Netflix delivered very strong results in the first quarter of 2026. Revenue is growing at a double-digit pace, operating margins are above 32%, and earnings per share are nearly double last year's. In addition, the company significantly raised free cash flow thanks to an extraordinary payment from the pending Warner Bros. transaction. Discovery and confirms that it is targeting around 12-14% revenue growth and an operating margin of around 31.5% in 2026.

Still, the stock lost more than 9% in the aftermarket after the results were announced. The reason is not the weak quarter, but the earnings structure and a more cautious outlook for the second quarter. Investors see that much of the jump in net profit is one-off and that margins and earnings per share in Q2 will be weaker than they have managed to paint after a very strong Q1.

Q1 2026 results

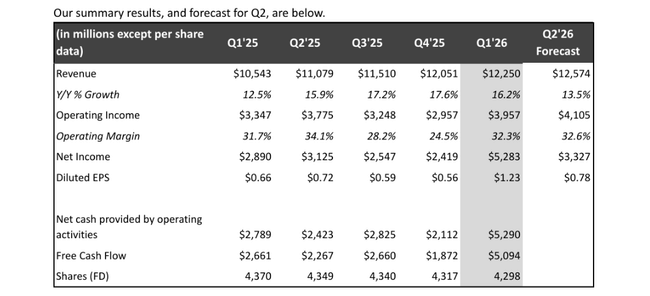

Netflix's $NFLX revenue in the first quarter was roughly $12.25 billion. That's a 16% growth year-over-year, and about 14% after adjusting for currency effects. Revenue growth is on three legs: continued subscriber growth, higher average revenue per user due to price adjustments, and a growing share of advertising revenue. The company itself says revenue was "slightly above plan" precisely because of higher-than-expected subscriber growth and favorable currency.

Operating profit in Q1 was about $4 billion, up about 18% from the same period last year. Operating margin moved to 32.3%, compared to 31.7% in Q1 2025. This means that Netflix was able to not only increase revenue, but also keep costs under control enough to improve margins slightly. For a company that just a few years ago was burning much of its cash flow into content and expansion, this is confirmation of a transition into a "profitable" growth phase.

At the net profit level, the numbers look even better. Netflix earned about $5.3 billion versus about $2.9 billion a year earlier. Diluted earnings per share rose from $0.66 to $1.23, up roughly 86%, while market expectations were around $0.75-0.80. Thus, the company significantly beat estimates in terms of net income and EPS.

The important thing is why EPS jumped so dramatically. In the first quarter, Netflix collected $2.8 billion as a fee for the cancellation of a planned deal with Warner Bros. Discovery, which was part of a broader deal with Paramount. The amount is a one-time charge, appearing on the books as "interest and other income" and artificially inflating net income and earnings per share. Without it, EPS would still be solidly above estimates, but the difference from consensus would not be nearly as spectacular.

The significant impact of this payment can also be seen in cash flow. Net operating cash flow increased roughly year-over-year from $2.8 billion to $5.3 billion and free cash flow from $2.7 billion to $5.1 billion. As a result, Netflix adjusted its free cash flow estimate for 2026 from roughly $11 billion to $12.5 billion. It also reiterates that it wants to keep the ratio of cash spend on content to its book amortization around 1.1 times, so it intends to continue to invest heavily in content despite strong cash flow.

Overall, then, Q1 2026 in terms of revenue, operating profit and cash flow confirms that Netflix can grow at double-digit rates while generating high margins. However, much of the jump in net profit is one-off and the market is not forgetting that when interpreting the results.

Outlook and why the stock is falling after the results

For the full year 2026, Netflix leaves its own outlook unchanged. It still expects revenues in the range of $50.7 billion to $51.7 billion, which equates to roughly 12-14% growth, and an operating margin of around 31.5%. That's up about two percentage points from 29.5% in 2025. The company thus confirms that it sees itself as a steady double-digit growth business with improving profitability and strong free cash flow.

So where is the problem? In the detailed outlook for the second quarter. Netflix itself says that content cost growth this year will be mainly concentrated in the first half of the year and that it is the second quarter that will have the highest year-on-year growth in content amortisation. This means that even with double-digit revenue growth, operating margins will deteriorate year-on-year in Q2. The company expects Q2 operating margin to be roughly 32.6%, compared to 34.1% in Q2 2025.

At the same time, the market is sensitive to the Q2 earnings per share estimate. Based on the numbers Netflix is reporting, Q2 EPS should be around $0.78, which is less than what most analysts were counting on. After a first quarter where EPS significantly beat expectations thanks to a combination of higher operating profit and a one-time charge from Warner/Paramount, investors were hoping for a more aggressive tone in the months ahead. The reality is more cautious: the second quarter will be more cost-intensive, and so earnings per share are unlikely to be as strong as would be consistent with the post-Q1 "euphoria."

Add to that the psychological equation around the failed acquisition of Warner Bros. Discovery. Netflix explains in a letter to shareholders that Warner would be a nice accelerator to the strategy, but only at a price it considers reasonable. The company stresses that it has multiple avenues to fulfill its ambitions - in-house production, licensing, partnerships - and that it would rather focus on disciplined capital management and organic growth than a "deal at any price." But part of the market was clearly hoping for a big leap forward through acquisition, and with it more flagship brands in the library. Instead, there's a one-time revenue of $2.8 billion, no Warner in the catalog, and the prospect of "only" 12-14% revenue growth annually.

The result is a typical scenario where short-term players react to the combination of inflated one-time earnings and a less optimistic short-term outlook by realizing gains. That's why we see the stock fall more than 9% in the aftermarket, even though the quarterly numbers themselves are very good and the full-year outlook remains stable.

Long-term results

If we look at the last four years, we can see how Netflix has gradually transitioned from a "grow at any cost" phase to a model that combines a decent revenue growth rate with high profitability.

Revenues in 2022 were roughly $31.6 billion. By 2023, they have moved to 33.7 billion, a growth rate of about seven percent. In 2024, they reached $39 billion, and in 2025, more than $45.2 billion. This corresponds to roughly sixteen percent growth in two consecutive years. After a slower year in 2023, when the streaming market took a breather after the covid boom, Netflix was able to return to double-digit growth thanks to paid account sharing, pricing adjustments, and the rollout of an advertising plan.

Gross profit increased faster than revenue during this period. It was around $12.4 billion in 2022, $14 billion a year later, $18 billion in 2024 and around $21.9 billion in 2025. The improving gross margin confirms that Netflix can get more out of every dollar of revenue, whether by better managing content costs or monetizing users more effectively.

Operating profit grew from roughly $5.6 billion in 2022 to $7 billion in 2023, $10.4 billion in 2024 and $13.3 billion in 2025, more than doubling in three years. Net profit has moved from $4.5 billion in 2022 to $5.4 billion in 2023 and $8.7 billion in 2024 to about $11 billion in 2025. Profits are growing faster than sales, which is exactly the shift you want to see from a more mature but still growing business.

A looser but important figure is EBITDA. This was around $20.3 billion in 2022, $21.5 billion in 2023, $26.3 billion in 2024, and around $30.2 billion in 2025. This makes Netflix a company that is not only growing fast, but also generating very high operating cash flow on a steady basis. It is Q1 2026, with free cash flow of over $5 billion, that fits into this picture, even if part of that increment is due to a one-time payment.

Shareholders

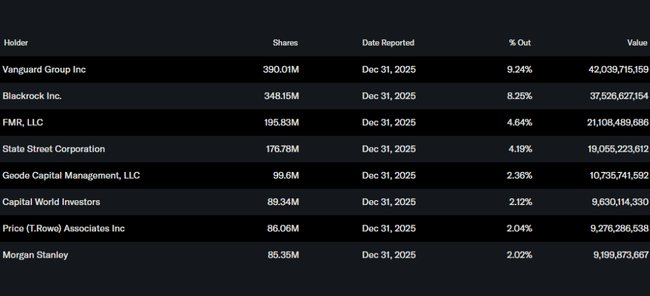

Netflix is now a classic big blue chip, with institutional ownership playing a major role. Management and other insiders hold less than one percent of the shares, while institutions own more than 80% of the total number of shares and free float. The largest shareholders are global asset managers such as Vanguard, BlackRock, Fidelity and State Street, each with a few percent stake. This means that short-term price swings are very sensitive to the mood of a few dozen large funds - when they decide to reduce exposure after earnings for a more conservative earnings outlook, the stock can react very quickly, even if the company's fundamental story doesn't change much.

In terms of capital deployment, Netflix continues to pursue a strategy of prioritizing investment in content, technology and any smaller acquisitions, before returning excess cash to shareholders through share buybacks. During the period when the potential transaction with Warner Bros. Discovery, the buyback program was temporarily suspended, but resumed in full swing following the withdrawal from the deal and the collection of the break-up fee. In the first quarter, Netflix repurchased roughly 13.5 million shares for about $1.3 billion, leaving it with several billion dollars of room on its existing program. The company is not yet paying a dividend, and the priority is to continue to build its content and technology base, and to do so by gradually reducing the number of shares outstanding.

Strategic directions and news

Strategically, Netflix is looking to expand its role from "just" a streaming platform to the broader entertainment ecosystem. It is adding video podcasts, games and live streaming alongside its core series and movies. In the first quarter, it broadcast over 70 live events, including the World Baseball Classic in Japan, which attracted over thirty million viewers and became the most-watched program in Netflix's history in that market. Similarly, a live stream of a BTS band event brought in tens of millions of viewers worldwide and topped the charts in many countries.

In games, Netflix is developing several categories ranging from narrative titles to party and puzzle games to children's games. The new Netflix Playground app specifically targets children's users, and the company says it's already seeing early promising signs - roughly ten percent of children's profiles are at least trying out games, and nearly half of children's profiles watch Netflix on mobile and tablet devices, where games can be easily integrated.

Technologically, Netflix is betting on the next wave of personalisation and the use of artificial intelligence. AI is meant to help both in recommending content and customizing the user interface, as well as in the creation and post-production of the content itself. This shift includes a redesign of the mobile app and tests of new formats such as vertical video.

In terms of governance, the important news is the formal departure of co-founder Reed Hastings from the board. Hastings had previously stepped down from the role of co-CEO and moved into the role of executive chairman. He has now announced that he will no longer run for the board and wants to focus more on philanthropy and other projects. In practice, this only completes the handover of the reins to the current leadership, but it symbolically closes a chapter in Netflix's history and confirms that the future of the company rests on the duo of Greg Peters and Ted Sarandos and the culture that Hastings helped build.