of $5.7 billion; non-GAAP EPS of $2.65 (-7% y/y).

QCT revenue USD 9.08bn (-4% y/y), of which handsets USD 6.02bn (-13%), automotive USD 1.33bn (+38%, all-time high), IoT USD 1.73bn (+9%).

QTL revenue USD 1.38bn (+5% y/y), EBT margin 72% (vs. 70% last year).

Operating cash flow for H1 FY 2026 USD 7.41bn, cash + securities approx USD 9.8bn, long-term debt USD 14.8bn.

Return of capital to shareholders in 1H FY 2026: buybacks USD 5.4bn, dividends USD 1.9bn; new buyback program up to USD 20bn.

Q3 FY 2026 outlook: revenue USD 9.2-10.0bn, non-GAAP EPS USD 2.10-2.30, QCT handset sales in China expected to bottom and grow again from Q4.