Meta has had an exceptionally strong quarter in terms of business growth - revenues jumped by a third, advertising is growing in both volume and price, and GAAP earnings look fantastic on paper. But at the same time, one-time tax effects are significantly impacting results, and the company is dramatically increasing planned capital spending on AI infrastructure, raising nervousness around future margins and free cash flow.

The result is a paradox: the fundamental metrics look great, but the investment and cost commentary is so aggressive that the stock falls roughly 7% after the results.

Q1 2026 results: strong revenue growth and tax effects

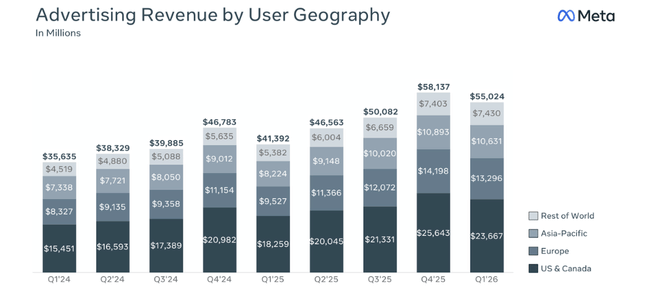

Meta Platforms $META revenue came in at $56.31 billion in Q1 2026, up 33% year-over-year from $42.31 billion in Q1 2025. Adjusted for currency effects, revenue would have grown roughly 29%, so growth is not just about rates, it's about real business. In terms of platform metrics, the firm reports 3.56 billion daily active people across the app family (Facebook, Instagram, WhatsApp, Messenger), +4% y/y, though there was a slight decline quarter-on-quarter due to internet outages in Iran and WhatsApp restrictions in Russia.

In terms of advertising, it was a very strong quarter: the number of ad impressions increased by 19% y/y and the average price per ad increased by 12% y/y. In other words, Meta is selling significantly more ads while collecting a higher price for them, which is one of the main reasons for the sharp revenue growth.

But operating costs are rising even faster than revenues. Total costs and expenses rose 35% to $33.44 billion (from $24.76 billion). This is mainly driven by investments in infrastructure (data centers, AI chips, servers) and higher personnel costs, which are reflected in higher revenue and R&D expense items. Still, operating profit increased to $22.87 billion from $17.56 billion, and margins remained at a very high 41% (same as last year), so the company has been able to "roll over" the higher costs with revenue growth and scale so far.

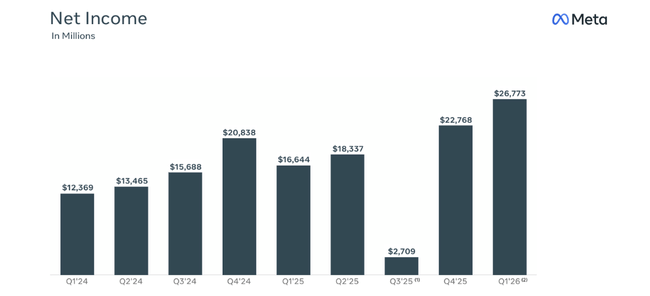

GAAP net income jumped to $26.77 billion, up 61% from $16.64 billion a year ago, diluted EPS came in at $10.44 vs. $6.43 in Q1 2025, +62% y/y. But here's an important detail: the numbers are significantly inflated by the tax effect.

The tax benefit: an unrealized bonus that distorts EPS

In the quarter, Meta reported an $8.03 billion tax benefit associated with last year's tax reform (the "One Big Beautiful Bill Act") and the subsequent clarification by the Treasury Department (Notice 2026-7) that retroactively adjusts the treatment of previously capitalized R&D costs. This benefit partially offsets the huge non-cash tax expense of $15.93 billion that Meta booked in the third quarter of 2025 upon implementation of the new legislation.

The effective tax rate in Q1 2026 is -23% due to this effect, negative because the company booked a net tax benefit instead of an expense. Meta itself reports that if not for this one-time tax benefit, the effective tax rate would be 37 percentage points higher and EPS would be $3.13 lower. This means that "normalized" EPS would have been somewhere around $7.3, not $10.44.

Therefore, an investor looking at profitability going forward would logically not view this tax boost as repeatable. Thus, from a core business perspective, operating profit growth and free cash flow are more important than headline GAAP net income.

Cash flow, capex and balance sheet

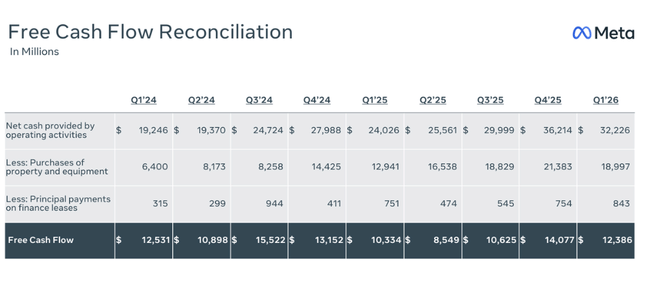

Meta generates very strong operating cash flow: it reached $32.23 billion in Q1 2026, up from $24.03 billion a year ago. Free cash flow (after accounting for investments in assets including lease payments) was $12.39 billion. Thus, even with sharp capex growth, the company remains strongly cash-flow positive.

Capex including lease payments was $19.84 billion in the quarter - significantly higher than the $12.94 billion in the same period in 2025. This is related to a giant wave of investment in AI infrastructure - data centers, custom chips, accelerators, networking equipment. CFO Susan Li says the higher capex this year is due to both higher component prices and additional data center costs to create capacity for future years.

On the balance sheet, this is reflected in asset growth: net tangible assets (property & equipment) rose from $176.4 billion to $194.8 billion in three months. At the same time, Meta holds $81.2 billion in cash and marketable securities, so even with massive investments, it has very strong liquidity. Long-term debt is $58.75 billion, so the net cash position is still significantly positive.

The company paid out $1.35 billion in dividends and equivalents in the quarter and did not make any additional share buybacks (unlike in 2025 when buybacks were massive). In the context of such a giant capex, this may suggest that the number one priority now is investing in AI, not maximizing cash returns to shareholders.

Management commentary and news

Mark Zuckerberg described the quarter as a "milestone" - the company sees strong growth across apps and also unveiled the first model from Meta Superintelligence Labs. The goal, he said, is to deliver "personal superintelligence" to billions of people, clearly framing AI as the company's main strategic direction.

In specific news:

AI and Meta Superintelligence Labs: Meta says the first model from this new AI unit was launched this quarter and is set to be the cornerstone of a new generation of AI assistants and content creation within the app family.

Advertising and monetization: management highlights that revenue growth is being driven by a combination of higher engagement (more time in apps), higher impressions, and improving ad effectiveness through AI (better targeting, creative, campaign optimization).

Infrastructure and capex: CFO Susan Li and team are clear that they are raising the full-year capex outlook for 2026 to $125-145 billion, from the original $115-135 billion, and that this reflects higher component prices and additional data center capacity in the coming years. This is substantially above the 2025 level of $72.2 billion and roughly double the sum of the 2024 and 2025 capex combined.

This sends a clear signal to management: Meta will not skimp on AI infrastructure - it's going in hard, even at the cost of short-term margin and cash flow pressure.

Why the share price is down ~7% after the results

Meta stock is down roughly 7% after earnings, even though the quarter looks great on paper, precisely because of how the market is reading the quality of earnings and investment outlook.

Some of the gain is one-time: investors can well see that a big chunk of EPS is driven by a one-time tax benefit of $8.03 billion - "real" EPS would have been $3.13 lower. Thus, some of the positivity will not carry forward.

Capex explodes: Meta raises this year's capex to $125-145 billion, $10 billion higher than previous estimates, and well above 2025 levels. This means lower free cash flow in the coming years and pressure on margins due to rising depreciation.

Costs are rising fast: total costs +35% y/y, management openly says much of this is structural - infrastructure costs, AI talent, data centers.

So the market is not just looking at the fact that Q1 delivered 33% revenue growth and high operating margin, but more importantly that Meta is willing to invest hundreds of billions of dollars in AI over a couple of years, which can significantly depress earnings per share and free cash flow in the interim. Hence the negative reaction to the results: investors are questioning whether the pace of AI growth and monetisation will be fast enough to justify such massive investment.

Meta's outlook for 2026

Meta confirmed and expanded several key outlook items in its Q1 2026 results:

Total 2026 Costs and Expenses - The firm expects total annual costs and expenses in 2026 to be in the range of $162-169 billion, unchanged from the previous outlook in Q4 2025. Meta also says that even at this level of costs, it still expects operating profit in 2026 to be higher than in 2025.

Capex (AI and Infrastructure) 2026 - Highlights: Meta raised its 2026 capex estimate, including leases, to $125-145 billion, up from the previous range of $115-135 billion. CFO Susan Li explains the $10 billion increase by higher component prices and - to a lesser extent - additional data center costs for capacity in future years.

Cost Growth Structure - Meta notes that most of the cost growth in 2026 will come from infrastructure - i.e., third parties in the cloud, operating costs for its own infrastructure, and hiring and rewarding AI professionals.

Revenues (implied) - For Q1 2026, Meta previously guided revenues in the $53.5-56.5 billion range and ended up with $56.31 billion, the top end of the range. There is no explicit new revenue band in the release for the rest of the year, but the company declares that at costs of 162-169 billion, it still expects operating profit to be higher than in 2025, implicitly assuming further growth in revenue and margins, although they will be pressured by higher capex and depreciation.