ASML entered 2026 with a quarter that at first glance looks slightly weaker than the end of 2025, but under the surface shows very strong momentum. Revenues fell quarter-on-quarter from roughly €9.7 billion ($10.6 billion) to €8.8 billion ($9.6 billion), but gross margins rose to 53%, while the company also raised its full-year guidance significantly.

Net profit in the first quarter came in at €2.8 billion (about $3.0 billion), and ASML now expects to make €36-40 billion ($39-43 billion) for the full year on a gross margin of 51-53%. Combined with a rising dividend and share buybacks, that says one thing: demand for lithography for AI and advanced chips is so strong that the company can afford to plan for further growth after a record year.

How did Q1 2026 turn out?

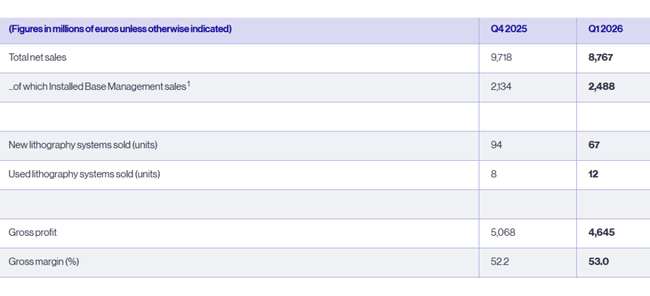

In the first quarter, $ASML generated €8.8 billion (roughly $9.6 billion) in total revenue, down from €9.7 billion ($10.6 billion) in Q4 2025, but comfortably within the previously stated outlook. Year-on-year comparisons don't matter so much to management in the materials, as 2025 was already very strong; more important is the trajectory: Q1 is a bit weaker than the extremely strong Q4, but the outlook for the rest of the year is rising.

Installed Base Management - i.e. servicing and upgrades of installed machines - is still a bigger part of the revenue. This item reached €2.5 billion ($2.7 billion) in Q1, versus €2.1 billion ($2.3 billion) in Q4 2025. This is key for the investor as it is recurring, more stable, high-margin revenue that helps smooth out the new machine delivery cycle.

The company delivered 67 new lithography systems, down from 94 in Q4, but also 12 used machines (vs. 8 in Q4). The mix of deliveries and a strong service business meant gross profit reached €4.6 billion (about $5.0 billion) and gross margin jumped to 53% from 52.2% in Q4. This is an extremely high number for a capital intensive business and confirmation that ASML has exceptional pricing in the delivery of the most advanced lithography.

Net profit was €2.76 billion (about $3.0 billion), only slightly below the €2.84 billion ($3.1 billion) in Q4. Earnings per share were 7.15 euros ($7.8) basic EPS versus 7.35 euros ($8.0) a quarter earlier. Given the seasonality of orders and the fact that Q4 2025 was exceptionally strong, this is a very solid start to the year.

On the balance sheet side, there is one notable movement - cash, short-term investments and equivalents fell from roughly €13.3 billion ($14.6 billion) to €8.4 billion ($9.2 billion). This is due to a combination of payments for investments, dividends and, most importantly, the launch of a new share buyback plan: in Q1 alone, the company bought back about €1.1 billion ($1.2 billion) worth of shares.

What management has to say about the results

New CEO Christophe Fouquet described Q1 as a quarter "within guidance" on revenue, but at the upper end on gross margin. However, his report on demand is key:

Industry growth continues to be underpinned by investment in AI infrastructure

chip demand is beginning to consistently outstrip supply

Customers are accelerating capacity expansion plans for 2026 and beyond

and ASML has a very strong pipeline of new orders and installed base upgrades as a result

Fouquet says bluntly that all these factors are now behind ASML's expectation of further growth in 2026 in all core businesses - so not just the most advanced EUV systems, but also in DUV and services. He also points out that the company has built in "latitude" in its 2026 estimates for various scenarios around export controls - i.e. that even with unpleasant regulatory developments, it should fit into the €36-40bn revenue band with a gross margin of 51-53%.

For Q2 2026, ASML expects revenues of €8.4-9.0 billion ($9.1-9.8 billion) and a gross margin of 51-52%. R&D costs are expected to be about €1.2 billion ($1.3 billion) and administrative costs €0.3 billion ($0.3 billion). This means that even with aggressive R&D investment, it is still a very profitable business.

Long-term results

Revenues rise from roughly €21.2 billion ($23.3 billion) in 2022 to €27.6 billion ($30.3 billion) in 2023, €28.3 billion ($31.1 billion) in 2024 and €31.4 billion ($34.5 billion) in 2025. That means roughly thirty percent growth in 2023, a slight slowdown in 2024, and again over eleven percent in 2025 - a very strong pace for a company of this size and with such high margins.

Gross profit grew even faster than sales: roughly 10.7 billion euros ($11.8 billion) in 2022, 14.1 billion euros ($15.5 billion) in 2023, 14.5 billion euros ($15.9 billion) in 2024, and 16.6 billion euros ($18.3 billion) in 2025. This corresponds to gross margin growth - ASML is succeeding in selling more and more higher value-added systems, while increasing service and upgrade revenues.

Net profit is around €5.6 billion ($6.2 billion) in 2022, rising to €7.84 billion ($8.6 billion) in 2023, falling slightly to €7.57 billion ($8.3 billion) in 2024 and rising to €9.23 billion ($10.1 billion) in 2025. In addition to the growth in profitability, this is helped by a slight decline in the number of shares due to buybacks (the average number of shares fell from around 398 million in 2022 to 389 million in 2025).

Dividends and buybacks

ASML continues to see a combination of rising dividends and buybacks. It plans to pay a total dividend of €7.50 ($8.2) per share for 2025, up 17% from the previous year. It is proposing a final dividend of 2.70 euros ($3.0) per share after three interim dividends of 1.60 euros ($1.75) already paid.

In addition, it is running a share buyback program for 2026-2028, under which ASML bought back about 1.1 billion euros ($1.2 billion) worth of shares in Q1 alone. Given the high valuation, this is questionable for some investors, but in terms of capital structure the company remains very strong and can afford to do so.

Shareholders

The ownership structure is consistent with a global megacap:

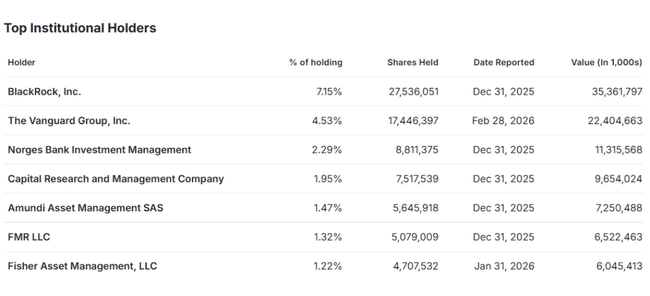

approximately 43% of the shares are held by funds and ETFs

about 9-10% by other institutional investors such as Norges Bank, Capital Group, Amundi, Fidelity, etc.

The rest (less than 48%) is held by public companies and retail investors

The largest shareholders include BlackRock (about 7.1%), Vanguard (about 4.5%), Norges Bank (about 2.3%) and other large asset managers. That said, the sentiment of large global funds on the semiconductor sector - and especially on the "AI capex" story - has had a major impact on ASML's share price.

News

Several things have happened at ASML in recent months that are more important to the story than the Q1 number itself.

After an exceptionally strong Q4 2025, the company reported record order volume of around €13.2 billion (about $14.5 billion), nearly double market expectations, and followed that up Q1 2026 with another "strong but quieter" quarter.

In response to the long-term boom in AI infrastructure and datacenters, it significantly raised its 2026 revenue guidance to €36-40 billion ($39-43 billion) at a gross margin of 51-53%, above both the initial range and analyst consensus.

At the same time, the company announced continued restructuring - including a plan to eliminate some 1,700 jobs to simplify its structure and improve efficiency, while continuing to invest massively in the development of next-generation EUV and High-NA systems.

ASML confirms that capacity, not demand, is the main limit to growth. In materials and commentary, management talks about the key driver being investment in AI infrastructure and that demand for state-of-the-art EUV systems is higher than the company can physically produce. The plan is to deliver a minimum of around 60 EUV systems in 2026, and to approach the 80-unit mark in 2027, which would represent further significant revenue growth.

At the same time, changes in the management and governing bodies are underway - ASML has published the agenda for this year's AGM, where the appointments and renaming of the Board and Supervisory Board members are to be confirmed. The aim is to align the governance of the company with the fact that it is becoming a key strategic player not only for the chip industry but also for geopolitics (West vs. China).