Berkshire’s quarterly headlines can be misleading because net income moves with stock prices in its investment portfolio. A better way to judge the business is operating profit, which reflects what the group’s companies actually earned in insurance, rail, energy, and industrial operations. In Q4 2025 that measure was weaker, with after-tax operating profit falling to $10.2 billion from $14.5 billion a year earlier.

At the same time, Berkshire enters 2026 with unusual financial strength. Reports pointed to cash near $373 billion at year-end. The company still is not buying back its own shares and remains careful with new investments. For investors, the message is straightforward: results can move up and down, but the balance sheet gives Berkshire the ability to wait and act when better opportunities appear.

How was the last quarter?

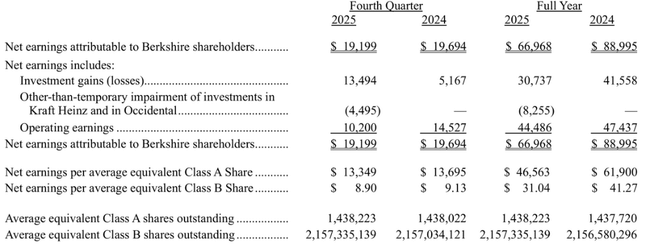

Berkshire $BRK-B reported net income of $19.199 billion in Q4 2025, but this number is misleading for Berkshire because it includes a large component of investment gains and losses. The firm says it outright in the press release: investment results in individual quarters "typically say nothing" about the performance of the business and can be confusing to less experienced investors. In Q4 2025, after-tax investment gains were $13.494 billion, but at the same time, write-downs on investments in Kraft Heinz and Occidental ($4.495 billion) squeaked into the results.

Therefore, it makes more sense to stick with operating profit, i.e. the result "excluding the impact of investment revaluation" and selected one-off items. Q4 operating profit fell to $10.200 billion from $14.527 billion a year earlier. The biggest negative contribution came from the insurance industry: insurance underwriting fell to 1.561 billion from 3.409 billion and insurance investment income fell to 3.072 billion from 4.088 billion.

Outside of insurance, the picture was mixed but less dramatic. BNSF railroads lifted operating profit to 1.347 billion (from 1.278 billion), energy (Berkshire Hathaway Energy) was slightly lower at 691 million (from 729 million) and industrials, services and retail rose to 3.370 billion (from 3.262 billion). In other words: "real businesses" held up, but insurance companies didn't generate as strong a surplus this time as last year, and that dragged the entire quarter down.

Top points of the results (quarter + full year)

Q4 after-tax operating profit: $10.2 billion (up from $14.5 billion).

Net income attributable to shareholders in Q4: $19.2 billion (virtually unchanged).

Q4 includes, among other things, a $4.5 billion after-tax write-down of the value of investments in Kraft Heinz and Occidental combined.

Full-year 2025 operating profit: $44.5 billion (down from 2024).

Full-year net income 2025: $67.0 billion (down from 2024).

Insurance "float" at the end of 2025: about $176 billion (+$5 billion year-over-year).

Management commentary

"The amount of investment gains (losses) in a given quarter is typically meaningless and provides earnings per share data that can be very misleading to investors who have little or no knowledge of accounting rules."

From the letter to shareholders: Management positions Warren Buffett as a key pillar of Berkshire's entire investment identity. It recalls that his "engine" was not just stock selection, but building the insurance business and working with the so-called insurance "float," the capital Berkshire holds through insurance and can invest over the long term. At the same time, the text works with comparisons to baseball legend Ted Williams to emphasize the style of decision-making: patience, picking the right opportunities, and then making a decisive move when the "right pitch" comes along.

Long-term results

At Berkshire, the long-term view is always about what is "corporate performance" and what is "accounting noise" from the stock portfolio. That's why the company itself tries to pitch operating earnings, not net income, to investors. In the 2025 numbers, the difference is starkly visible: full-year net income of $66.968 billion carries investment gains of $30.737 billion, but also write-downs on selected investments of $8.255 billion. The operating profit of 44.486 billion thus comes out as a more "realistic" picture of how the core group fared.

The structure of operating profit for the full year 2025 shows where Berkshire is earning steadily: insurance investment income 12.513 billion, insurance underwriting 7.258 billion, BNSF 5.476 billion, energy 3.979 billion and industrial/services/retail 13.647 billion. If an investor wants to understand Berkshire, this is the "engine map" that is more important than quarterly swings in net income.

The other long-term axis is capital discipline. The public summaries show that Berkshire continues to do no buybacks of its own stock despite its huge cash hoard and remains a net seller of stocks in the portfolio, consistent with a "don't buy at any price" philosophy. This is a factor that may hinder short-term performance against the market, but over the long term it is a mechanism that protects against overshooting in an expensive market.

Shareholding structure

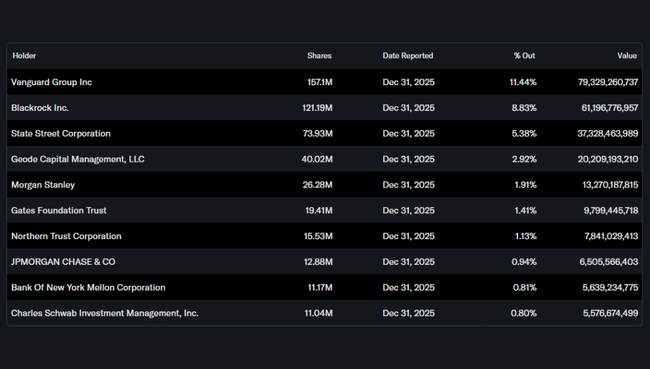

Berkshire is a distinctly institutional title: the institution holds roughly 67% of the stock and the largest holders are Vanguard, BlackRock, State Street and Geode. For the average investor, the conclusion is simple: this is a highly liquid and "fund-owned" stock where sentiment is driven more by the market's view of value, interest rates and investing discipline than by short-term news.

Analysts' expectations

Berkshire's analyst coverage tends to be surprisingly limited and target prices vary across sources. For example, Investing.com lists a consensus "buy" with an average target price of about $526 for the Class B stock, while MarketWatch mentions an average target price of about $533 and an average recommendation of "hold." It's fair to read this to mean that Berkshire's analytical models differ mainly in their work with portfolio value, insurance revenue expectations, and how the market values the giant cash.